Loop is a new mobile payments startup making some fairly big claims. The company says it has invented a technology that lets you pay with your phone at nearly any point-of-sale across the U.S., without requiring merchants to upgrade their hardware. Nor do you have to own a particular device, like those NFC-based smartphones required for mobile payment services like Google Wallet or Isis. Instead, consumers can either use a dongle plugged into their smartphone or a special charge case that is simply held close to the magnetic stripe reader (the place you swipe your credit card) at checkout. Seemingly like magic, the payment processes as if you had swiped your card as usual.

If mobile payments were this easy, though, why hadn’t someone launched technology like Loop’s years ago? The answer has to do with how complicated the payments industry is, as well as the challenge that lies in changing consumer behavior on a broader scale.

But Loop co-founder and CEO Will Graylin thinks they’ve figured it out. Graylin has an extensive background in the industry, having previously founded others in the mobile and payments space, including WAY Systems (sold to VeriFone) and ROAM Data (sold to Ingenico), among others. Loop’s other co-founder and chief technologist, George Wallner (Hypercom founder), meanwhile, was a pioneer in the early days of magstripe technology.

But Loop co-founder and CEO Will Graylin thinks they’ve figured it out. Graylin has an extensive background in the industry, having previously founded others in the mobile and payments space, including WAY Systems (sold to VeriFone) and ROAM Data (sold to Ingenico), among others. Loop’s other co-founder and chief technologist, George Wallner (Hypercom founder), meanwhile, was a pioneer in the early days of magstripe technology.

At ROAM Data, which Wallner also invested in as he has now done with Loop, the company was in the business of supplying Square’s competitors with similar dongles for mobile point-of-sale solutions, including names like Intuit, PayPal, and PayAnywhere, for example.

Working together on various companies for a decade or so, the two came together to focus their efforts on the mobile payments space from the consumer side, following Ingenico’s takeover of ROAM Data.

“At ROAM Data, we were thinking about mobile commerce as a platform – not only mobile POS, but also mobile checkout, mobile promotions, and mobile wallet,” says Graylin. All the pieces need to work together to close the loop, he explains. They also were thinking about NFC and why that technology hadn’t yet taken off, and realized that asking merchants to change things on their end was the problem.

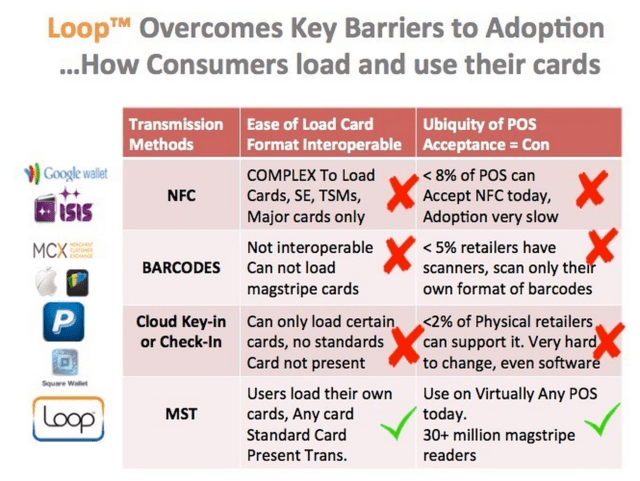

The trick, the founders believe, is in using the POS systems and technology already out there, then getting the consumer on board with their proposed solution. “The one common interface is the magstripe reader, but that was never meant to be a contactless reader,” says Graylin.

But Wallner came up with a fix to that problem. He engineered a way to induce a strong-enough magnetic signal to emulate the same signal you would get when you moved the magnetic stripe across the reader by swiping your credit card at checkout. Wallner got this contactless magstripe transmission to work in late 2012, calling it Magnetic Secure Transmission, or MST for short.

For those interested in the physics of the technology, a quote from the company’s Kickstarter page helps to fill in the blanks:

MST technology generates changing magnetic fields over a short period of time. This is accomplished by putting alternating current through an inductive loop, which can then be received by the magnetic read head of the credit card reader. This signal received emulates the same magnetic field change over time as when a magstripe card is swiped across the same read head. Loop works within 4 inches from the read head; the field dissipates rapidly beyond that point, and only exists during a transmission initiated by the user (as opposed to NFC).

