How investors can still get strong returns from late-stage tech startups

Image Credits: Grafissimo / Getty Images

Last year was a record 12 months for the tech industry, with immense amounts of money flowing into both early- and late-stage companies as well as an all-time-high number of IPOs. But it feels like 2022 has been exactly the opposite.

This year has proven that there is always risk in any investment, whether it’s a public stock or a private startup. While the last couple of years may have allowed many people to put on their blinders about those risks, ups and downs are natural and should be expected.

Still, there are ways to mitigate risk when investing in late-stage companies. For investors, now is a good time to start seeing the opportunities while also protecting themselves against potential risks down the line.

What’s affecting late-stage startup valuations in tech?

Risk exists even in the “good times.”

Tech companies — private and public — have seen strong corrections to their valuations. Some companies that went public in the last year or two have lost more than 75% of their value.

Here’s how things have changed for companies of all stripes:

Image Credits: Secfi

As even high-growth companies see their values being halved or worse, it’s no surprise that private investors and venture capitalists have slowed down their capital deployments, especially to late-stage companies.

Many of these companies were forced to delay their IPOs until the markets calmed down and had to start conserving cash and extending their runways for longer than they anticipated. Some have already lowered their valuations, either in response to these market corrections ahead of a future IPO or to attract investors.

Many tech startups can still outrun the down market

The current market is impacting high-growth companies that consistently lose money the hardest. But it’s also rewarding those that are prioritizing profitability, which is why many companies are reducing spending and costs.

Plenty of companies have always combined consistent growth, cash efficiency and profitability. And there are companies that continue to be profitable (on an EBITDA or cash-flow basis).

Battery has an excellent overview of how to view the differences between these types of companies. For example, the report visualizes a popular concept, the “Rule of 40,” which states a tech company’s combined growth rate and profit margin should exceed 40% and further breaks this down into four different zones based on a company’s multiples. The point is to show the difference in how those companies are performing in the markets when weighing growth and profitability.

This focus on profitability is why many startups are taking drastic steps to save cash. Layoffs are also happening because many companies went on hiring sprees, anticipating growth over the next few years. But, as growth stagnated this year and is not expected for another couple of years, it is unfortunately better for the business to save those associated costs.

Furthermore, not laying off workers could be a bad signal to investors. When the market trends downward, companies and their founders need to show that they can make tough decisions. Of course, layoffs are always a last resort, but making those tough decisions quickly can offset even worse decisions down the line.

That’s all to say that great companies still exist, and they are taking steps to thrive and survive, despite current trends and decisions that could be interpreted otherwise.

