Startups Selling To Other Startups: A House Of Cards?

Image Credits:

“Don’t put all your eggs in one basket,” the saying goes. Well, if you’re running a startup that sells to other startups, you might be putting all your eggs in one blender.

B2B companies whose customers are other early stage B2B companies put themselves doubly at risk: Not only are startups failure-prone by nature, but an early stage company with strong fundamentals can still falter if its client base is vulnerable to market corrections.

Recession-proofing a B2B startup isn’t easy, but as fears of a tech bubble grow, it may be necessary for the company’s survival.

A cautionary tale from the not-too-distant past

Back in 2000, Regus PLC, an international real estate company that largely sold to other startups, raced to a valuation of more than $3 billion. Then, the dot-com bubble burst and its client base evaporated seemingly overnight. The company filed for Chapter 11 bankruptcy protection, and now — 15 years later — its market capitalization still hasn’t reached its turn-of-the-century high.

Of course, times have changed since 2000. There are 11 times more people online, e-commerce has grown from 0.6 percent of total U.S. retail spending to 7 percent and big tech companies are sitting on mountains of cash. But, depending on who you sell to, you might be at risk when a correction kicks in (if it hasn’t already).

What happens to B2B startups in a recession

There’s lots of talk about the impending doom in the venture-funding environment; people who agree, people who disagree — but one thing’s for sure: We’re at a 15-year high in venture capital financing volume and there are lots of rumblings of a quieter 2016.

Startups are much more vocal about their successes than their failures.

What will happen if and when startup funding does retreat for some period, and valuations reset? Lots of pre-seed founders will need to find “normal” jobs, many seed-stage startups will fold, a bunch of Series A startups will falter, some Series B companies will retrench and so on. But here’s the thing: Solid businesses with solid financials will persist. The later the stage or the closer to profitability, the likelier a company is to survive.

How I’m recession-proofing my business

When funding streams dry up, many companies stay barely afloat by reining in avoidable expenses. They’ll do away with their office space, lunch caterer, health insurance — and possibly their sales intelligence platform. As a SaaS CEO with many venture-backed customers, I needed to understand these potentially major risks. And even more importantly, I had to make sure our customer base would survive a downturn.

My investment banking experience kicked in, and I devised a quick and dirty framework to figure out how risky our revenues are from different customers and prospects. Which startups should we be trying to get more exposure to, and from which should we ensure we’re diversified? My aim isn’t to call out businesses I think may struggle. I wish every startup the best. But I hope this might help founders like myself seek a healthy and recession-proof customer mix.

In other words, make sure you’re not a Regus, and that Regus isn’t your only customer.

The framework

Perhaps a truly rigorous analysis would involve finding out what percentage of startups “die” at each funding stage or size, segmented by industry or business model. We could then endeavor to avoid overexposure to the segments with particularly high failure rates. Unfortunately, startups are much more vocal about their successes than their failures, so this data doesn’t exist.

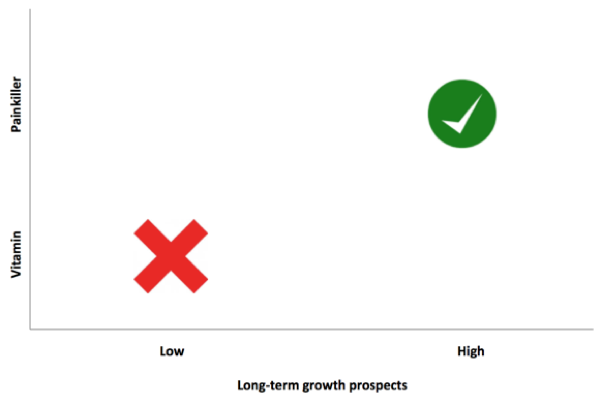

In the absence of that data, for my own analysis, I came up with heuristics for those success and failure rates. I based my prediction of a company’s long-term strength on two factors:

- Vitamin or painkiller: Is the product simply nice to have, or does it address a burning need?

- Customer long-term growth prospects: Do the company’s customers (not just the company itself) have room to grow?

I’ll go into scoring both factors in more detail.

Vitamin or painkiller?

When funding dries up, products that are considered vitamins will quickly lose customers. It’s the painkillers that retain paying customers no matter what. To determine whether a startup delivers a vitamin or a painkiller, I looked at three criteria:

- Cost-saving: Does this product produce meaningful cost savings for the customer? Amazon Web Services (AWS), for example, saves us a lot of money versus owning our own servers.

- Revenue-driving: Does the product have a meaningful impact on the customer’s top line? InsightSquared, a sales analytics company, and Looker, a business intelligence company, both help their customers run their sales and overall business more efficiently, leading to demonstrable revenue gains.

- Sticky: Is the product difficult to remove? Gild, a recruiting and applicant-tracking software; eShares, which provides digital stock certificates; Gusto, a payroll provider; and Zenefits, an all-in-one HR platform, are all sticky B2B products that become ingrained in a company’s operations, and would therefore be painful to displace.

Admittedly, the second criterion applies more readily to B2B companies than to B2C companies, but I think that’s fair; great consumer products, while incredibly valuable and/or addictive, can be abandoned in tough times. Moreover, the third criterion can favor consumer products that have very strong brands. Great products are both sticky and cost-saving or revenue-generating. Here are just a few examples:

- AWS, in addition to saving us lots of money, is very sticky — it’s a pain in the butt to move to a different cloud provider.

