A new data set from Silicon Valley Bank (SVB) details how startups are reacting to the post-unicorn era as COVID-19-related disruptions upset the global economy and remake the risk tolerance of private investors.

What SVB’s new report shows is unsurprising: venture capital deal volumes are falling, startups are tapping existing debt capacities to add cash to balances while they still can and some upstart firms are curtailing spend to reduce unprofitability. The last data point comes via the lens of startups that recently raised, making the data more a snapshot of what companies that are successfully attracting capital may have accomplished with regard to improving profitability — the directional shifts are material regardless of that particular nuance.

Let’s briefly examine what the data says and what it tells us about the state of the startup market.

Spending less, borrowing more

Venture capitalists are pulling back, SVB data indicates. A chart from its Q2 markets report notes that the “SVB Deal Activity Index” had fallen from a rating of 160 in early March to just over 70 by mid-to-late-April. That staggering decline means fewer rounds are getting done and that there is less capital going into startups of all sizes.

This mirrors what TechCrunch has heard from founders looking for capital.

Less capital on offer from VCs has startups looking for capital in other places. As your couch can only cough up so many quarters, startups are increasingly turning to debt.

We know this because venture debt lines are often facilitated and funded by SVB itself — many startups secure a new debt line after fundraising for use between then and their proximate venture capital event — so it has the data. And utilization of those facilities went up by 23% in relative terms, and 10% in absolute terms as debt lines associated with tech firms held by SVB rose from 43% in early 2020 to 53% in March of this year.

Given the trend, we can anticipate that the same number will rise more when April data comes in.

So, venture capital inflows are down and more startups are taking on debt. Thinking out loud, you might expect startups to slow spend at the same time, allowing their business to drift closer to breaking even, or generating adjusted profit. Per SVB, that’s precisely what’s happening.

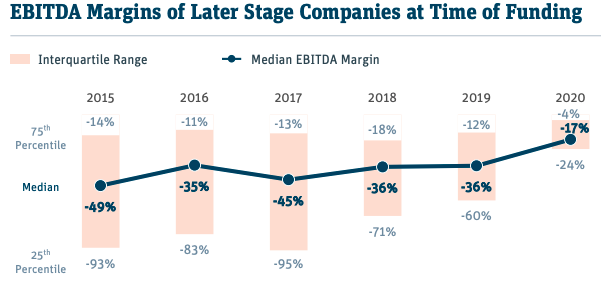

Observe the following chart (shared with permission):

Unpacking that dataplot, we’ve seen the least profitable late-stage firms dramatically reduce unprofitability, helping cut the median EBITDA margin’s red ink in half in a single quarter. Notably, firms on the other end of the scale have reduced negative EBITDA margins so close to break-even that the 75th percentile and better are effectively not losing money.

Good. That means that some unicorns will get through the downturn in fine order, provided that they don’t loosen their purse strings after their recent spend reductions.

Looking backwards in time, however, holy shit that lower-tier of late-stage companies that raised capital in the past few years. The 25th percentile of late-stage companies that raised capital in 2017 had a -95% EBITDA margin? That means they were certainly running worse than -100% net margins. That’s terrible! Really and truly awful!

(It’s a historical fact of many of today’s tech giants that even in their youth they generated profit; of today’s Big Five, only Amazon was not profitable early on, and Amazon’s deficits were honestly not very bad, even when it went public.)

But those losses have been cut by around 60% in 2020 from their 2019 results as the startup world pivots to a risk-off posture, among later-stage companies that have raised this year. What the same chart would look like if, in a magical world, we could see all late-stage startup financial results? Not as good, I’d bet you $5. Why? Because the startups that could — and did — cut the most are probably those most palatable for VC funding. The late-stage startups that can’t, or did not, cut are probably less enticing. And thus did not raise, not making it into the above chart.

Finally, the post-2017 profitability trend for later-stage startups has been largely upwards, the direction you’d want to see the cohort move if they wanted to survive a winter (or Fifth Season) that came as a surprise. Like the one we’re in now.

The data matches our gut, which feels good. There’s still a lot more work to do for us to fully understand the changed venture and startup worlds, but we’re making progress.

Comment