Denis Barrier

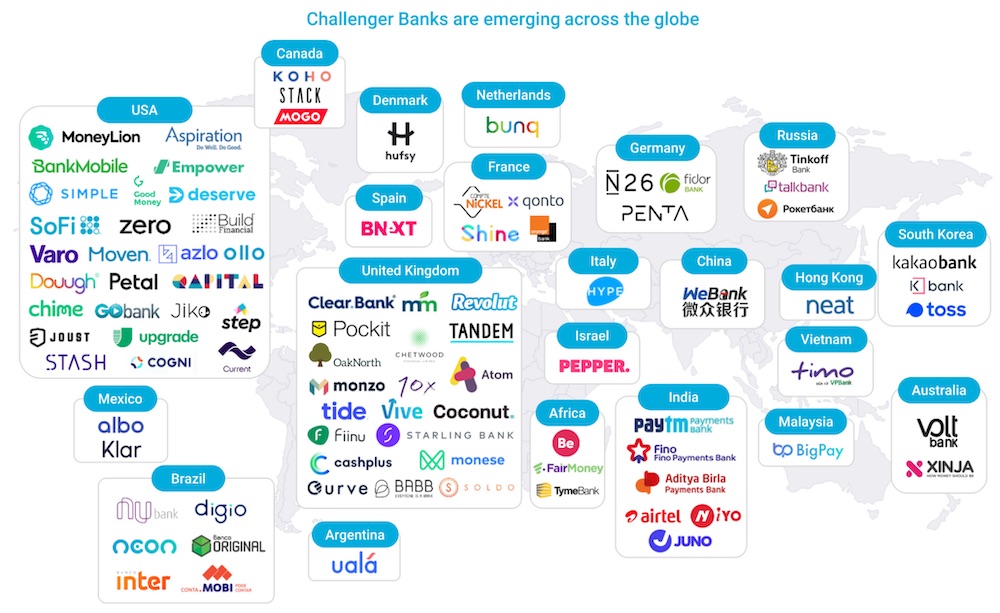

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Five global models of neobanks

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Ecosystem-led: One of the original neobank models (that we consider largely unproven), where the checking account may not be the profit driver but unlocks a range of monetization strategies as a gateway to a broader financial products ecosystem. Many in this category also charge monthly subscriptions as an additional vector of monetization (e.g. N26, Monzo / Europe).

Asset-led: Offers savings accounts and looks to acquire deposits with competitive rates [e.g. Goldman’s Marcus, Beam / U.S.]. There are also those that focus on ethical or moral spend management [e.g. Aspiration Bank / U.S.].

Product extensions: Credit-led models are distinctly successful, but are also merely examples of product extensions, blurring the lines between financial domains [e.g.,Robinhood, Wealthfront / U.S.]. One of the biggest drivers here will come from larger tech companies [e.g. Square Cash App / U.S.] and partnerships with banks [e.g. Amazon / U.S.].

Neobanks have three key success factors — underpinned by impact

The difference in models is driven by various market needs and regulations, but in such a crowded space, which neobanks will succeed? Before digging into specifics, there is one overarching factor — the most successful neobanks are those that are the most impactful, particularly to underserved customers.

Valued at $10B, Nubank launches it’s Nu credit card in Mexico

Despite popular belief, the rise in digital banks is not a product of preference by the younger digital-native generations (e.g. millennials), but from reaching a broader set of customers that have historically been overlooked by incumbent banks. In the U.S. for instance, the average Chime customer earns between $35,000 and $70,000 with lower account balances — accounts considered to be unprofitable for most banks.

Neobanks represent a paradigm shift in financial services, bringing us back to a customer-centric core, offering services that are cheaper, simplified, more useful and better targeted for the people who have been left out of the traditional system in some capacity. But beyond impact, there are three key elements that set successful neobanks apart:

Strong stand-alone unit economics: A key driver to long-term success is having strong standalone unit economics with the core bank account product. For instance, an interchange model can bring significant value to customers, particularly those in the middle class who benefit from lower costs. However, this isn’t applicable everywhere. In Europe, average rates on transactions are significantly lower (capped at 0.3% compared to approximately 1.2% in the U.S.), making it more difficult to build traction.

The digital bank account strengthens the core offering: Another factor is when the neobank product can be a core improvement to the larger offering. Nubank’s case is striking. By having customers leverage its bank account, Nubank benefits from a lower cost of funds from deposits. Importantly, by deepening the customer relationship, it also gleans more insights into the customer’s credit worthiness and spending potential.

Massive acquisition subsidization generated externally: Neobanks that leverage a strong existing customer base, and have a customer cost acquisition (CAC) distribution advantage, will be able to scale more challenging unit economics more successfully. In a space that is still largely dominated by incumbents with CACs steadily increasing over the last five years, a big challenge for fintechs is customer adoption and retention. This is why product extensions work well — such as Robinhood’s account structure off the back of its stock trading, or Apple’s credit card launched with Goldman Sachs, which has reached 3.1 million American customers in its first year.

In an ideal world, an impactful neobank will have strong standalone unit economics or strengthen an existing core offering, as well as enjoy a distribution advantage. While the model can work with only one, without two, neobanks will struggle to scale.

Unique challenges in emerging markets

Globally, approximately 1.7 billion people are underbanked, with no access to the formal economy. Neobanks have emerged as a powerful bridge to promote financial inclusion, but there are unique challenges in emerging markets — a topic that easily deserves a separate article, but from a high-level, points back to a lack of critical infrastructure.

A reliable cash-in and cash-out flow is required and sometimes can kick-start the ecosystem. But for the true bottom of the pyramid, the critical infrastructure needs to be created first. Without a widespread payment infrastructure, including point-of-sale (POS) acceptance, a card-based model will struggle, as the value is directly correlated to ease of use. One reason Nubank scaled in Brazil is because POS penetration is on par with many Western countries.

Take credit-led models as another example, which traditionally depends on credit score infrastructure. Credit scores in many emerging markets either have limited coverage or are non-existent which forces credit-led neobanks to develop their own insights on a customer’s propensity to repay.

We’re seeing other players set the seeds in areas such as Sub-Saharan Africa, Southeast Asia and Latin America, on the heels of the massive mobile money trend, and of course those that are working to close the digital divide.

Neobanks are here to stay

Neobanks have created a new tech stack, completely changing the services, products and speed at which they are delivered, and creating more fluidity in payments and currencies. The neobank space will continue to grow with more specialized offerings emerging for new demographics, but the true success driver is because they are highly impactful — offering greater transparency, lower costs and easier access to financial services. These digital challengers are increasingly becoming the social, sustainable and people-oriented financial players to the populations who need them most.

Disclosure: Cathay Innovation is an investor in Chime.

Comment