- Twilio, an API for business phone and text functionality, is similar: It saves companies lots of money versus setting up their telephony infrastructure themselves and, once integrated, is difficult to replace.

On the other hand:

- UpCounsel, an online marketplace to find lawyers, offers great cost savings, but hasn’t quite figured out how to avoid being circumvented. As a result, it isn’t very sticky (yet!).

- Corporate catering company ZeroCater is a nice-to-have that’s not very sticky. In a downturn, free lunch is one of those benefits that’s likely to be nixed for a while. Through longer-term subscriptions, economies of scale and ancillary services, companies like ZeroCater can become stickier and more like painkillers over time.

Customer long-term growth prospects

The companies whose products are painkillers are more likely to weather downturns. Next, I wanted to estimate how large and durable each startup could become in the future. I scored each company’s “long-term growth prospects” on two criteria:

- Incremental addressable market: How much bigger can customers get? In other words, how much opportunity is left to be captured in the market?

- Proximity to profitability: How close is the customer to being profitable? Again, B2B companies outscore B2C companies, in my opinion for good reason — selling to another B2B company provides more stability than selling to a consumer-facing startup without a clear revenue stream.

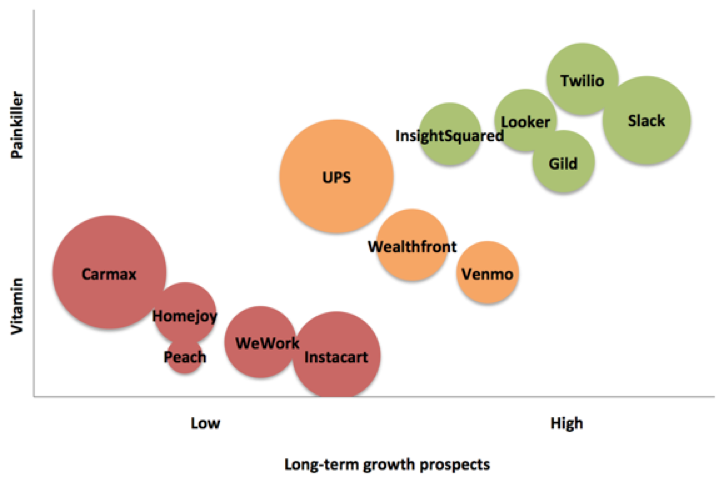

Mobile payments platform Venmo and groceries-as-a-service Instacart score highly on incremental addressable market, because they’re mass-market products. Uber is another example; they were an early Twilio customer and major fuel behind the latter’s growth. On the other hand, large and entrenched companies like UPS and CarMax can be great customers — for the logo, as well as the revenue potential — but they are less likely to fuel your startup’s growth the way Uber did Twilio’s.

With a potential correction in venture funding on the horizon, it’s becoming more important to be thoughtful about your customer mix.

And on the profitability scale, previously mentioned Looker is a SaaS company with, I’m guessing, a healthy LTV/CAC. The path to profitability is clear, although often deliberately delayed in exchange for growth. That’s the kind of customer I want DataFox to have. Instacart, though? Nowhere near profitability, and therefore a riskier customer. All else being equal, I want to target prospects with a clear path to profitability.

On the chart below, you’ll see a few of the examples I mentioned. The critical reader will notice that my framework favors post-Series B enterprise SaaS companies; for my worldview, I think that’s appropriate. There’s a reason the failure rate in SaaS is so low once a company approaches initial scale.

I guess this is why private equity investors look for a diversified client base; it’s risky to be overly reliant on one customer or one type of customer.

Caveats, caveats, caveats

There are so many different types of companies and so many factors that go into each company’s probability of success. My intention with this rudimentary framework isn’t to score companies against each other. If I could actually pick the winners, I’d start a concentrated VC firm! Rather, I want to educate B2B founders — including myself.

How this framework fueled our product development

It goes without saying that I measure DataFox using this same scorecard. It took us a while to get here, but much of our product choices are made with the goal of being both a cost-saver and a revenue-generator:

- Cost-saving: Using DataFox, sales reps can spend 75 percent less time doing customer research. That sort of demonstrable value is hard to argue with, even if funding is tight.

- Revenue-driver: We’re able to alert our customers to new opportunities first, and help them engage on a personal level, leading to more closed deals. Again, we can point to a number that shows customers how we’ve increased their top line.

- Stickiness: For intermittent users of our web application, it’s not difficult to switch us off in a dire situation. Over the past year, we developed a Salesforce integration and API; consistent users will now find it hard to work without DataFox.

- Incremental addressable market: Although we initially targeted financial services, the more we learned from our customers, our customer mix and focus shifted to sales, marketing and other prospecting-heavy use cases like growth equity. Those markets are massive and untapped.

- Proximity to profitability: Most of our customers are financial services firms and B2B companies. We’re relatively certain that, with their strong financials, they’ll continue to stay afloat even in a downturn.

We would have been a pretty risky company to sell to 12 months ago, but by moving toward a painkiller product and healthy customer base, we’re on our way to protecting ourselves against a downturn.

Building your recession-proof customer mix

Many startups, as natural early adopters, are fueling other startups’ growth. With a potential correction in venture funding on the horizon, it’s becoming more important to be thoughtful about your customer mix. There’s still ample time to make sure you’re not stacked in a large, but fragile, house of cards.

If you’re looking for more post-Series B SaaS companies to start diversifying your customer base, this list is a good starting point.