Editor’s Note: Ben Narasin is president of TriplePoint Ventures, the seed equity practice of TriplePoint Capital, and a freelance writer. Jeremy Abelson is the Founder and portfolio manager of Irving Investors.

The warning flags are flying and discussions of inflated private company valuations are en vogue, but the concerns from investors may be premature. The sky isn’t falling… yet.

Bill Gurley, a partner at Benchmark Capital, spoke at SXSW last week and again gave us the advice that “we are in a risk bubble.”

Gurley blames this on “institutional public investors…rushing into this high-stakes late-stage game,” and warns that “Silicon Valley’s optimism could lead to the death of so-called “unicorn” companies.”

The Wall Street Journal created their “Billion Dollar StartUp Club,” which lists these 78 unicorns that have received investments at valuations over $1 billion. Steve Case claims the “late stage market has gotten frothy,” and Marc Cuban has gone so far as to say that “this tech bubble is worse than the tech bubble of 2000.”

We wanted to understand whether the declarations and warnings were warranted so we turned to the data of late stage investing returns (we rely on the trends in the data to support our thesis).

First, we don’t think that pundits are saying these are bad companies at all. Instead they’re warning that they are bad investments at these levels… which means they believe these valuations are unsustainable in the public markets.

Implicit in the idea of a bubble is that it will burst; and in this specific case what will burst are the returns from late stage investments.

To assess this claim, we need to assess the implications of the term “bubble.”

Implicit in the idea of a bubble is that it will burst; and in this specific case what will burst are the returns from late stage investments. The Valley doesn’t do dividends, so late stage investors generally don’t realize returns until liquidity events (such as a sale at lock-up expiry or an IPO or an acquisition).

The bubble claim then implies that these companies will have an initial public offering and trade after their lock up expires at significantly lesser valuations than their last private round.

Thus far, we haven’t seen anyone present data supporting this bubble claim. So we went digging. To evaluate this trend, we studied three key metrics measuring the actual returns of companies that have successfully listed on one of the US exchanges.

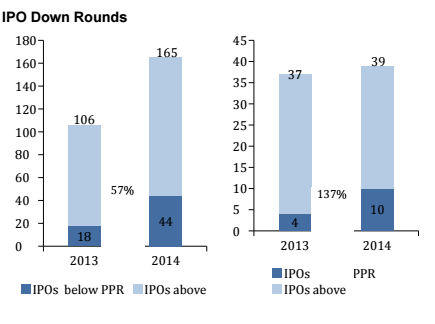

1. IPO Down Rounds (IPOs at a lesser valuation than previous private rounds):

44 out of 165 IPOs in 2014 were down rounds, a 57% increase over 2013 which had 18

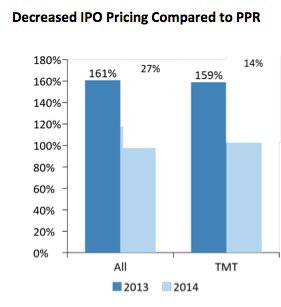

2. IPO Price Premiums:

IPO’s priced 27% lower relative to their last private round between 2013 and 2014. In 2013, the average IPO pricing premium relative to the last private round was 161% compared to a 118% premium in 2014.

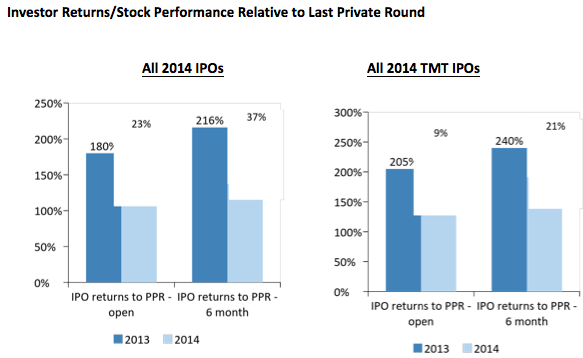

3. Investor Returns:

Investor returns, from the prior private round to the stock price six months post-IPO, decreased to 137% in 2014 compared to 216% in 2013, a 37% decrease.

The data shows that yes, the inflation trend is real and returns from late stage investing are decreasing, but the whistle blowers are overlooking some of the facts…most notably, these investments are still wildly profitable.

Investor returns, from the latest private round to an exit at the expiration of a lock-up, did decrease by 37% between 2013 and 2014, but they still realized 137%. The results are even bigger in the “Technology, Media and Telecommunications” sector (TMT), which showed a return of 191% in the same period. All this with companies in the data set going public an average of 20 months after their last private round.

