OK, OK, no more 2.0 ‘clichesuffixes’ :)

I’ve been eagerly awaiting the launch of Wesabe (not to be confused with the nuclear horseradish) for several weeks. Firstly, it’s an interesting concept and secondly, one of the co-founders is Marc Hedlund – O’Reilly Media’s entrepreneur-in-residence and author of hugely entertaining and informative talks on VC Funding for Geeks.

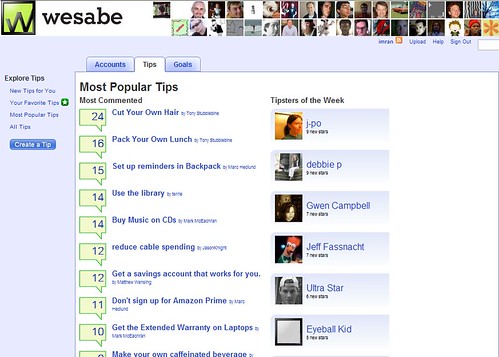

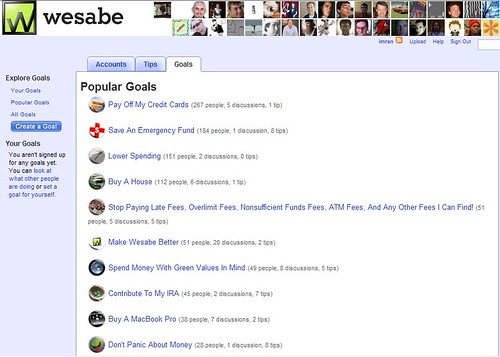

Wesabe essentially helps users figure out where they can save money and manage their finances better by anonymising, aggregating and analysing their personal financial data and comparing it with that of other Wesabe users. Users can tag each entry in their spending (lunch, movies etc.), set goals for themselves and tag their spending entries to find tips and shared goals from other users.

Wesabe is a great concept – a 43 Things for your money – and it’ll be interesting to see how the community evolves over time. Users are already sharing useful tips and advise, many of which can be glaringly obvious, but nevertheless hearing it from another person with a similar lifestyle can be valuable. Perhaps with a future layer of reputation, the tips may be eminently trustable.

Though Wesabe is a US startup, it emphasises a gap in the British financial services sector and UK startup scene. Britain has one of the largest concentrations of financial sector expertise in the world, a population that favours digital transactions over cash (and is very much in debt!) and yet the world’s fiscal hub is not giving rise to the emerging generation of Money 2.0 startups – the likes of BillMonk, ChipIn, FEED Tribes, Fundable, Prosper, TextPayMe and indeed, Wesabe.

Is this a consequence of conservatism in the financial sector, the glamour and glitz of social and entertainment based Web 2.0 services or simply the superior entrepreneurial abilities of American startups. Ironically, the one exception is Zopa, founded by former VPs and execs from Barclays, Tesco Personal Finance, Abbey and Egg; the latter, of course, led many innovations in online banking and lending in the first dotcom boom.

There’s perhaps a structural change that could help move things forward. Wesabe has shown that unbundling our banking data from our banks can help create new areas of value and usefulness – coincidentally, Marc led a panel discussion on Open Data at Web 2.0. Perhaps if banks began to offer platform services, like secured RSS feeds from your current account, they could assist in ushering in an ecosphere of innovative services that add value to their business and create growth for others…perhaps creating future acquisitions for themselves as those startups flourish.

A few years ago, the DaVinci Institute hosted a summit on the Future Of Money – I think it might be an interesting time to revisit those themes :)

Comment