It’s not hogwash. We spoke off record to other magstripe experts with no horse in the race, so to speak, to get their thoughts. And they admit that, technically speaking, the system works. It does work. Testers are using the system, which is live right now.

MST works nearly anywhere magstripe is accepted, except in a few locations, like gas pumps or ATMs where the reader is encased deep in plastic or requires you insert your card (such as when it sucks in your card for you) in order to trigger a switch that turns the magstripe reader on. A few older PC-based point-of-sale software solutions will also be exceptions. But overall, Loop works at over 90 percent of the point-of-sale terminals used in the U.S. today, without any changes to the hardware on the merchant side, or a phone upgrade on your part (beyond buying Loop’s accessories).

But when it comes to payments, things aren’t quite as simple as getting things to just function.

SECURITY

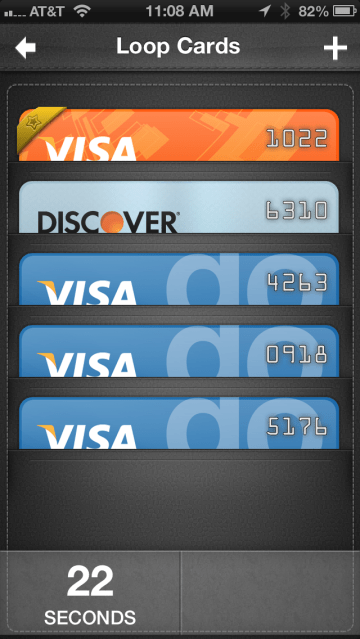

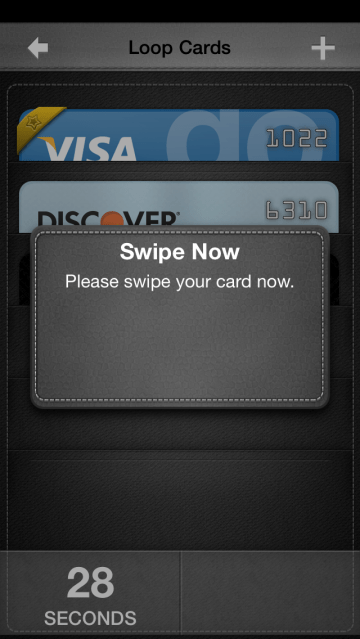

First of all, there’s the security problem. Loop sells a smartphone dongle called the Loop Fob, which allows consumers to load their payment cards into their mobile wallet (a smartphone app installed on the phone). To prevent thieves from using the dongle as a skimmer, the company first has to bind the device to a user’s Loop account. That is, when a card is loaded by swiping it through the dongle – similar to the way you’d swipe when paying with Square – Loop checks the name on the card with the name on the Loop account on the phone. This prevents someone from simply grabbing people’s wallets and quickly loading the victims’ payments cards into their own Loop app on their phone.

Once authenticated, the card data is stored encrypted on the Loop device, be it the dongle or the other Loop product, ChargeCase, a Mophie-like case that serves both as the payment mechanism and as a way to keep your phone’s battery juiced throughout your day.

Once authenticated, the card data is stored encrypted on the Loop device, be it the dongle or the other Loop product, ChargeCase, a Mophie-like case that serves both as the payment mechanism and as a way to keep your phone’s battery juiced throughout your day.

The keychain dongle ($34) and ChargeCase ($99, 1200 mAh battery) will ship in Q1 2014, and a premium ChargeCase shipping in Q2 (1500 mAh battery and much thinner) will follow. Another product will be a Bluetooth LE-enabled plastic card that can be handed to cashiers for swiping when their POS system is behind the counter. (Assuming they’ll do that for you instead of giving you the stink eye.)

In addition to holding your mobile cards loaded through the dongle, the Loop mobile app is similar to something like Lemon Wallet, as it also lets you snap photos of other cards you carry around in your physical wallet, like ID and membership cards, gift cards, or even those keychain tags with the printed barcodes.