The tech industry is resilient to economic downturns

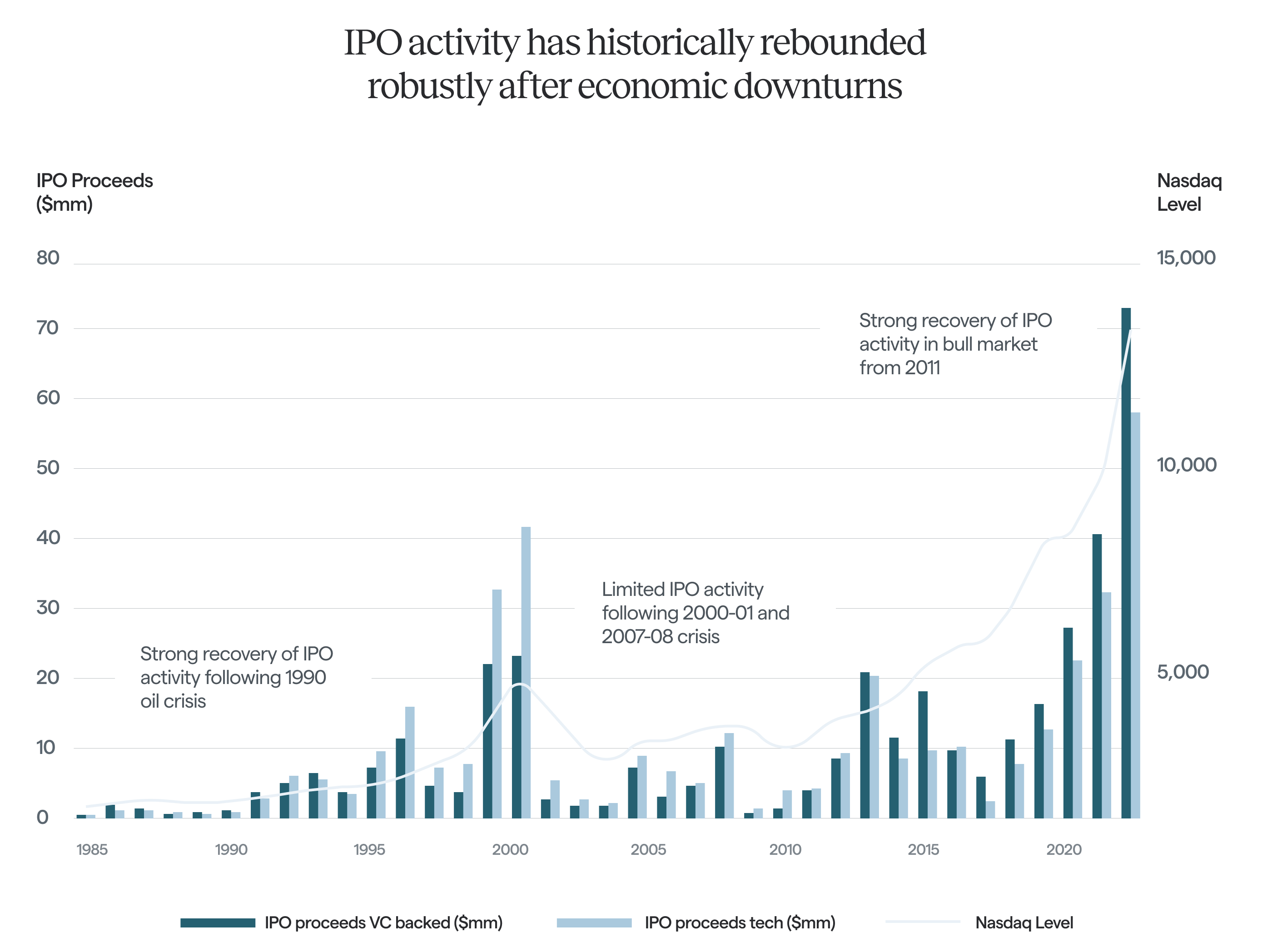

If we look back at past economic downturns and bear markets, the tech industry has performed fairly well, and IPO activity has always bounced back. That’s why, after the market stabilizes, it should be a good time for investors to get back into the private markets. The entry point will be uniquely low, as evidenced by this chart of IPO activity over the last few decades:

Image Credits: Secfi

Of course, it’s hardest to predict when that bottom will happen and things start to calm down.

However, governments and central authorities are taking action to stabilize markets in the near to medium term. For example, governments are finally beginning to tackle inflation more aggressively, with the Federal Reserve, European Central Bank and Bank of England raising rates at a clip not seen in decades. The hope is that financial stability will return in three to 12 months if inflation can be tamed.

The other side of this coin is persistent shock from energy situation as well as politics — the war in Ukraine and skyrocketing gas prices — but there is hope those will also ease in the next year or so. That should reduce the supply-chain-driven inflation pressure (as opposed to consumer-driven inflation), as governments readjust their oil supply and suppliers.

But investors can still get equity-like returns

Secondary markets have become a viable and popular way for investors to buy a stake in private companies via employees, and even executives, willing to sell their pre-IPO shares. Many who turned to secondary markets saw stellar returns the last few years, as they tend to perform well during bull markets.

But, as we’re now seeing, markets can change rapidly and aggressively, resulting in a level of risk that may not be tolerable for all investors, especially considering the limited data available for private markets.

