In the ‘buy now, pay later’ wars, PayPal is primed for dominance

Image Credits: the burtons / Getty Images

The COVID-19 pandemic has already dramatically reshaped how Americans shop, with e-commerce expected to grow 20% in 2020 as a greater proportion of users shift from in-store to online. Due to this transition to greater online shopping coupled with the increased financial uncertainty of the American public, Button expects that COVID-19 will also reshape how Americans pay for their shopping with a similarly dramatic increase in adoption of “buy now, pay later” payment programs (BNPL) at checkout.

The greatest limitation to BNPL adoption is its availability, i.e., whether the retailer offers its customers a BNPL program. Offering such a program in the checkout flow doesn’t happen with the flip of a switch. It requires a direct integration into the retailer’s point-of-sale system, which is an onerous process and a meaningful moat for providers in place. Leaders in the BNPL field include Klarna, Affirm, Afterpay and Quadpay — and PayPal made a major announcement in August that it would begin offering BNPL services.

In anticipation of this season’s increased adoption of BNPL, mobile commerce platform Button examined our marketplace to understand the current state of affairs as it relates to BNPL — how many retailers feature BNPL programs, which programs are most prevalent and how often do the BNPL programs compete head-to-head.

Using Button’s Commerce Intelligence, we analyzed the payment method used by consumers in our marketplace over the past 90 days. We reviewed nearly 500,000 transactions across more than 300 retailers. Key highlights included:

- Of nearly 500,000 transactions, Button observed five available alternative payment solutions: Afterpay, Affirm, Klarna, QuadPay and PayPal. While PayPal’s payment option is not exclusively a BNPL option like the others, we included it in this analysis to highlight the significant foundation upon which it can build its BNPL program relative to its competitors.

- PayPal had the greatest retailer coverage with a presence of 65% retailers. Afterpay was a distant second at 10%, then Affirm 6%, Klarna 5% and QuadPay 2%.

Image Credits: Button (opens in a new window)

