A year after raising $100 million, London-based startup WorldRemit has picked up more funding. To compete against the likes of Western Union in the world of money transfers — and tap a remittance market that the World Bank estimates will be worth $610 billion in 2016 — the company has added another $45 million to its coffers.

This latest round, a debt round from TriplePoint Venture Growth BDC Corp. and Silicon Valley Bank, will be used to expand its business both in developing markets and wealthier, mature regions like the U.S., CEO and co-founder Ismail Ahmed told TechCrunch in an interview. (In other words, WorldRemit is focusing not just on areas where money is sent, but on places where the transfers are originating, too.)

Ahmed and WorldRemit are not disclosing the company’s valuation, but Ahmed describes this as a debt round that “could have been added at the same time as the last round.”

We understand from very reliable sources that the valuation is at the same level it was a year ago — $500 million. (An equity round could have likely shifted the valuation higher.) The funding is coming at a time when it’s getting harder for even the brightest sparks in the startup world to raise, is there in the event that WorldRemit needs it down the line. The company — which has picked up $192.7 million in funding to date from other investors that include Accel and TCV — still has money in the bank from the last round.

In the last year, WorldRemit has been working on licenses to add more sending regions to its network. It is now active in some 40 U.S. states and will be adding more key markets soon (one huge state it has yet to tackle, for example, is California).

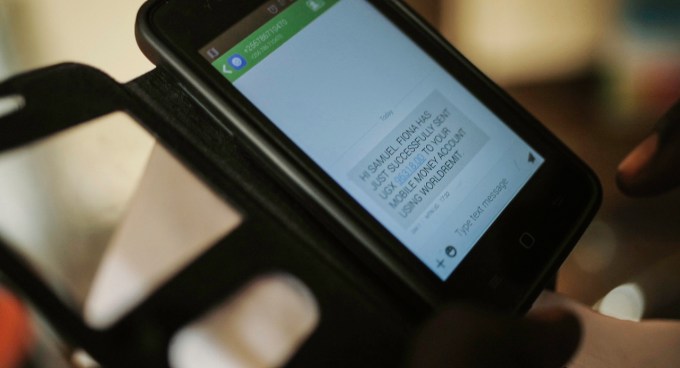

On the receiving end, WorldRemit is focusing on mobile money services: these are the agreements between carriers and mobile money operators that let residents in many developing countries use their mobile numbers (and mobile phones) effectively as proxy bank accounts.

This is a very fragmented area: there are now 25 mobile money services that work with WorldRemit, including large companies like Mpesa and MTN, but Ahmed says that there still another 265 serving emerging markets.

Today, mobile money transfers account for about 25% of all of World Remit’s business (the remaining 75% goes to a variety of other endpoints including traditional banks, cash pick up, mobile airtime top-ups, and even door-to-door delivery where the funds are delivered to someone’s home).

But mobile money is where a lot of the opportunity lies: mobile phones are already being used as the primary medium for long-distance communications with family and friends, and so it becomes a natural platform for sending them money, too.

WorldRemit made $39 million in revenues in 2015. In dollar terms, that represented growth of 56% versus 2014, short of the bullish projections it made in 2015 after pulling $24 million in revenue in 2014 (it made $9.3 million in 2013, growing 168% in 2014). (Update: WorldRemit notes that it’s a Sterling company, based in the UK, so 2014 turnover was £15.2m in 2014 and £27m in 2015. In that currency, WorldRemit actually grew 80% last year, as the pound has just weakened against the dollar.) There is also the issue of wider economic forces, for example the economic downturn, which had an impact on the remittance market, according to the World Bank.

WorldRemit currently averages around 400,000 transfers each month, and it claims that its mobile money market share is the largest of any money transfer service today.

But interestingly, as WorldRemit continues to build out its business in mobile, it may be processing a lot more transactions, but the value of them has been in decline.

“If you look at the number of transactions going to mobile money, they are increasingly getting smaller,” Ahmed says. “Today our average per transaction is around £90, but historically it was £150. The reason why is that with messaging apps, people are communicating with family members more frequently, and so they are sending smaller amounts more frequently.” (This is also one reason why Facebook has explored ways of tying its own Messenger app more closely with remittance services.)

Competition in the market has also led to remittance companies slashing their fees: it was not that long ago that a typical transfer fee was £10 or more, Ahmed says, forcing migrants to send larger amounts in one go. That has been slashed to fees that can be under £1, alleviating the pressure to send quite as much.

That raises another potential pressure for WorldRemit: it’s operating in a crowded market. Apart from incumbents like Western Union and MoneyGram, there are a number of others that are building businesses in the remittance market. They include the likes of Xoom (acquired by PayPal last year for $890 million), Azimo, Regalii, Remitly and TransferWise.

“I think there are a number of companies in the money transfer but when you are looking specifically at companies targeting emerging markets like we are, there are really only a handful of bigger players, and I think we are the most global,” Ahmed says.

This reach and purpose of targeting underserved areas is what has helped WorldRemit stand out with investors, too.

“It is exciting to be involved with a service that delivers real benefits to people around the world while demonstrating impressive business growth,” said Sajal Srivastava, President of TriplePoint Venture Growth BDC Corp., in a statement. “WorldRemit represents what the FinTech revolution has to offer: innovation, empowerment to individuals and new opportunities to the financial services industry.”

“Operating across the world gives WorldRemit diversified revenue streams and a huge customer base,” said Phil Cox, Head of EMEA and President of UK Branch, at Silicon Valley Bank. “This is a great story of tech for good – the social impact of connecting remittances to Mobile Money services in the developing world has been huge and looks set to continue.”

Updated with more detail on revenue growth and currency clarifications.