Some companies have attempted to address these concerns to make investing in late-stage startups more accessible. In these approaches, instead of employees selling their shares, investors help them exercise their options so employees retain ownership, and then participate in some of the upside when the company exits.

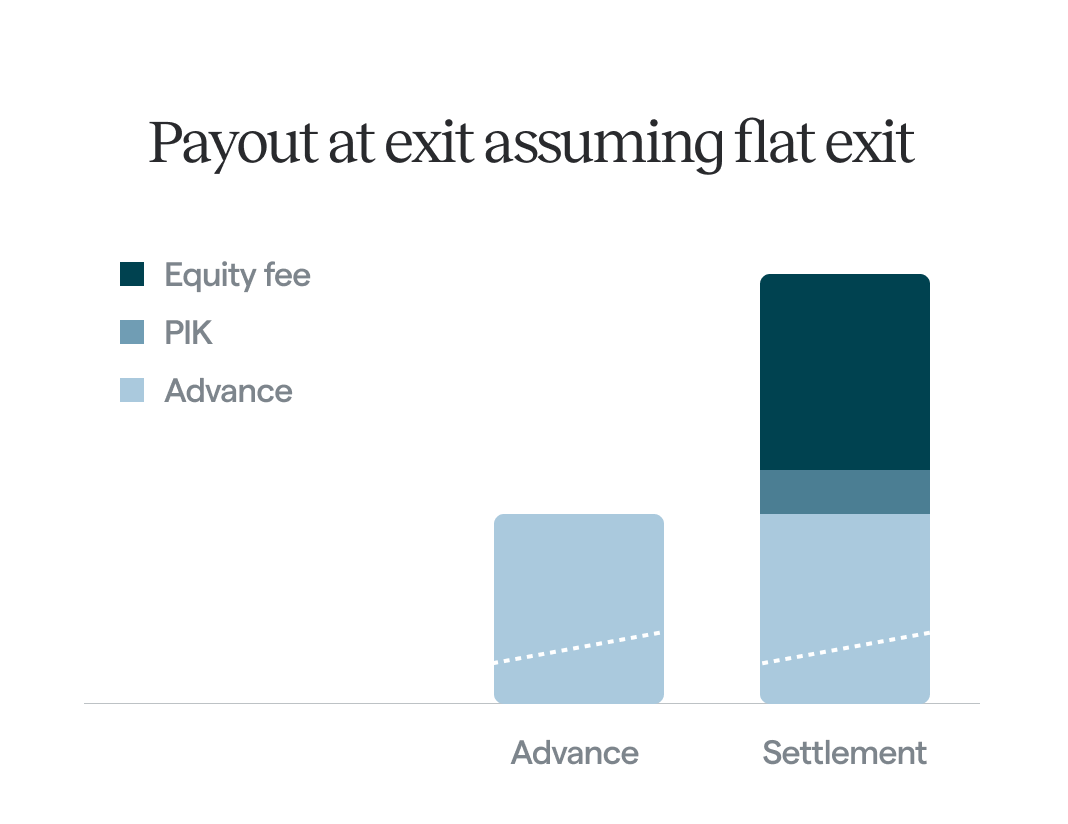

Here’s how these transactions work:

- The investor provides an advance for an individual (the employee) to exercise their stock options, as well as pay the associated taxes.

- The advance is over-collateralized to provide a significant buffer for market and price volatility.

- When the company exits, the individual pays the investor the original advanced amount plus a PIK (payment-in-kind) interest fee (compounded from origination until exit) and a percentage of the valued equity at the time of repayment.

Image Credits: Secfi

How this helps with downside protection

When the markets are doing well, investors are more willing to take on risk, because they believe that risk is minimal. But, this year has illustrated the importance of downside protection.

Risk exists even in the “good times.” Companies can delay IPOs for a variety of reasons; exits can be weaker than investors hope; or there are unforeseen issues, like those at Better.com.