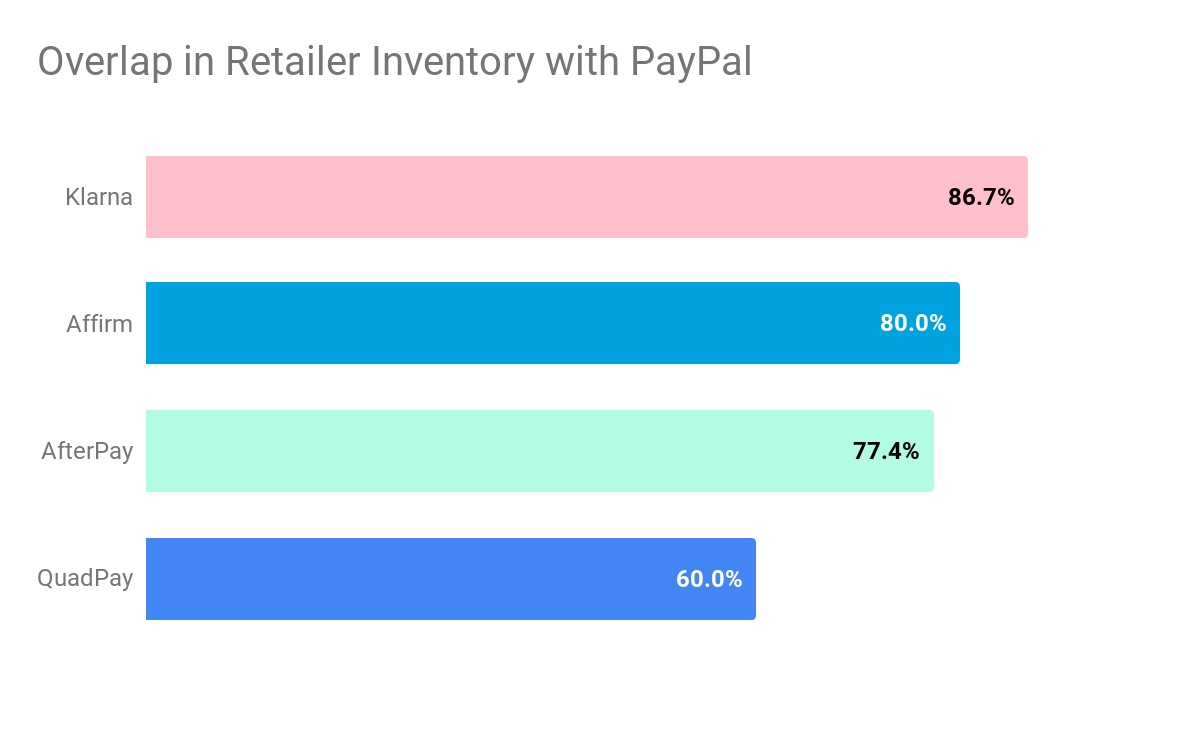

It’s difficult to step out of PayPal’s shadow … the other payment solutions had the following overlap with PayPal of their respective retailer inventory: Klarna (87%), Affirm (80%), AfterPay (77%) and QuadPay (60%).

Image Credits: Buttobn (opens in a new window)

Of the 218 unique retailers where an alternative payment solution was offered at checkout, multiple alternative payment options were available on 50 retailers (26%). PayPal was the only alternative payment option for 155 retailers (71%). PayPal was only not available on 14 retailers (6%).

Image Credits: Button (opens in a new window)