At point-of-sale, you hold your phone near the reader and press the “transmit” button on the Loop device or software. The system is in field trials now and will launch near year-end when Loop devices start to ship.

INDUSTRY ACCEPTANCE?

But even with the security in place and the technology functioning, there’s still the issue of getting the rest of the industry on board with the solution. In the payments world, a transaction where a card is not swiped is considered a “card not present” transaction, and merchants have to pay higher rates because of the increased possibility of fraudulent transactions. While for now, something like Loop works as a “card present” transaction because it’s essentially tricking the POS hardware into thinking a card has been swiped. But if this grew in popularity among consumers with official industry acceptance and standardization, the industry players – card issuers, banks, even retailers – could eventually figure out a way to fight back.

But Graylin is no spring chicken here. He knows he can’t go it alone. “We’re working with card issuers that want to provide this as a safer and more convenient solution for their card holders,” he claims. Though he can’t provide their names due to NDA agreements, he says Loop is in discussions with some of the largest issuers in the world. And they’re even talking with those making the incompatible gas stations POS readers about a software solution. “We’re industry veterans,” Graylin admits. “We’re just going after the grassroots feel.”

$10 MILLION SERIES A UNDERWAY

He explains that the $100,000 they’re “raising” on Kickstarter is not about the money, it’s about gaining access to the “world’s largest focus group” and getting early feedback from beta testers.

Graylin and Wallner have already put a couple of million of their own money into Loop, and are in the middle of raising their first outside round — a $10 million Series A — from the same angels who have invested in their previous companies. They also already have 25 employees and 15 contractors working in their Boston headquarters, as well as in California, Florida, Denver, and even in China (to handle the manufacturing and hardware side of the business).

EMV TO DOOM LOOP?

And to address the elephant in the room, yes: they know that the U.S.’s transition to EMV (chip cards, a replacement for magstripe technology, like what’s used in Europe) is only years away. The U.S. is supposed to switch by 2015). Graylin first points out that terminals accepting magstripe will still be around for a long time, and is also skeptical the deadline will be met.

Still, it’s a problem for Loop: after consumers receive their EMV-enabled cards, they won’t be able to swipe them (or trick terminals into “swiping” them via Loop) when at an EMV-enabled POS system.

Still, it’s a problem for Loop: after consumers receive their EMV-enabled cards, they won’t be able to swipe them (or trick terminals into “swiping” them via Loop) when at an EMV-enabled POS system.

For Loop, getting past this particular hurdle is the difference between creating a clever, but ultimately transitional mobile payments solution, and one that fundamentally changes the way consumers pay at point-of-sale. And to be clear, that’s something that no one, not Apple, Google, Visa, MasterCard, banks, carriers, or other startups (excluding to some small extent Square, with its say-your-name-at-checkout feature) – have managed to do.

So what’s the plan?

“We found a new interface with the magstripe reader in such a way that the transmission to that magstripe reader can now be dynamic. We can even add the level of security that’s much stronger than even the magstripe that’s on your plastic,” Graylin says. He claims also that the major card issuers are now working with Loop to create a dynamic mobile card. They’re asking Loop if there’s now a way to dynamically encrypt (tokenize) the data so they can use the same transmission means (the magnetic interface) for these mobile cards.

Discussions, however, are not commitments. Everything is under NDA and in early stages of exploration for now. There’s the potential that the issuers will buy in, because this could offer them something they want — a way to communicate with consumers via their phones, to say things like: “thanks for your business”; “here’s an offer or deal”; “check your balance”; and so on.

Getting the issuers to do this would be a selling point for consumers, too, who today may not see an advantage in using Loop over just swiping a card. But if their payment cards became interactive, mobile cards while still secured in a PIN-protected app, that might be worth something. As would be the merchant deals platform that could potentially follow.

There’s still the very real risk that Loop will not fully convince the key players that its solution is not only as good, if not better, than EMV, but can effectively work beside EMV, too, even as the U.S. transition occurs. And if it can’t, then Loop has a shelf life that will ultimately expire.

But for a mere $35 – $99+, depending on your device preference, you can at least enjoy a couple of years where you can pretend to live in a modern world where phones work like credit cards, before all the rules and regulations get in the way.