Editors Note: Rob Leclerc is the CEO, and Melissa Tilney is head of communications at AgFunder, an investment marketplace for agriculture and AgTech investing.

Before Monsanto acquired Climate Corporation in late 2013 for nearly $1 billion, few investors gave much thought to technological innovation in our agriculture system. What a difference a year can make. In what can be described as the Netscape moment for agriculture technology, the sector had a breakout year in 2014, receiving over $2.36 billion of investment across 264 deals spanning the agriculture value chain, according to data we pulled from CrunchBase as well as press releases and SEC filings for last year. Surprisingly, this $2.36 billion figure has now surpassed well-known sectors like fintech ($2.1 billion) and the former queen of green, cleantech ($2 billion).

Why now?

According to data from the CleanTech Group, investment in AgTech was relatively flat before 2013. Most tech innovation in agriculture was narrowly concentrated in biotechnology and seed genetics, and both investment and innovation was limited to players with close ties to the ag sector. Outside of seed genetics and crop inputs, most other AgTech was typically bundled with Cleantech.

Then, in 2013, there was a shift. AgTech grew 75 percent to reach $860 million across 119 deals. Taken together with our data (while recognizing our unique methodological approaches), AgTech subsequently grew 170 percent in 2014 and it’s continued to show strong investment in early 2015.

-

a groundswell of macro economic trends that tipped the balance between supply and demand in agriculture

-

shifting consumer tastes, and

-

a confluence of new hardware technologies that freed computation from the desktop and automated multivariate collection of big data.

A sea change

Advances from the mechanization in the 1920s and the Green Revolution from 1940-1960 have largely been exhausted. Rates of yield increases for major crops have been trending negatively on a 10-year curve at the very time that global forces of population growth, prosperity, and globalization are putting basic supply-and-demand pressure on our agriculture system.

The population is growing at approximately 77.6 million per year, and it is expected to reach nearly 10 billion by 2050. At the same time, the middle class is expected to double by 2030. And as incomes rise people spend more on food (Engel’s law) and eat more animal protein (8 pounds of grains are needed for 1 pound of beef). To meet the demand for food, fuel and fiber from a growing and increasingly affluent population, experts predict that we will need to double global crop production over the next 35 years.

With demand outstripping supply since the emergence of China starting in the mid 1990s, the agriculture sector has quietly outperformed all other sectors except for tech since 1999. It’s taken a while, but investors and entrepreneurs have started to take notice.

In addition to secular trends driving the agriculture sector, the public at large is now better informed about the state of our food system and more concerned about the impact that agriculture has on the environment.

Agriculture now accounts for about 30 percent of greenhouse gas emissions, a 75 percent increase since 1990, which makes agriculture a huge target for disruption. In addition, informed consumers are demanding locally grown, sustainable food with fewer chemicals, and the agriculture supply chain must evolve to deliver such products. This has created opportunities for a new generation of startups to gain a toehold into new markets that are too small for larger agriculture players.

Finally, a confluence of hardware and software technology advances are creating opportunities to address this market. Inexpensive and infinitely configurable mobile devices (enabled by advances in wireless and energy storage) have liberated technology from the office desktop. At the same time, inexpensive but sophisticated hardware sensors have emerged to automate the collection of massive data sets.

With these technology shifts, exciting technologies like drones, AI, satellite mapping, robotics, and the Internet of Things, have quickly realized that the agriculture value chain provides fertile first market opportunities for many technologies that are not advanced enough or have not yet found solutions in the consumer space. Many investors looking at these technologies are going to need to get smart on agriculture if they’re going to make informed investment decisions.

