Editor’s note: Cyril Ebersweiler is the founder and Benjamin Joffe is general partner of the hardware startup accelerator HAXLR8R (“HAX”). Both have been living in China and Asia for over a decade. This is the sixth part of their series on “Lean Hardware.” Applications for the next HAX program starting in January are open until November 20, 2014.

About a year ago, Aileen Lee from Cowboy Ventures wrote her seminal piece on billion-dollar startups, now widely called “unicorns.” At the time, she found 39 U.S.-based software companies fewer than 10 years old in that category.

Since then, other articles expanded this list to a global research by various people like Fred Wilson from Union Square Ventures, which lead to further analysis. South Korea alone had 10 of them, though a few were older than 10 years. The news about an actual unicorn lair found in North Korea proved to be a misunderstanding.

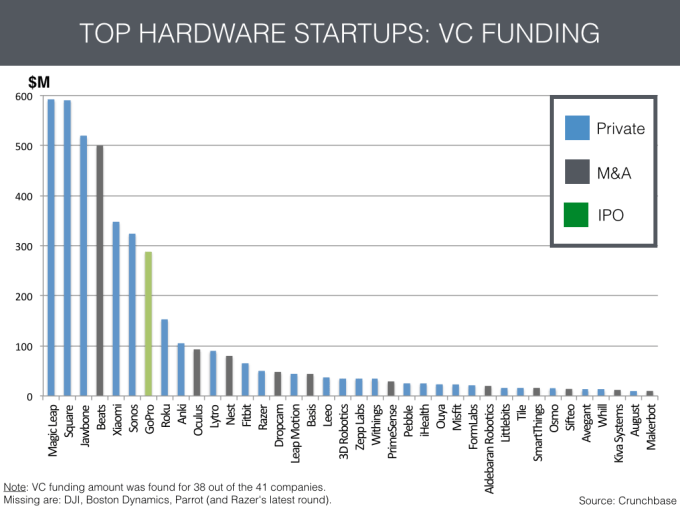

As early-stage investors and hopeful hardware unicorn breeders, we looked into the situation of hardware unicorns and up-and-coming “ponies.” As it takes an average 7 to 10 years to unicorns to reach $1B, many of the newer companies will need more time to reach a high valuation, so our list includes 41 hardware companies that raised the most VC funding or exited recently. The source is accessible here and you are welcome to expand it.

Below is a list of things we have learned about the “hardware unicorn club”:

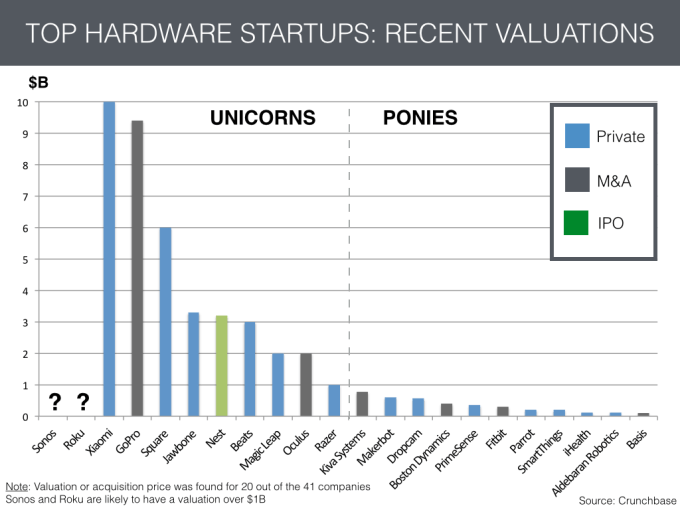

- We found 11 companies with a valuation above $1 billion. Their combined valuation was above $40 billion.

- Only one unicorn did IPO (GoPro) and three others were acquired (Nest, Beats and Oculus). Exits are more likely to be acquisitions than M&A: Another eight companies were acquired in deals ranging from $100 million to $1 billion.

