Five years ago, Dynamic Yield was courting an investment from The New York Times as it looked to shift how publishers paywalled their content. Last month, Chicago-based fast food king McDonald’s bought the Israeli company for $300 million, a source told TechCrunch, with the purpose of rethinking how people order drive-thru chicken nuggets.

The pivot from courting the grey lady to the golden arches isn’t as drastic as it sounds. In a lot of ways, it’s the result of the company learning to say “no” to certain customers. At least, that’s what Bessemer’s Adam Fisher tells us.

The Exit is a new series at TechCrunch. It’s an exit interview of sorts with a VC who was in the right place at the right time but made the right call on an investment that paid off. [Have feedback? Shoot me an email at lucas@techcrunch.com]

Fisher

Fisher was Dynamic Yield founder Liad Agmon’s first call when he started looking for funds from institutional investors. Bessemer bankrolled the bulk of a $1.7 million funding round which valued the startup at $5 million pre-money back in 2013. The firm ended up putting about $15 million into Dynamic Yield, which raised ~$85 million in total from backers including Marker Capital, Union Tech Ventures, Baidu and The New York Times.

Fisher and I chatted at length about the company’s challenging rise and how Israel’s tech scene is still being underestimated. Fisher has 11 years at Bessemer under his belt and 14 exits including Wix, Intucell, Ravello and Leaba.

The interview has been edited for length and clarity.

Saying “No”

Lucas Matney: So, right off the bat, how exactly did this tool initially built for publishers end up becoming something that McDonalds wanted?

Adam Fisher: I mean, the story of Dynamic Yield is unique. Liad, the founder and CEO, he was an entrepreneur in residence in our Herzliya office back in 2011. I’d identified him earlier from his previous company, and I just said, ‘Well, that’s the kind of guy I’d love to work with.’ I didn’t like his previous company, but there was something about his charisma, his technology background, his youth, which I just felt like “Wow, he’s going to do something interesting.” And so when he sold his previous company, coincidentally to another Chicago based company called Sears, I invited him and I think he found it very flattering, so he joined us as an EIR.

And really only at the very end of his residence did he come up with this idea that would become Dynamic Yield. He came about it very much focused on the problem he saw with publishers being outwitted by ad buyers. He felt like all the big publishers really didn’t understand their digital businesses, didn’t understand their users, didn’t understand how performance ad buying was working, and he began to build a product that could dynamically optimize a publisher’s website to maximize revenue, hence the yield … the dynamic yield.

But very quickly, we told him, ‘That’s interesting, but we’re not sure how big that market is. And, you know it’s not always great to sell to those kind of weak customers. Sometimes they’re weak for a reason.’

Adam Fisher: It’s hard in the early days to say no to customers that are willing to pay you money

And he agreed, but at this point, he was asking for seed money to get started. And so we were happy to do that. It’s never easy for a big fund to do a seed deal. At least at the time, it was a lot harder. You know, we got a little bit of pushback, because the idea wasn’t thrilling, but we loved Liad and we said, ‘Yeah, we want to support him. And let’s just try to kind of give him a bit more direction, where we think we would be more interested.’ And we agreed to lead that round, but we told him ‘Listen, you really need to expand beyond publishing to e-commerce and SaaS, there’s much more to be done in terms of dynamic optimization.’

What is Dynamic Yield?

- The startup is a little bit like an adtech platform without ads. It learns about the users who are visiting customer sites and then instead of surfacing external advertising, the platform shifts the actual site content being presented to the user. This could be suggestions of things to buy or videos to watch, the key is that the otherwise static site or app is able to give the visitor an experience that’s customized by machine learning. The company talks a lot about “personalization,” something that is often taken for granted on sites like Amazon where suggestions often lead to transactions but it’s an ethos that’s largely absent across other websites.

Agmon told TechCrunch his founding idea back in 2014: “The trigger of starting Dynamic Yield was the introduction of the paywall in The New York Times. We asked ourselves – why do they arbitrarily block access to the site after 20 page-views? What if I have a strong Twitter following, and every time I share an article, I actually drive a lot of traffic to their site? By delivering real value, shouldn’t I be treated a bit different than other users?”