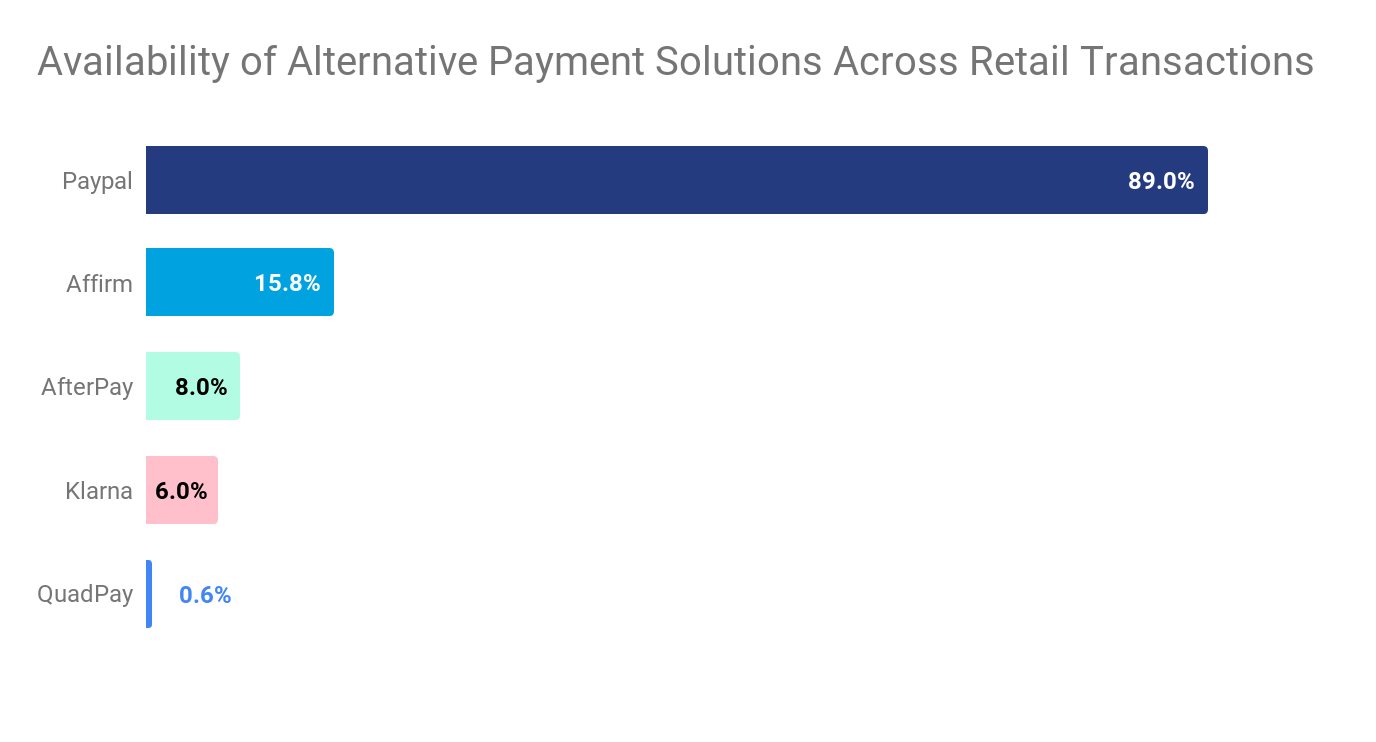

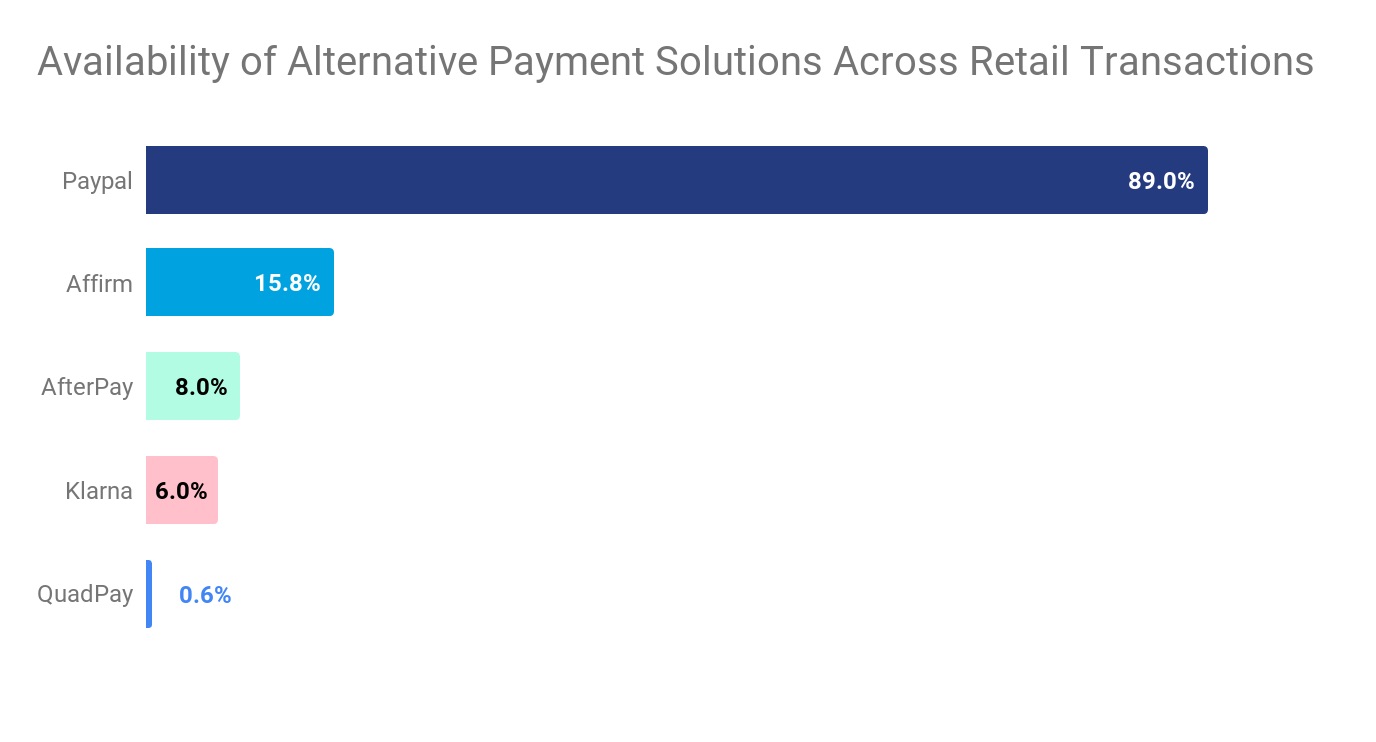

As a result of greater retailer coverage, PayPal was also the most widely available alternative payment solution. It was an option for 89% of all transactions where an alternative payment solution was available. The other payment solutions trailed with the following transaction coverage: Affirm (15%), AfterPay (8%), Klarna (6%) and QuadPay (<1%). No alternative payment solution was available for 3% of the transactions analyzed.