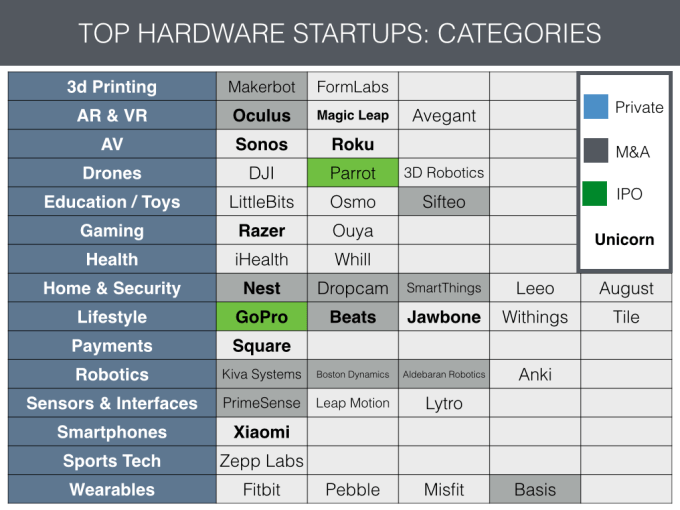

- Most companies are B2C. Robotics dominate B2B.

- Despite the media attention, wearables and smartwatches are a relatively small percentage among unicorns and ponies. AR/VR, Robotics, Smart Home and lifestyle products also fared well.

- Most companies were from the U.S., while China and Europe had a few outliers. We did not research age and ethnicity of founders and it is possible some foreign companies “rebranded” as US companies. It is likely China, Japan and Korea are punching below their weight, as their expertise in consumer electronics is undeniable.

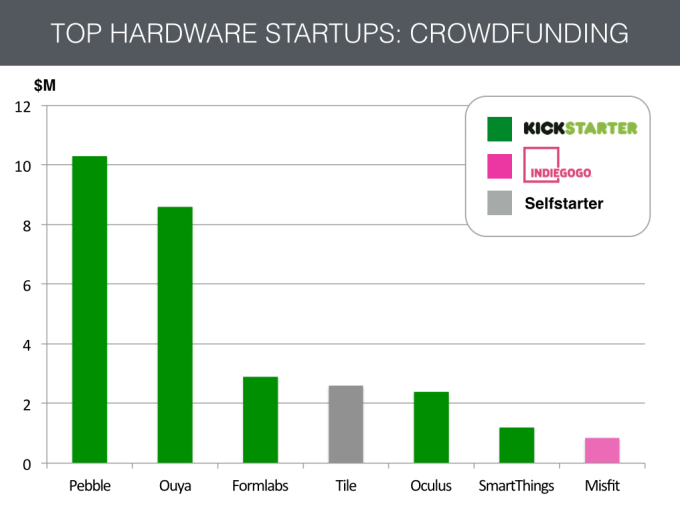

- Crowdfunding is still nascent but seven startups on this list, including one unicorn, raised funding on Kickstarter, Indiegogo or on their own. It is likely this trend will grow.

- There is (almost) no hardware without software. Standalone hardware was an exception.

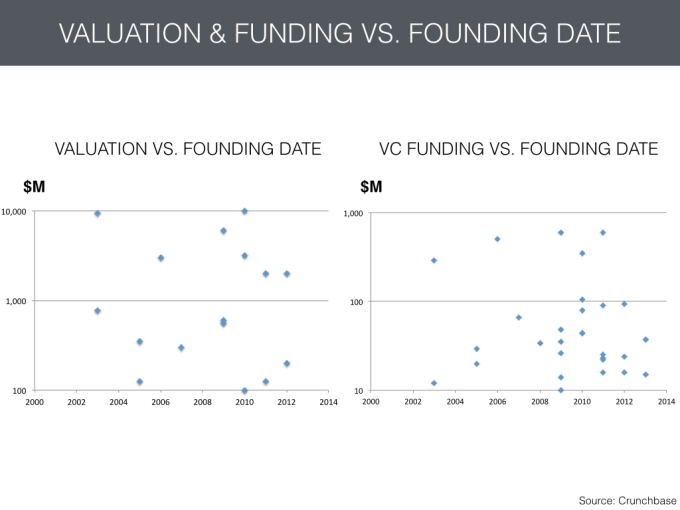

- Hardware unicorns are growing faster. Five out of the 11 unicorns and a total of 27 startups out of the 41 in our list were less than fewer years old.

- Unicorns ship products.

Welcome to the Hardware Unicorn Club

We could not estimate precisely the percentage of unicorns among hardware startups due to lack of data. Yet, it is likely they represent less than 1/10th of tech startups — maybe even 1/20th or less. Aileen Lee estimated the number of software and Internet companies at 60,000 over the past decade, so a generous estimate would be 6,000 companies for hardware. Eleven out of 6,000 would be 0.18 percent or one out of 545.

