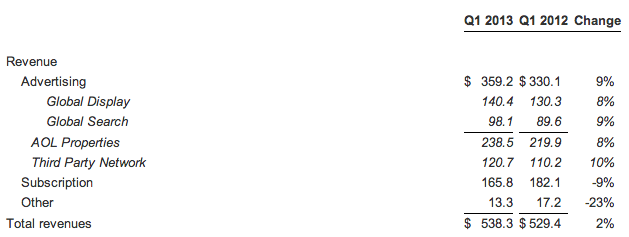

AOL (owner of TechCrunch) has just reported its Q1 results for the quarter, and it’s a mixed bag, with sales of $539 million, up 2%, beating Wall Street estimates, with diluted earnings per share coming in at $0.32. Analysts were expecting revenues of $537.15 million, with First Call’s EPS estimate of EPS at $0.32. Still, Q1’s EPS number is up 45% on the same period a year ago. Net income was up 23% to $25.9 million.

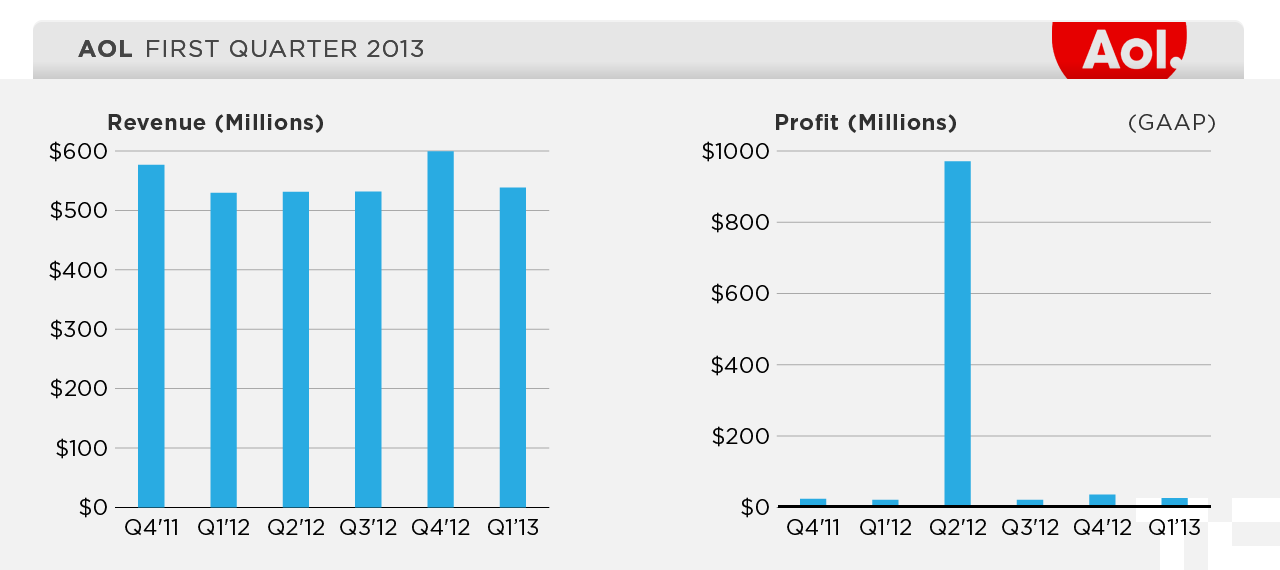

Here’s how revenues and profit break down over the last several quarters:

This quarter, it looks like AOL’s global display revenues are finally in an upswing, rising 8% over a year ago to $140 million. Subscription revenues, the legacy part of AOL’s business that still includes (yes) revenues from dial-up customers, is still coming in as a bigger part of AOL’s revenues, at $165.8 million. They are slowly on the decline, though, down 9% on a year ago.

Last quarter was a notable one for AOL in that it was the first one in eight years where the company had posted revenue growth, with revenues of $600 million for the three-month period. As with many other online, advertising-based companies, AOL’s revenues for this most recent, post-holiday quarter will be seasonally lower.

More interestingly, the company has been working to reposition itself around a couple of key strengths where it can still gain ground, even as Google continues to dominate the online advertising market overall. As eMarketer notes, in AOL’s biggest market, the U.S., its share of online ad spend is in decline, with AOL’s share expected to be 2.3% this year compared to 2.5% in 2012, with Facebook and Google particularly gaining in the display sector where AOL makes most of its revenue. Total display ad spend in the U.S. is projected to be $17.7 billion this year, with AOL taking 3.1% of that, with Google and Facebook taking 17.6% and 15.5% respectively. In this regard, for AOL to make its position as strong as possible in the couple of areas where it can still grow.

The first of these involves innovations around ad tech. That has included grouping together all of the company’s online advertising sales and technology assets into a single group, AOL Networks. And last week the strategy got another boost when AOL signed a deal with FreeWheel and Mediaocean so that AOL’s online inventory, and specifically its video inventory, can be bundled together with TV ad buys in a multiscreen strategy.

The second is a stronger emphasis on rich-media advertising, specifically against premium content that AOL owns itself or has deals to provide advertising for. AOL’s portfolio got a boost early in the quarter with the acquisition of gdgt, started by two former Engadgeteers (founder Peter Rojas and ex-editor-in-chief Ryan Block).

And last week, AOL expanded the amount of content against which it can sell online ads even further with the news that it would be releasing 15 new original video programs, created in a factual, unscripted format that fits with the rest of AOL’s newsy portfolio. However, as it grows in these areas, it’s also continuing to whittle down assets in others, such as its nearly-concurrent decision to shut down AOL Music.

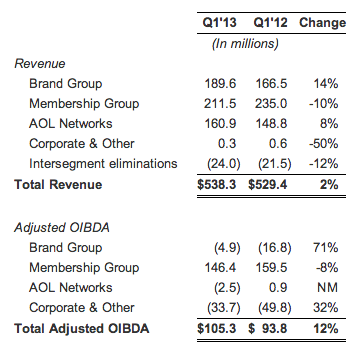

AOL’s own branded content is still lagging behind the company’s subscription revenues (again, these relate mainly to the company’s legacy services) but they are also showing the strongest growth in terms of revenues over a year ago. But if you look at operating income before depreciation and amortization, collectively the Brand Group, along with AOL Networks, are still loss-making, if coming very close to break-even:

The third-party advertising business continues to grow for AOL. This quarter revenues for ads distributed on sites not owned by AOL were up 10% to $120.7 million.