Lucas: How strongly was Liad holding to the original concept? Did you feel like you had to convince him to make this transition?

Adam: The challenge in these types of situations is one in which you have a lot of customers to choose from. And it’s hard in the early days to say no to customers that are willing to pay you money. And that’s honestly what it requires.

We could see where it was going, we could see that these customers — boy, they really don’t know anything about their business. There’s nothing good to say about that, you know, you always say you never want to be the last thing between your customer succeeding and going bankrupt, that’s just not an enviable position to be in.

And so he knew that, but it just took a bit longer to literally start saying no to publishers, like we’re not going to sell to you anymore. We didn’t drop customers, but we stopped signing them unless they were massive publishers.

Lucas: It sounds like you’ve been at this a while, but how did you get into tech investing in the first place– were you an entrepreneur?

Adam: No I belong to — I guess — a unique class of VC that just started in VC.

Lucas: They do exist!

Adam: Well more and more so I would say, you know, I really got in at the ground floor. Because in 1996, when I started interning at a venture capital fund in Israel, the industry was just getting started. I mean, the funds may have been in existence for a few years, but nobody really knew what they were doing.

I was an American who brought something a little bit different to the table — an ability to come from the outside, learn very quickly, bridge certain cultural gaps, and I kind of fell in love with the sector and obviously with the Israel side of it.

The State of Israel

Lucas: So as the American looking in, what’s the relationship between Silicon Valley and Israel look like these days?

Adam: So I think anybody who’s an experienced VC and invests across multiple sectors will tell you that outside of the Valley, Israel is probably the hottest spot in terms of just the breadth of companies and the blend of companies that you see. For pretty much every sector, any kind of company you would see coming out of the Valley, you could find coming out of Israel. Those companies are then built differently — that I will concede — but in terms of what they’re doing, and the market opportunity, they are remarkably similar.

So that’s what Israel looks like. And from the outside, everybody has their own impression of what Israeli high tech may be, maybe they think a lot in terms of cyber security or semiconductors, or maybe some consumer apps like Waze and Wix and Fiverr, but it’s really broad.

It’s enterprise software. It’s enterprise infrastructure. It’s fin-tech. It’s digital print. It’s very broad.

And that’s what makes it a great match for me at Bessemer, because there’s literally nothing we see in the US that we don’t see in similar startups in Israel, that also makes it very helpful for me to know how these Israeli startups compare to the things we’re seeing elsewhere.

Lucas: So how are these startups built differently? And how does that impact early-stage versus later-stage investments?

Adam: So I would say that the first thing is that most Israeli entrepreneurs come from a technology background, at least the majority of the co-founders come from a technology background, they almost always have a technology bet, they try to differentiate on technology, as opposed to differentiating on product, or go-to-market.

Adam Fisher: The company had its tough moments for sure … But, you know, it ended up with a surprising and, obviously, happy ending

That’s a generalization, but on average, you will find that they’re probably taking bigger risks than your typical US company in the sense that they’re taking a longer time to develop a product, likely because that product is probably trying to do too much. It’s not focused enough. That said, my experience has been that when it comes to a US company versus an Israeli company developing the same product, the Israeli company will do it more efficiently with less capital.

But that’s not always an apples-to-apples comparison, I think a lot of times Israeli companies are over-engineering their product. The whole notion of MVP [minimum viable product] is… I don’t want to say it’s new here. But there’s some lag time, let’s just say that. And that’s why sometimes the companies take a bit longer in their gestation period. The other thing is that, that efficiency generally continues when they’re building their business. We don’t have the equivalent of “blitzscaling” in Israel.