The number of hardware unicorns is probably still too low to be statistically significant, but a sloppy analyst could say your chances of reaching unicorn status are more than twice as high as in software (for which chances are 0.07 percent, according to Lee).

Prototyping has become much easier, whether it is for giving a new connected life to existing “dumb” product categories or building entirely new ones. Electronics can be done initially with platforms like Raspberry Pi, Arduino and Spark Core. Connectivity is done via smartphones, Bluetooth, Wi-Fi and cloud infrastructure. Even prototyping circuit boards is becoming easier with a growing number of PCB printers, reducing the time needed for iterations. And coming up with form factors is now a fairly simple job with 3D printing.

Finally, going to market and manufacturing is also getting easier thanks to the “Lean Hardware” approach and the opening up of Shenzhen’s supply chain to startups.

All those reasons might explain why the investment in IoT is soaring.

Acquisitions Dominate in Hardware

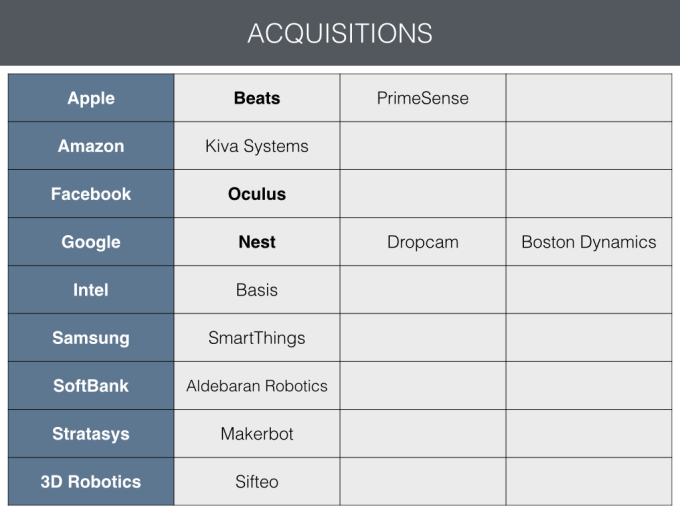

So far only one unicorn went IPO (GoPro) but combined acquisitions are worth over $11 billion. The largest acquisitions were done by software companies: Google (Nest, Dropcam, Boston Dynamics), Facebook (Oculus) and Amazon (Kiva Systems). For software firms, acquiring hardware startups can be seen as an easier option than building a hardware business from scratch.

Apple (Beats, PrimeSense), the world’s largest hardware company, also acquired a few hardware startups for brand or technology. Other giants like Microsoft, Adobe, Autodesk and more are also joining the hardware game.

“Part of the reason we don’t see hardware startups make it to IPO is because they’re often product-centric; this means they’re not iterating and launching new products fast enough to beat emerging competitors,” says Madelynn Martiniere, community engineer and founder of Spark Plug Labs. “To see a successful IPO, hardware companies need to create an ecosystem of rapid innovation, instead of a single product.”

B2C > B2B, But Products Aren’t Always for the Mass Market

B2B hardware used to rule the tech space with components, servers and infrastructure, from Internet to telecom. Today’s consumer hardware companies generally require much less investment, less capital expenditure and are more nimble.

With easier prototyping and rising interest in early stage investment their number is likely to grow fast. At HAX alone, we already launched 50 hardware startups and will add another 30 in 2015, the majority B2C.

Yet, B2C does not mean mass market, according to Madelynn Martiniere:

“Oftentimes startups focus on creating mass market hardware products, and that’s not the best way to go. It’s nearly impossible to create ubiquitous devices that resonate across all consumer segments. The most successful emerging hardware companies will develop solutions that will fundamentally disrupt specific sectors, and encourage new ways to interact with existing devices.”

Wearables Aren’t the Biggest Players

It is increasingly hard to differentiate in the crowded smart watch and activity tracking space. How can you do anything 10 times better or much differently in that category? Just tracking steps 10 times more accurately is not going to cut it.

It is thus no surprise that HAX did not invest much in wearables, preferring robotics and other lifestyle products. 6 out of 10 startups in our last batch were robotics (including one biotech robot and one robot for cats).

Most Hardware Startups Are from the U.S.

