British startup Revolut just raised $2.3 million (£1.5 million) from Balderton Capital to make you pay less exchange fees when you travel around the world. Also backed by Seedcamp, Revolut provides an app to seamlessly exchange or send money, and an optional debit card to pay around the world or online.

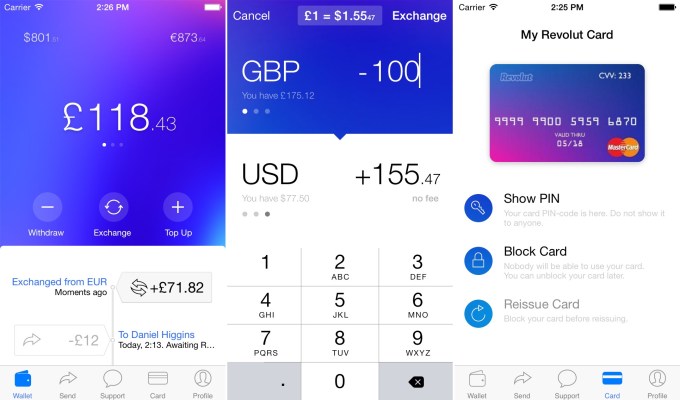

Here’s how it works. Creating a Revolut account is basically like creating a virtual bank accounts in three different currencies, USD, EUR and GBP. You can top up your account in any of these currencies using your credit or debit card, or a bank transfer. I tried topping up from my American bank account but my debit card was rejected and making a wire transfer to a U.K.-based bank account costs $35 — I blame my bank more than Revolut. Evidence of Revolut’s purpose also lies in this crazy $35 fee.

Once you have money on your Revolut account, you can exchange your pounds into euros (or any other combination) without any fee. The startup promises interbank rates, and this is exactly what I can see from the app. Exchanging money takes seconds as the startup probably holds money in all currencies at all times.

You can then send this money to another Revolut user or withdraw it from your account with a transfer. You can also ask for a Revolut debit card, which is a good old MasterCard physical card that should work around the world. This card supports 23 different currencies, meaning that even if you only hold GBP on your Revolut account, you can pay in Thai Bhat when you travel to Thailand and avoid exchange fees.

For now, everything is free — opening an account, transferring money and paying with Revolut’s card are all free. Like Number26, Revolut makes money from MasterCard’s cut on every transaction — it’s transparent for the user. Making everything free is a strategy to boost the company’s growth — the startup also says that it might add fees in 12 months.

Revolut differs from peer-to-peer money transfer services like CurrencyFair or Transferwise, as these existing services let you transfer money between two existing bank accounts. For example, I use CurrencyFair to transfer money from my American bank account to my French bank account.

But what if you don’t want to open yet another bank account because you’re just traveling every now and then? Revolut works well for this particular use case. It will be interesting to see whether Revolut is able to generate enough MasterCard transactions in order to keep its exchange rates low.