2015 is soon coming to a close, and the world of hardware startups has been changing even faster.

Over the past year several trends have emerged that will shape the state of hardware for years to come.

First, the good news: more everything!

Prototyping is getting better, with the usual platforms (Arduino, Pi) but also new ones like Intel’s Edison and a few more. The price of those still puts them out of reach for low-cost consumer devices.

2016 and the sales of Next Thing’s $9 computer should help solve that. Voltera’s circuit board printer, which recently received the James Dyson Award, will in turn support faster PCB iterations for those creating their own circuit boards. Interestingly, both projects got their start on Kickstarter.

3D printing is still there, with some incremental progress, more flexibility and materials. The breakthrough from prototype to product at low-cost is yet to come.

As smartphones kept improving, including more and more technology, and selling hundreds of millions of units, they gave birth to a flurry of startups leveraging the economies of scale of mobile components.

Startups are re-imagining daily objects and inventing new devices. Those are gradually finding their way onto people’s wrists, into our homes, workshops and industries.

Supported by maker spaces incubators and accelerators, a fraction of this explosion of startups moves on to later stage financing. Investment in IOT startups is likely to hit a record height of $2B this year according to CBInsights. Some hardware startups such as Fitbit, Xiaomi or Square have reached unicorn status or liquidity, further fueling the interest of investors.

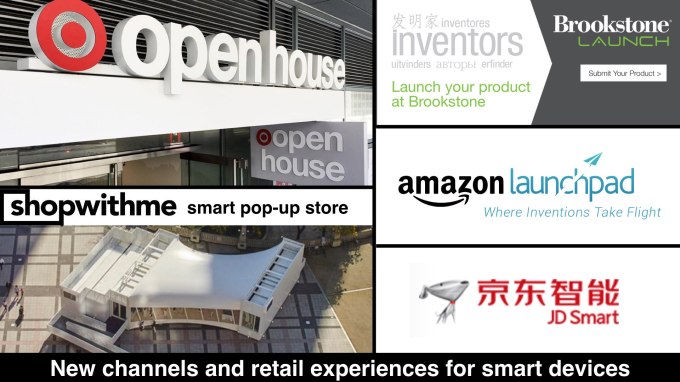

Retail is also stepping up its game with a flurry of initiatives to:

Retail is also stepping up its game with a flurry of initiatives to:

- display smart devices like at Best Buy,

- fast-track them to retail with Brookstone Launch, Amazon’s Launchpad or with JD Smart in China,

- educate customers thanks to new experiences like at the Target Open House, in San Francisco’s Metreon shopping center

- bring the store to the people with ShopWithMe‘s smart pop-up store.

Yet things are also getting harder, faster, and more competitive

Walk around Maker Faire, then in any consumer electronics trade show and you will understand why the transition from maker to startup has become more difficult. Consumer expectations are higher than ever, and scaling remains difficult, with or without engaging with foreign supply chains.

Competition looms large and many “smart devices” are becoming commoditized rapidly. Xiaomi and its dozens of satellites are at the forefront of this: cutting out middlemen and using real-time online sales they became the poster child of what we call now “Xiaomization”.

In just a few years, the prices of numerous devices have fallen by a ratio of 2 to 20. This activity tracker? A mere $10. This action camera? A fraction of GoPro’s price. Those personal mobility things? They are mainstream in China already, and can be yours for less than $300.

More, the Chinese versions are not only much cheaper but often of equal quality or better made than their “original” counterparts (when those exist). Just how much profit margin is left with all those devices as they transition to commodity status (and into more hands)? And more importantly, which ones are next?

It’s easy to get hung up on the IP issues. While they do exist in numerous cases (and are sometimes solved in unexpected ways like when Chinese personal mobility startup Ninebot bought Segway), what is equally important here is to realize that the supply chain is a weapon.

And yet, it’s not just about price, it’s also about speed. Time-to-market is another weapon in the arsenal of hardware startups. Entrepreneurs who dive into the Shenzhen supply chain can equip themselves with both. Obviously, Chinese entrepreneurs have a very real advantage there.

Chris Anderson, CEO of the drone giant 3DR said at the last MakerCon: “Before, you had 6 years [to evolve from maker to startup], today you have 6 months.”