Image Credits: Button (opens in a new window)

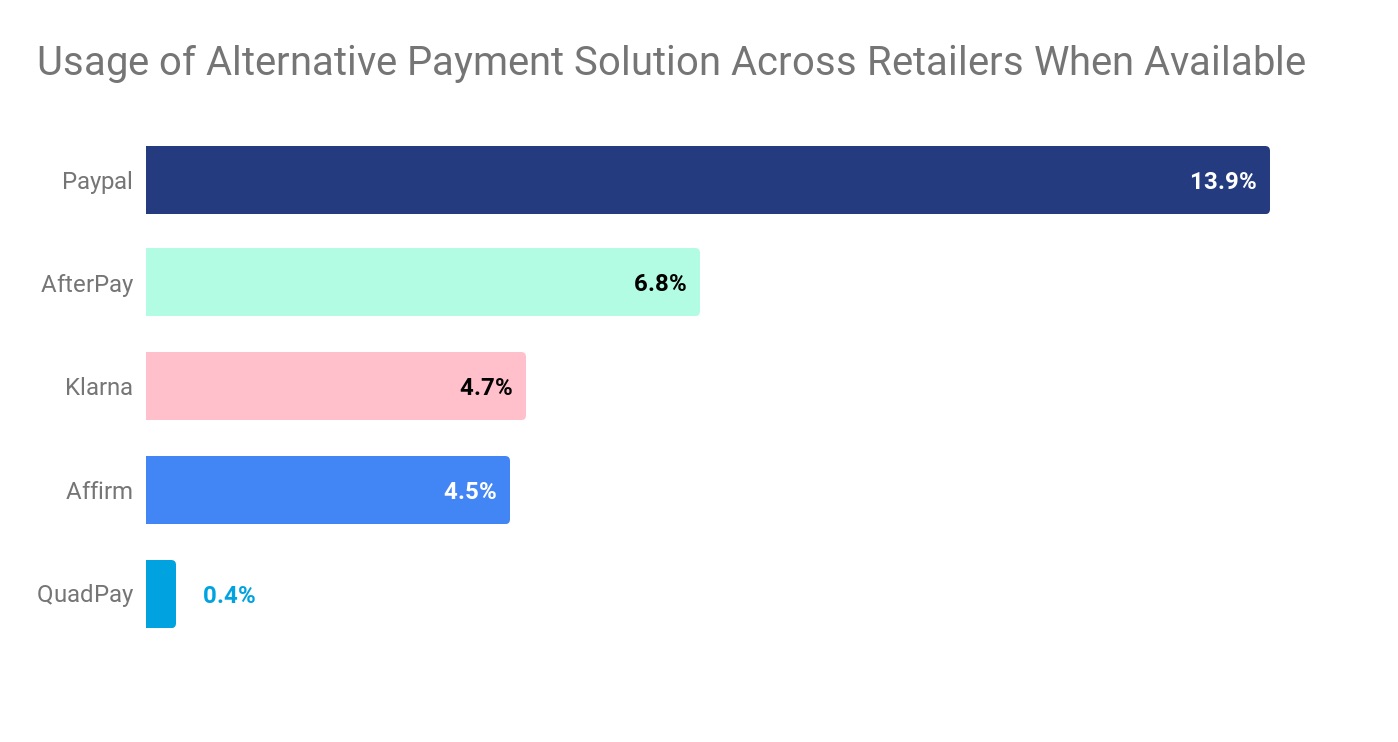

Adoption rates indicate that BNPL is in its nascent stage of adoption. Of their respective potential transactions (i.e., where an alternative payment solution was available), PayPal was the most widely selected at 13%, AfterPay was second at nearly 7%, Klarna and Affirm were both selected for ~5% and QuadPay was selected as the payment method for less than 1% of the transactions when available.

Image Credits: Button (opens in a new window)

While users selecting to pay with PayPal were not necessarily using PayPal’s BNPL feature, PayPal’s widespread market presence is imposing and has it well-positioned to lead the BNPL space going into the 2020 holiday season. The others — AfterPay, Klarna, Affirm and QuadPay — will undoubtedly also benefit from this expected rise in BNPL adoption.

However, their limited product differentiation — all providers offer payments in four installments, interest free — and comparatively limited market coverage suggests that they all must achieve significant increases in retailer coverage and user adoption if any of them hope to compete at scale with PayPal.