Not necessarily from Silicon Valley, mind you. The U.S. benefits from the world’s largest consumer market, a strong early adopters population, a fair number of role models and an ecosystem supportive of entrepreneurship.

Only Xiaomi (CHI) and Razer (SIN) were from overseas among unicorns. Despite their strong skills for consumer electronics and product design, Japanese, Korean and Taiwanese engineers are still locked into large MNCs like Sony, Panasonic, Samsung or LG.

In China, despite an obvious competitive advantage thanks to the world’s best supply chain for electronics, software is seen as more attractive and has led to a flurry of IPOs in everything from gaming, e-commerce, travel, jobs and search. Maybe Xiaomi’s success will inspire some?

As hackerspaces, fablabs and hardware accelerators are opening around the world, we might see an emergence of hardware startups from outside the U.S. in the coming years.

Thanks to our accelerator program, HAX sees thousands of applications with ideas coming from literally everywhere. Out of the 50 startups that graduated so far, 60 percent were from the U.S. and Canada, 20 percent from Europe and 20 percent from Asia. Let’s see how the needle moves next year.

Crowdfunding Is Here to Stay

Crowdfunding is a great place to launch products but not many can become large companies.

“Backers are buying a product,” says Matt Witheiler, general partner at FlyBridge Capital. “Investors are buying a vision. Some products may generate tons of demand (like the Coolest Cooler) but may not be great venture investments.”

That said, crowdfunding already gave birth to one unicorn (Oculus) and is an increasingly popular go-to-market strategy for hardware startups. As platforms mature and backers get more educated about what makes a project worthy, it is likely this trend will reinforce.

Dropkicker is one such site educating the market about the feasibility of projects.

“A lot of the “scams” that we’ve found on crowdfunding sites are really the result of inexperienced people hopelessly overestimating their abilities,” said Michael Ciuffo, one of its founders, in a recent interview.

We hope to see more whistleblowers looking at projects as the platforms grow.

HAX startups completed 23 crowdfunding campaigns so far, bringing early sales and market feedback from early adopters. With this approach, several of our startups managed to go to market with a mere $25,000 in capital, a far cry from the hundreds of thousands or millions that used to be commonplace for consumer electronics. Post-crowdfunding, a majority went on to raise venture capital in a much more comfortable position.

Here is more on what we learned about crowdfunding.

There is Almost No Hardware Without Software

HAX often gets asked about China and IP. Our answer is “If you’re successful and it’s easy to copy, it will be. So don’t do easy things.” Beyond patents, IP comes in the form of complex technology, software, algorithms and a community of developers or users.

While some consumer product companies like Beats and Jawbone emphasize design and branding, software is often the most important asset.

A difficult technology like those put forward by PrimeSense, Kiva Systems or Boston Dynamics are a classic and highly relevant way to stay on top. In some cases, like Square, the hardware itself is trivial compared to the software and ecosystem and might even disappear in the future.

Building a community around a product is a strong asset: Makerbot with its Thingiverse, Oculus, Glass, Spark or Leap Motion with its developer community, or even Xiaomi’s fans who also contribute lots of feedback.

Last, data can help create better services, derive high value information and use other business models than a pure hardware sale. Nest, Dropcam and Fitbit fit that category.

Hardware Unicorns Are Growing Faster

Xiaomi, Nest and Oculus reached unicorn status in fewer than four years. Xiaomi and Nest were founded by industry veterans with capital access, but Oculus was bootstrapped and soared.

This is the key reason HAX started in 2012 focusing exclusively on hardware: not only can one go to market much faster and cheaper than before, but also reach scale at a greater pace. Figuring out how much faster it can be done is one of the items on our to-do list.

Unicorns Ship Products

All unicorns shipped tens or hundreds of millions of dollars worth of products. Except Magic Leap. But it’s magic, like unicorns.

In Conclusion

The jury is still out as to whether unicorns are born or bred. One apparent thing is that you don’t become a unicorn without shipping products.

We believe, however, that caring for hardware companies during their early stages increases dramatically their chances of avoiding an early death due to either poor product/market fit, mishaps in prototyping or manufacturing, and inadequate marketing, distribution or financing. For more on this, our list of “Wares” to avoid has become popular. Now, we’ll have to wait and see whether those startups are to become ponies or unicorns.

Thanks to Duncan Turner at HAXLR8R, Matt Witheiler, Madelynn Martiniere and Christine Magee for their help with this article.