It is a matter of time for Chinese startups to run out of low-hanging fruits and emerge with innovative technologies and services. DJI, based in Shenzhen, has thus become the leader in consumer and imagery drones. Let’s wait until new teams spin off from university research and giants like DJI, Huawei, Google and others.

Even without intense competition, the realities of a hardware business are still the same: you need money to make things. Cash flow issues might simply prevent you from building a business- unless you find suitable suppliers and distributors who will accommodate some of your cash flow needs, and help you to avoid fronting 6 months worth of inventory before you get paid.

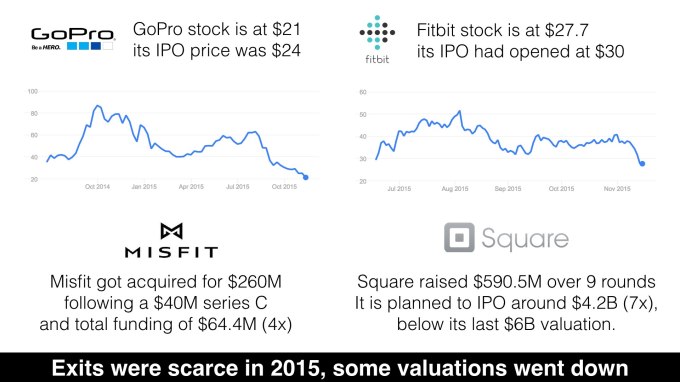

Last, exits in the hardware space have been quite limited this year, after a glorious 2014 with the GoPro IPO and the acquisitions of Nest and Oculus. Fitbit went public but its stock is now trading below its opening price. GoPro is below IPO price. Misfit has just been acquired by the traditional watchmaker Fossil for $260M, about 4x the funding it received. Square is planning to IPO at 7x its funding amount, and below its previous valuation.

What is relatively new is to see hardware startups being bought to directly join the portfolio of the acquirer: only Google (Nest, Dropcam) and Facebook (Oculus) have done it. Many others buy startups for the team or the technology (the Samsung / SmartThing and Intel / Basis deals come to mind).

When will we see Sony or Samsung acquire hardware startups for their ‘real’ potential? And when will a software company (apart from Google and Facebook) get into the hardware game?

The way forward: pick your battles, build faster, cheaper, better and plan for scale

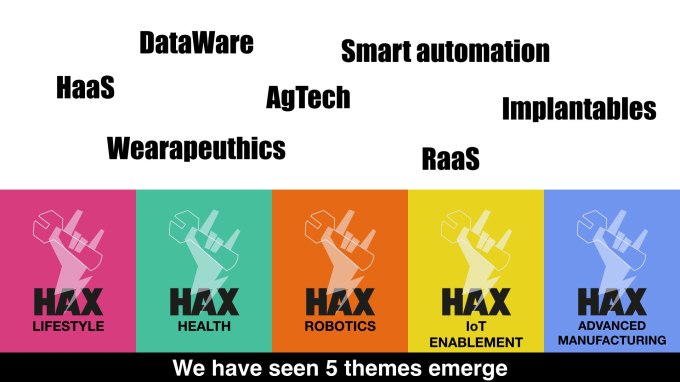

Picking your battles means going into solving harder problems, that won’t suffer “xiaomization” too quickly. Involve science (medical, material, physics, etc.), software (algorithms, AI) and communities (of users or developers) to build a moat. With this in mind, HAX recently launched five specialized tracks within its program to better support lifestyle products, robotics, health, “IOT enablement” and advanced manufacturing startups.

Beyond technological prowess, leveraging more software in connected products can help:- — turn hardware companies into SaaS businesses,

- — create health tech products who not only measure but help patients manage their condition, or cure it,

- — open new fields, sometimes literally like with Agriculture Tech.

- Further, startups are increasingly venturing to Shenzhen to do more, better, cheaper and faster. This also allows them to prepare for scaling with less pain from 1 to 100 to any number above that. Shaving months or more in time-to-market also translates to direct savings in salaries and operations costs.

Next year might bring us even more intelligent devices, at lower cost. After becoming ubiquitous and disposable, will 2016 be the year where computing becomes free?