Not only will there not be a bursting of the bubble, but we won’t see a reversal in this trend for a while.

Why The Trend Exists: Silicon Valley Vs New York,

Silicon Valley contends that mutual- and hedge-funds (aka New York Money aka “Dumb Money”) paying up to buy “pre-IPO” companies are inflating valuations beyond logic. The Wall Street Journal lists Tiger Global and T.Rowe price as two of the 5 top investors within the Billion Dollar Startup club — ahead of Andreesen Horowitz.

To understand this discrepancy in “logic” you must understand return expectations. According to Morningstar, mutual fund investors experience [annualized] 5-12% returns where VC investors shoot for a 3-10x (300% – 1000%) return… there’s quite a gap there. With 137% returns in an approximately two year period, there’s logic in mutual funds continuing to throw big dollars into strong IPO candidates, thus significantly inflating valuations. With this encroaching competition it’s not surprising then that VC’s are sending the warning.

Why Will It Continue?

Clearly, returns from these late stage investments have been multiple times better than broad mutual fund performance and have also been much better than investing in the same companies once they IPO through the public markets.

These big “East coast funds” are crossing over into private rounds with capital historically allocated to public stock portfolios. These funds have an interest in becoming long-term shareholders…well past the IPO or lock up expiry. This crossover is also motivated by institutional public investors’ inability to get a large enough allocation of stock through an IPO, especially in the most exciting tech companies.

With 137% returns in an approximately two year period, there’s logic in mutual funds continuing to throw big dollars into strong IPO candidates, thus significantly inflating valuations.

Their new strategy has become to first own stock from a private round, then participate in the IPO and finally, fill the balance of the desired position in the open market.

Although, compared to 2013, these returns are shrinking, and IPO down rounds are increasing at a meaningful rate, these trades remain highly logical and will continue until the returns are exhausted.

Lets Discuss The Risk

New Relic, HortonWorks, and Box are the recent poster children for IPO down rounds. In a Bloomberg article, Serena Saitto and Leslie Picker claim these companies are representatives of the “risky outcome” of late stage investing and the “disconnect between the valuations of [private] companies and publicly traded ones.”

For supposed losers, late stage won’t necessarily even lose money on these investments. They have all traded well above their private valuations at their highs and they are not far off from them now. If you own an equivalent position in all three from their last private rounds, you are down ~5%… That’s 5% for the big headline losers of 2014.

You could point to the fire sale of Fab.Com for $15MM. Not a great return on the once $1 billion company. This basically 0% return is not relevant to this conversation, because there are always going to be zeroes in private company investing. Whether you bought stock at $1B, or $750 million or $60 million, you still hit a zero. A company going to zero is not a symptom of a bubble or inflation – bubble or no bubble, investors need to make a call on the long term sustainability of a business. In this case (in hindsight of course) investing at any level was a mistake, but that’s always part of the game with private investments.

2000 Vs 2014 – The Bubble

A comparison of 2000 and 2015 is moot – today investors are valuing companies on revenues, future earnings or, in the case of a few, the ability to just flick the monetization switch (i.e Instagram, Snapchat, etc). In 2000, however, investors were valuing companies on users and page views. We view this as a fundamental difference.

Public valuations are also much more sensible now: On CNBC, Amanda Drury stated that in 2000, the average tech IPO came to market at 32x revenues compared to 6x in 2014. In 2002, the NASDAQ was trading at 120x multiple of earnings sales and is at 26x today.

While we should continue to monitor these trends, the comparison to the actual bubble of 2000 needs to be put out to pasture.

The Analysis

We looked at disclosures in S-1s (SEC filings) for prior private valuations and explored historical trading data from Bloomberg. We included transactions based on common stock or convertible preferred stock (includes all share purchases including related party transactions). Trading data as of 2/15/15 used for companies with less than six months since their IPO.

IPO down rounds were defined as companies with a prior higher private valuation (not necessarily most recent). Pricing premium and returns data were based on the most recent round. Some data was excluded when it was not meaningful or the companies were outliers. The following IPOs were excluded: IPOs related to REITs; IPOs without transactions in their stock; convertible preferred stock or options prior to the IPO; Master Limited Partnerships (MLP), Limited Partnerships (LP), closed end funds, and mutual conversions.