Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today, we’re weighing a standard bit of startup wisdom that recently reemerged against some surprising, contrasting evidence. Does too much money hurt a startup more than it helps, or is that standard view actually mistaken? We’ll start with the traditional view, which was re-upped this month by venture capitalist Fred Wilson, along with some supporting arguments proffered by a Boston-based venture firm.

Afterwards, we’ll dig into a grip of contrasting data that should provide plenty to chew on over the holidays. Ready?

Fit to burst

Union Square Ventures‘ Fred Wilson wrote earlier in December (citing an excellent Crunchbase News piece by occasional TechCrunch contributor Jason D. Rowley) that he was curious if startups that raise huge ($100 million and greater) early-stage rounds do better or worse than their cohorts that raised only smaller sums.

Underpinning his question is Wilson’s belief that “performance of VC backed companies is inversely correlated to how much money they raise.” This makes good sense. And if anyone has enough anecdotal evidence to support the view, it’s Wilson who has been a venture capitalist since the late 1980s.

The idea that too much money is bad for startups isn’t hard to understand: startups need to focus and run fast; too much money can lead to both bloated operations, diffuse product direction and useless dalliances in cruft.

Startups also die when they have too little money, of course. But the concept that there is a midpoint between insufficient funds and an ocean of capital that is optimal has lots of credibility amongst the venture class. (I believe this is my favorite phrasing of the concept, that “more startups die of indigestion than starvation.”)

A 2016-era TechCrunch article written by some of the folks from Founders Collective makes the point plainly:

By examining the technology IPOs of the past five years, we found that the enriched (well capitalized) companies do not meaningfully outperform their efficient (lightly capitalized) peers up to the IPO event and actually underperform after the IPO.

Raising a huge sum of money is a requirement to join the unicorn herd, but a close look at the best outcomes in the technology industry suggests that a well-stocked war chest doesn’t have correlation with success.

In the spirit of fairness, I’ve long agreed with the above views.

My views on the question of too much money ruining organizations came from a different field, but are worth sharing for context. My father once told me an analogous story about a small poetry magazine, a publication that operated on the proverbial shoestring and was always weeks away from shutting down. But it limped along, barely keeping the lights on as it produced brilliant work.

Then, someone died and left the magazine a pile of money in their will — but the sudden influx of capital wrecked the publication and it eventually shut down.

In many cases, raising too much money too early can hurt a team or cause it to lose track of its mission. But for tech startups, on average, is that really correct?

Maybe not

We aren’t going to solve this issue today, and I don’t want to say that we’re proving Wilson and company wrong. However, there is a fascinating set of data that I want to highlight, as it pushes back against what we think we know.

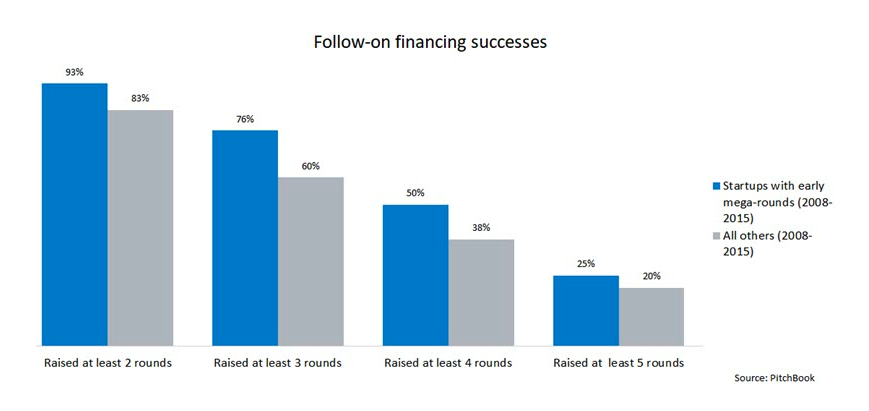

The folks over at Pitchbook put together an incredibly interesting dataset making the case that startups which raised $100 million or larger rounds while they were early-stage wound up having more fundraising success later on:

It’s not a huge improvement over competing cohort members that raised smaller rounds. But it’s not negative, which goes against venture capital conventional wisdom and against what I figured was common sense on my side. It appears that, at least in the current era, raising huge rounds early isn’t that bad for your company in terms of raising more capital.

But what about exits? Do early super-giant rounds harm the chance that a startup exits? Not really, what the rounds do instead is lower a startup’s chance of being acquired while raising the chance of it going public.

Looking at U.S. startups that raised both Series A and B rounds between 2008 and 2015, here’s the Pitchbook data:

- % acquired, raised early supergiant round: 14%

- % acquired, did not raise supergiant round: 25%

- % that went public, raised early supergiant round: 15%

- % that went public, did not raise early supergiant round: 2%

That’s an exit rate of 29% for startups in the group that did raise a huge, early checks, and 27% for those that did not. Given that an IPO is nearly always better than an acquisition in terms of dollar scale, the data is even more skewed in the direction of super-giant, early-stage rounds being good? And not bad?

Wild. I would have bet you lunch that this would not have been the way that the data would bend.