Growth potential

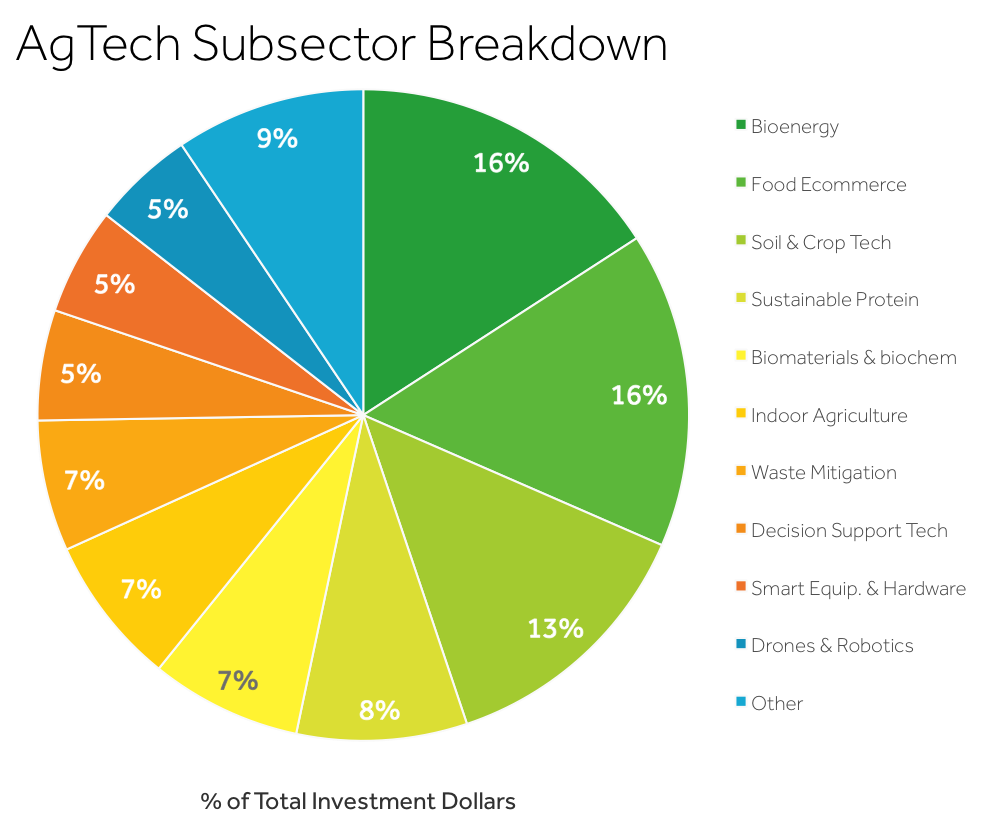

Agriculture has a long value chain and the sector is often described as being more horizontal than vertical (we tracked 16 subcategories—as diverse as biotech, food e-commerce, and smart equipment—and 10 of these subsectors had more than 5 percent share of the AgTech market), and currently there is room for growth across the value chain. Already this year, we’ve seen a $50M investment into drone maker 3D Robotics and a $95M investment into micro-satellite company Planet Labs, both of which count agriculture as key early market opportunities.

Foodtech company Soylent raised $20 million at a $100 million valuation, and plant trait company Arcadia BioSciences recently filed a $86 million IPO. And in what might seem like a jump-the-shark moment while still in the first inning, a company called FlowHive has emerged as the highest grossing campaign on Indiegogo, raising over $6.8 million for its honey-on-tap technology, already making it one of the top 10 crowdfunding campaigns of all time.

Big hairy audacious goals

Like cleantech before it, many AgTech companies are have set their sights on Big Hairy Audacious Goals. This is also a lure for investors who are attracted to companies looking to solve big problems with big market potential.

Agriculture accounts for 70% of freshwater withdrawals, and under Byzantine water rights laws that date back to the 1820s there has been little incentive for farmers to manage this resource more sustainably. In response to the massive multi-year drought, AgTech companies are developing new solutions to use water more sustainably. SWIIM, a company that was recently named a partner for the White House’s Climate Initiative, is developing the Airbnb for H20. It’s hardware/software solution enables farmers to analyze every drop of water on their property, optimize its uses, and then rent out their surplus water needs to thirsty municipalities and industrials.

On the other end of the spectrum, Hampton Creek, a vegan mayonnaise company, is attempting to formulate an egg-less egg product. If Hampton Creek can create a palatable all-vegan egg, the product could have a disruptive effect on the $120 billion egg industry.Investors seem to think so, too—the company took in $90M from the likes Silicon Valley heavyweights Khosla Ventures, Founders Fund, Li-Kai Shing’s Horizons Ventures, Jerry Yang (Yahoo), Marc Benioff (Salesforce), and Eduardo Saverin (Facebook).

And even further out there, New York-based Modern Meadow is printing meat and leather products with 3D technology. Although 3D-printed meat may take a while to hit the market and win trust from consumers, Modern Meadow has an opportunity to take on the $54 billion leather market by cultivating cow-less leather from real cells. And unlike leather made from an animal, the process doesn’t require any harsh chemical treatments.

Returns still need to be proved

This new generation of AgTech has only seen a few major liquidity events, and this will be a test for the industry in the years to come as investors assess their portfolios. In general, strategic acquisitions have largely been the path for liquidity for AgTech companies, but most of the incumbents have shown little appetite. While companies like John Deere and Syngenta have been mostly silent, Monsanto has decided not to wait for the competition. In 2011 Monsanto acquired Beelogics and Divergence; then in 2012 they acquired Precision Planting for $210M; and in 2013, Monsanto established Monsanto Ventures in San Francisco, and went on to acquire Agradis, GrassRoots, Rosetta Green ($35M), and Climate Corp. ($930M). As mentioned earlier, Climate Corp. has since been given access to Monsanto’s checkbook and has been on an acquisition spree itself with other Silicon Valley startups like Farmers Edge following suit.

In several subsectors, notably food e-commerce and bioenergy, companies are reaching sizes where an IPO is within grasp, but for most of these subsectors, it’s still too early to see the emergence of large AgTech companies. This will undoubtedly change over the next five years. The agriculture industry has historically sprouted large public corporations, and AgTech, still in its infancy, should be no different.