A year ago we modeled out the true value of various social networks based on the idea that users in high-value online advertising markets like Japan, the UK and the U.S. were worth more (financially speaking) than those in lower value online advertising markets. Facebook had recently become the largest worldwide social network in terms of users, but based on our model MySpace was still by far the most valuable social network.

We’ve now remodeled social network valuations based on current user numbers and Facebook’s most recent $10 billion valuation. The results are dramatically different.

Based on the original year-old model, if Facebook was worth $15 billion (their then-current valuation), MySpace, with far more U.S. users, was worth nearly $20 billion:

Our model takes Comscore data for available countries and regions. We’ve graphed each of 26 well known social networks with the data we have been able to collect. We’ve then calculated the average advertising spend (estimated by PriceWaterhouseCoopers in a recent report) for each person online in each of those countries. For example, in the U.S., the total 2008 estimated Internet advertising spend is $25.2 billion. We’ve divided that by the number of people online in the U.S. according to Comscore (191 million), to get an average Internet spend per person of $132. View the raw data and calculations here.

The U.S., by the way, is only the 4th most valuable market per Internet user, trailing The UK ($213), Australia ($148) and Denmark ($144).

We’ve then multiplied the average Internet spend per user in each market with the number of unique users each social network has in that market, essentially creating a “weighted average” based on the advertising dollars chasing users. If a social network has more users in the U.S., Japan, the UK, Germany, Australia, and other bigger advertising networks, they will have a higher weighted average valuation.

We believe this model is an effective way to rank various competing social networks. It bumps down networks like Orkut and Friendster who have tens of millions of users in markets with very little advertising spend, and bumps up networks with lots of users in higher value markets.

Based on this model, MySpace is by far the most valuable social network. Second place Facebook has just 75% of the value of MySpace (even though it now has more users), followed by Bebo (26% of MySpace value), Hi5 and Amebio. LinkedIn comes in at no. 11, at 6% of MySpace’s value.

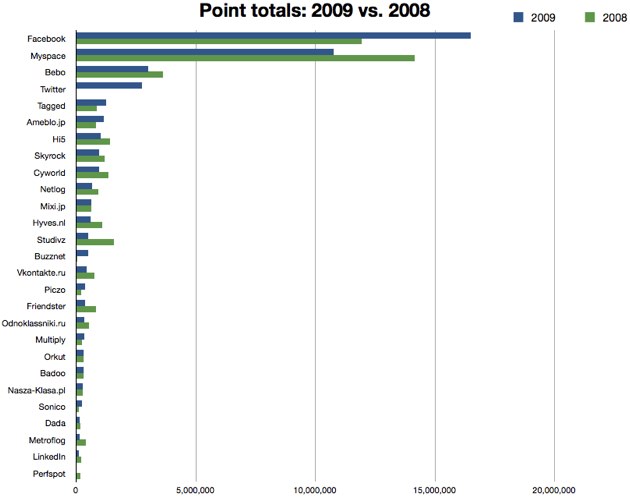

The new model takes into account the dramatic rise of Facebook usage over the last year, the massive recent decline in MySpace usage, and less dramatic changes in the other social networks. We’ve also modeled out the various valuations with the old Bebo ($850 million) and LinkedIn ($1 billion) valuations as pivot points. We’ve also added Twitter to the list just for kicks.

The bottom line: If Facebook is worth $10 billion today, MySpace is worth just $6.5 billion. Bebo is worth $1.8 billion, Twitter is worth $1.7 billion and LinkedIn is worth $0.8 billion. Facebook also accounts for 37% of all social networking value points in our model. Another way of saying this: If Facebook is worth $10 billion, the value of the entire social networking industry is $27.1 billion.

Lots of charts and graphs below. The full model is here if you want to look at all the data (I recommend zooming unless you have super vision). Thanks to TechCrunch intern Dan Romero for running the new model.