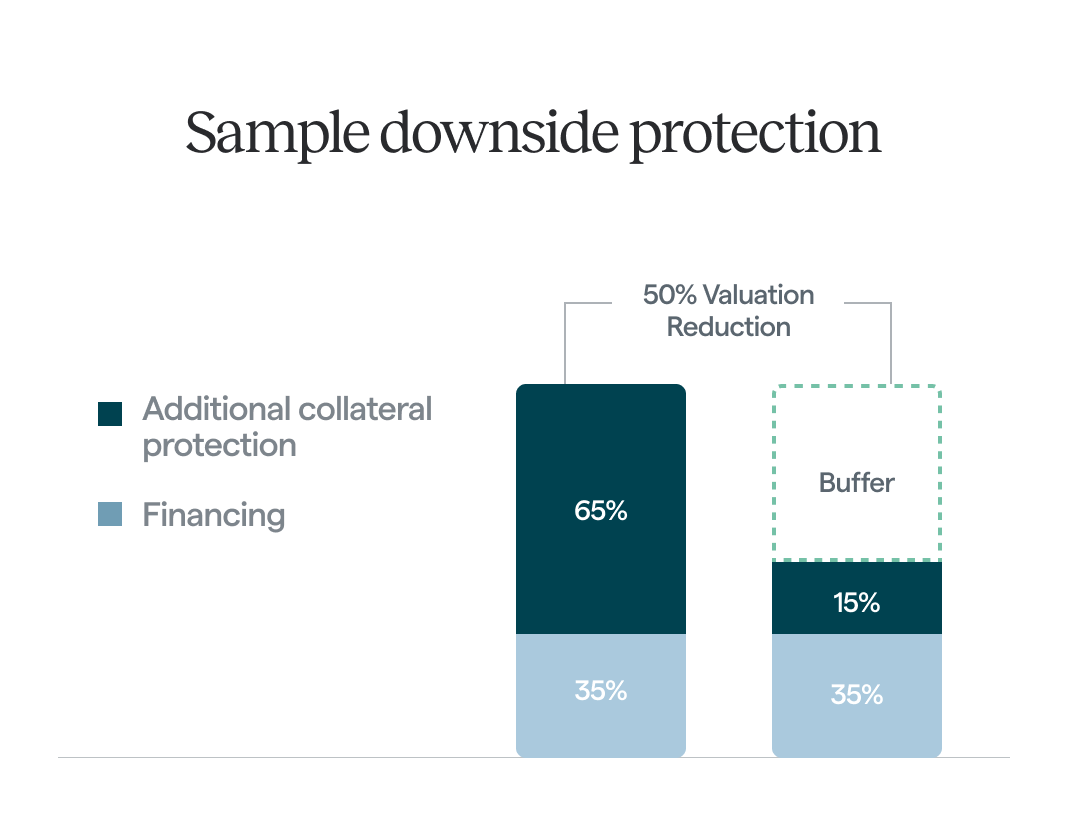

This type of transaction presents downside protection through over-collateralization, which provides a significant buffer to absorb price volatility, especially in a market like today’s. In a secondary transaction, however, a drop in the share price would result in a loss-making position.

For example, if a 35% advance is provided to an individual to exercise their options, the value of those shares would have to fall 65% before impacting the investor. Here’s a visual:

