Last week, when Square started pre-orders for new chip-based card-reading hardware to upgrade its older mag-stripe readers, we noted that it seemed only a matter of time before the company would finally turn on more international services, where the newer chip-based system reigns supreme. Now it looks like that’s just what Square has quietly started to do.

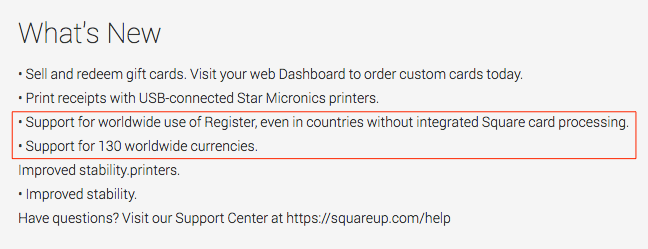

Updated Square Register apps in the iOS and Google Play’s Android app stores — part of the company’s bigger solution that lets merchants turn their iOS or Android smartphones and tablets into payment processing devices — note that the point-of-sale app supports 130 currencies and “support for worldwide use of Register, even in countries without integrated Square processing.”

But it’s still babysteps for the company. While the Square Register app has now been turned on internationally, the hardware, and payment processing, have yet to arrive.

“If you are in the U.S., you can also take payments with a Square Reader or Square Stand,” the company notes in the app description.

Sources tell us that Square has been in talks with merchant acquirers and others in the payment processing chain for at least six months now in Europe. What the company could be doing, therefore, is testing the waters to see where Register is picking up usage and how it’s being used, as well as start to build up a base of merchants who it can then eventually convert over to payment services.

Square Register is Square’s virtual component to its payment business. It lets users keep track of sales and inventory, manage items, and view analytics about a business, as well as manage an online storefront Square offers you free when you become a customer.

Before now, Square, founded in 2009, only had services live in the U.S., Canada (October 2012) and Japan (May 2013). And as such, Square Register apps did not appear in app stores outside of the the U.S., Canada and Japan.

I have been able to register for Register (!) under a UK address, with a pop-up menu listing the 129 other territories and languages now online. It reconfirms also what the app says: so far no card processing possibilities. “Square does not currently offer card processing in your country, but we will let you know if it becomes available.”

All change on the payments train

As we noted last week, Square’s payment hardware and payment services are in a state of flux right now. It has now started pre-orders for new chip-based devices, which will be shipping early next year.

For now, it looks like these devices — which operate on the EMV standard (jointly developed by Europay, Visa and Mastercard) and scan a chip embedded in the card for the duration of the transaction process — will require a signature, not a PIN number. (EMV was built to allow for one of the two options.)

This could become problematic: At one point iZettle, the mobile-based payment services based out of Sweden that competes with Square, found itself unable to process Visa cards in certain markets because chip-and-signature is considered more liable for fraud than the chip-and-PIN combination.

That leads me (and other observers) to suspect that Square may, in fact, include PIN-based functionality too sooner rather than later. This could come in the form of a PIN “pad” (screen) on a handset, or in an updated or separate piece of hardware.

Crowded, but not busy, markets for payments

Square will be coming into the mobile payments game in markets like Europe after several would-be competitors have launched.

Other companies that offer mobile-based, dongle-based point-of-sale services in Europe include PayPal’s Here, Rocket Internet’s Payleven, Orderbird (backed by Mastercard and PayPal), SumUp (backed by Groupon), and others.

iZettle, which this week expanded its European footprint to The Netherlands, has also made some inroads into Latin America in partnership with investor Santander. Jacob de Geer, iZettle’s CEO, tells me that the shifts in the U.S. market that are seeing a move to the EMV system are creating an opportunity for it to look at entering North America as well.

By and large, however, in regions like Asia (excluding China) or Latin America, where smartphone adoption is growing fast compared to more saturated and mature markets, the number of companies offering such services are still few and far between.

Yet Square’s expansion also comes at a time when there is still a lot of room for growth in general, with no single mobile payment service as-yet managing to ignite and comprehensively swing a critical mass of merchants to take up the services.

(The latter state of affairs is what Apple, a very recent mover into payments with Apple Pay, also hopes to tap into. Square apparently will support Apple Pay accounts in the future.)

Square the service, Square the startup

It’s not a surprise to see Square finally making a move to grow outside the U.S. for another reason.

The company has raised just under $600 million, but with its business model based around getting a very small cut on each transaction, it needs to gain more critical mass to improve its returns. It’s not clear what it’s current growth rate is in the U.S. but it’s notable that earlier this year the company apparently postponed plans for an IPO.

Why? Problems with its revenue run rate, according to reports, which hasn’t justified Square’s valuation. That valuation was $5 billion at the time of that story getting reported in February 2014. A source close estimates it is now closer to $6 billion.

This puts the company under more pressure for an exit: either to go public or get sold (reports of the latter have been denied by the company; accurate or not, we keep hearing names).

In either case, a larger international component to its business (beyond Canada and Japan) will be essential.

The margins on the product are relatively thin. Square only lists fees for transactions in the U.S. and Canada on the app in Google Play. The company takes a flat commission of 2.75% per swipe for Visa, MasterCard, Discover, and American Express cards. This is likely to be repeated in other markets, as it is similar to the commissions that other services have been taking. Square says payments are deposited into a merchant’s bank account in 1-2 business days.

Part of that has been around how Square spread its products and marketed itself. Square first picked up stream on its U.S. home turf by shipping dongles free of charge to small businesses. The carrot was a service that was portable and easy to implement, aimed at merchants who were either already paying high fees for more traditional payment card point-of-sale solutions, or simply only taking cash.

With the new devices, Square will be introducing fees for the hardware, and potential way of improving its margins on the service. Pre-orders for the readers start at $29 for the dongles that plug into handsets or iPads, and $39 for a less portable table-top version that looks a bit more like a traditional card reader.

We have reached out to Square to get more details and will update as we learn more.

Update: “We don’t have anything to share at this time,” a Square spokesperson says.

Update 2: Corrected to note that Square has so far only opened pre-orders for EMV devices that work with chip-and-signature, not chip-and-PIN, authentication. (H/T IDC payments analyst James Wester)