We have much more capital to access than we have ever had and that is changing the landscape here. But it’s still a fraction of what you find in the US. And in addition to that, even if we had the capital, you know, all that money would probably be spent on on a US presence and on US sales reps or on marketing in the US. So it’s a bit unnatural, I think, for most Israeli companies to to raise those amounts and spend those amounts. The net result being, yes, we don’t always have as big or the equivalent-sized exits as in the US. But they’re still great, they are much larger than they’ve ever been, and they’re profitable for all involved.

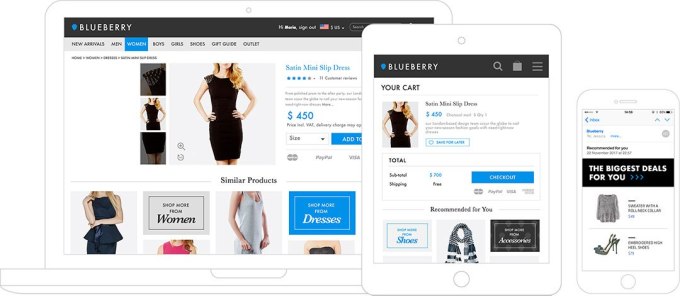

Example of Dynamic Yield’s personalization engine at work.

A Dynamic Exit

Lucas: Things obviously ended up well for Dynamic Yield, but was there ever any big tension between the company’s leadership and its investors about where it was moving?

Adam: No, I think we were generally on the same page. Again, he was working in my office for a year, so we got to know each other really well. I would not hold back on where I think he needed to make some changes or improvements, but it was never a relationship where I would just tell him what to do, I never work with entrepreneurs like that. An entrepreneur has to make the decisions, I can just be honest and be helpful, regardless of what the entrepreneur decides and be supportive.

Adam Fisher: The less traditional the buyer, the more worried you have to be that something strange will happen, that somebody will change their mind, that somebody will get fired, that something unrelated will happen on the macro level.

The company had its tough moments for sure. I mean, it was a company that had multiple shifts in its product and its customer focus, and had a few kind of strokes of bad luck in terms of financing.

But, you know, it ended up with a surprising and, obviously, happy ending, and we never thought that a company like McDonald’s would acquire the company. But we had begun to engage with very non-traditional customers looking to do various forms of personalization, offline online for very different types of products. And we realized the depth of the product and and how much little technology depth some of the biggest companies in the world have. We thought there could be something there, but you know, acquisitions of an independent software vendor… I mean, what do you do you? What do you do with the product that they’re developing for everybody else? So that took us a while to be convinced that they were serious about this kind of maintaining the company and also having it to, but it worked!

Lucas: Was it pretty much essential for this deal that Agmon was able to keep operating the company independently as opposed to folding it into some mega-corp?

Adam: Yeah, I think that was key, I don’t think [McDonald’s] would have be able to justify it from a price perspective, by the way, if it was purely buying a team to do new things. As you can imagine, as much as the team was excited about working for the McDonald’s company, the independent brand was important and keeping the relationships with existing customers and partners was super important.

Lucas: So kind of wrapping things up, McDonald’s certainly seems like a bit of an unexpected buyer considering the early history of the company, but at what point in the company’s life cycle did it make sense that they would want to buy this tech? Or are you still a little surprised that this is the deal that went through?

Adam: Oh, yeah, with these kind of things you have to be skeptical until you see it in writing, and even then, skeptical. You know, as a VC, I’ve seen too many deals never mature to an offer, or even after the offer it’s pulled away. I mean, the less traditional the buyer, the more worried you have to be that something strange will happen, that somebody will change their mind, that somebody will get fired, that something unrelated will happen on the macro level.

So, you know, we were obviously skeptical until there was an offer.

But it was very clear, at a certain point, that the level of engagement was so high and so immense that they were serious, that this wasn’t just an idea that popped up after the had met Dynamic Yield, that they had been thinking about making such an acquisition for quite a while beforehand.

Lucas: Great, well thanks for taking the time to break this down, it was nice chatting.

Adam: Thanks.

The Exit is a new, investor-focused series on TechCrunch. If you have feedback, input on a recent exit or would just like to chat, shoot me an email at lucas@techcrunch.com