WalkMe is going public: Let’s stroll through its numbers

Image Credits: Somyot Techapuwapat / EyeEm / Getty Images

Hot off the heels of our look into Marqeta’s IPO filing and dives into SPACs for Bright Machines and Bird, we’re parsing the WalkMe IPO filing. Later this week, Squarespace will direct list and we’ll see IPOs from Oatly and Procore. It’s a super busy time for public debuts of all sorts.

Given how hectic the IPO market is, we’re going to skip our usual throat clearing and dig into WalkMe’s IPO document. As always, we’ll start with a brief overview of its product and then move into discussing its financial performance.

Image Credits: Alex Wilhelm

WalkMe is the second Israel-based technology company to file to go public this week: No-code startup Monday.com is also pursuing an American IPO.

Alright! Into the breach.

What does WalkMe do?

WalkMe’s software provides visual overlays on websites that help users navigate the product in question. I base that explanation on my time at Crunchbase, which was a customer during at least part of my time there. WalkMe is popular with marketing teams who want to introduce users to a new or refreshed experience.

Per the company’s F-1 filing, other elements of its service that matter include its onboarding system and what WalkMe calls Workstation, or its “single interface to the applications within an enterprise and simplifies task completion through a natural language conversational interface and automation.” We’re including that last feature because it says “automation,” which, in the wake of the UiPath IPO, is a word worth watching. Investors are.

At a high level, WalkMe is a SaaS business, which means that when we digest its results we are digging into a modern software company. Let’s do just that.

WalkMe’s numbers

From 2019 to 2020, WalkMe grew its revenues from $105.1 million to $148.3 million, a gain of 41%. In its most recent quarter, the company’s growth rate slowed: From Q1 2020 to Q1 2021, WalkMe’s top line grew 25% from $34.2 million to $42.7 million.

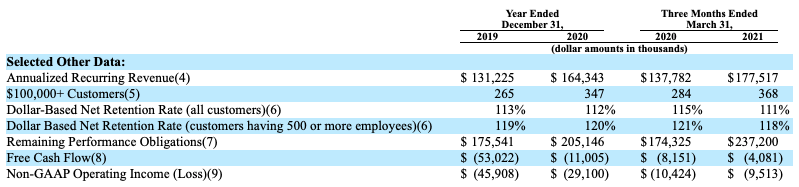

In SaaS terms, WalkMe calculates that its annual recurring revenue, or ARR, grew from $131.2 million at the end of 2019 to $164.3 million in 2020. In more granular terms, the company’s ARR grew from $137.8 million to $177.5 million in the first quarters of 2020, and 2021, respectively.

Sticking to SaaS metrics for a moment, WalkMe breaks its dollar-based net retention (DBNR) into two buckets. One for all its customers, and other dealing strictly with customers that have more than 500 employees. As you’d expect, the latter category has better DBNR results, which is why the company gave itself the additional line-item:

Image Credits: WalkMe

It isn’t great that we’re seeing the company’s aggregate DBNR fall from 2019 to 2020, and from Q1 2020 to Q1 2021. And its modest improvement of its larger-customer DBNR from 2019 to 2020 is undercut by its decline into the current year.

WalkMe is a growing software business. It’s valuable. But the company is not posting Slack-like growth, so we have to care about its profitability a bit more than we might if it was seeing more top-line expansion.

Profits, though?

A 40%+ growth rate is great for a company going public. A 25% growth rate is less enticing. Does WalkMe generate profits, or kick off lots of cash to compensate for its slowing growth?

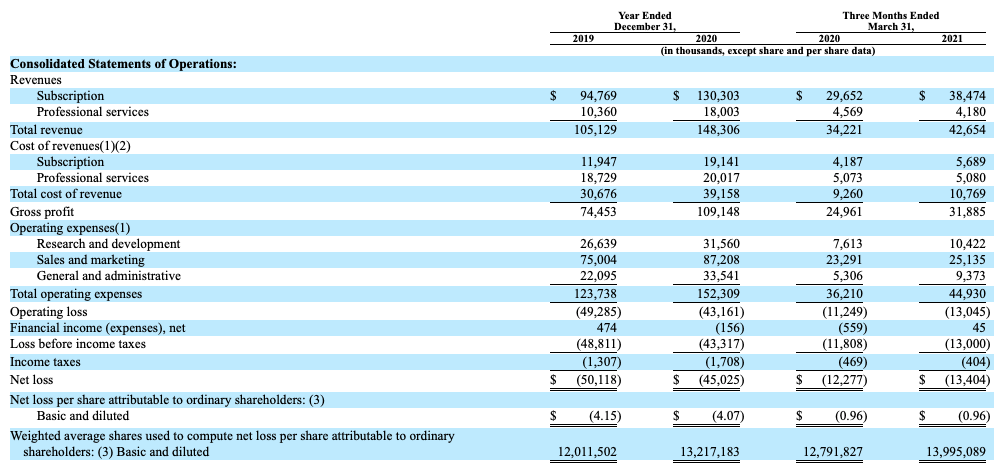

Nope, though things are improving regarding the company’s profitability. Here’s its collected income statement:

Image Credits: WalkMe

As we can quickly see, WalkMe’s net loss improved from 2019 to 2020, but worsened slightly in gross dollar terms when we compare Q1 2020 to Q1 2021. Our perspective is that the sharpest rise in spend in Q1 2021 was G&A, which sounds to us like a company bulking up its finance operation ahead of an IPO. Or something else, but either way the company’s losses are generally trending down while its revenue rises. That’s good. Everyone loves operating leverage.

If we deduct the expense of share-based compensation, Q1 2021 would have been less unprofitable than Q1 2020 by a few million dollars.

Finally, on the profit front, cash flow. WalkMe is making solid progress toward reducing its cash burn to zero. For example, in Q1 2020 the company’s operations consumed $7.4 million. In Q1 2021 that number fell to $2.9 million.

Just tell me what to think

WalkMe is an interesting company. It’s not growing fast enough to light up market chatter. But if it can convince investors during its roadshow that its growth rate either won’t fall further, or could even accelerate, it can chart a course to lots of future cash flow. That’s valuable.

How valuable is probably the question. PitchBook estimates that WalkMe was worth about $1 billion when it raised in 2018. But the company also raised in 2019, when it added $90 million to its books. We don’t know at what valuation those funds were raised.

But looking at various possible comps, Anaplan is also growing at a pace of around 25%. Its enterprise value is around 15x its annualized revenues. Given the modest cash and debt situation that we find WalkMe in, we can simply convert that number to a market cap figure, and, through a glass darkly, estimate that the debuting company could be worth around $2.6 billion. That’s probably a win compared to its final private valuation.

More when we have it of course, but stick close to TechCrunch as we work our way through a torrent of unicorn liquidity.