Image Credits: Secfi

Financing transactions vs. secondary sales

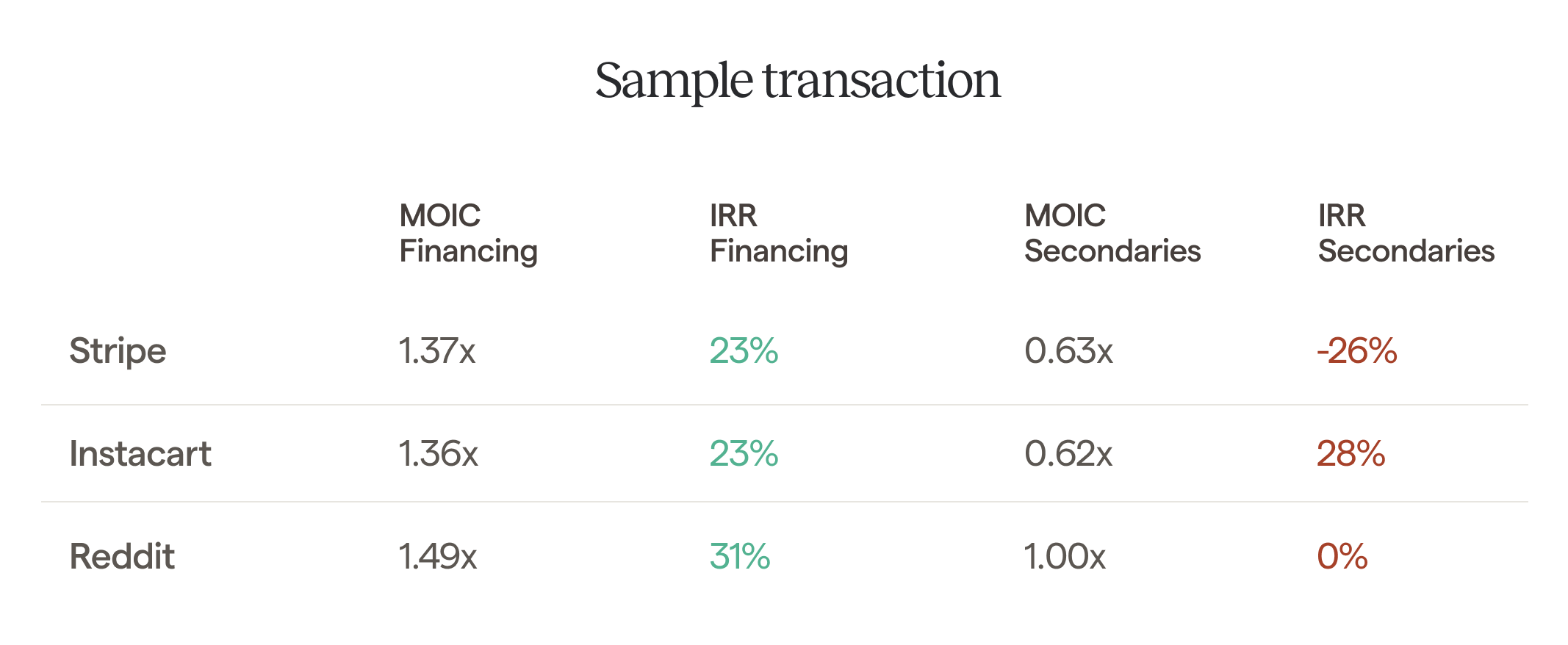

Here are a few examples of how these types of transactions compare to secondaries, using Stripe, Instacart and Reddit, which are all still private. These companies all reached their peak valuations in 2021 and were poised to exit this year. They also all saw those valuations significantly reduced by the downturn.

Let’s assume that the investment lifetime (from entry to an IPO or exit) is 1.5 years, and that the investment is at 30% ATV (a representation of the cost of the shares versus the estimated value of the shares).

IRR is the internal rate of return, an annualized figure of the returns; MOIC is the multiple of invested capital, how much the money has grown (end value divided by the initial investment). Image Credits: Secfi

You can see that even with these companies’ reduced valuations, this type of financing can still deliver strong returns when they go public. On the other hand, those that invested via secondary transactions will likely see losses or flat returns at best.

Look for entry points, but with the right protections

Even in a down market, investors are still looking for access to the right private companies. But they should also want the right access that yields healthy returns while also providing protection against tepid exits or market volatility.

The good news is that investors can still access plenty of strong private companies, and they can still see good returns once they do exit, even if valuations and exit prices are lower than last year’s expectations.