Larky, an Ann Arbor, Michigan-based startup focused on helping users take better advantage of discounts and benefits from various clubs or members-only organizations like AAA, AARP, as well as health insurance providers, credit card companies, and more, is today announcing a seed round of $650,000. The round, which officially closed in late 2012, was led by North Coast Technology Investors, and included participation from First Step Fund and the Michigan Pre-Seed Capital Fund, which gives the state of Michigan an equity stake in the new company.

The company was co-founded by Andrew Bank and Gregg Hammerman, who had previously co-founded Techstreet back in 1994, which they later sold to Thomson Reuters. Bank stayed on with Reuters for some time, growing the business there. The two teamed up again last year to create Larky, a service inspired by personal need.

Hammerman came up with the idea on a family trip to Florida, when he thought to ask at a museum he was visiting whether or not there was any discount available, since he was also a member of a museum back in Ann Arbor. As it turns out, there was – in fact, access to the museum was free.

Hammerman came up with the idea on a family trip to Florida, when he thought to ask at a museum he was visiting whether or not there was any discount available, since he was also a member of a museum back in Ann Arbor. As it turns out, there was – in fact, access to the museum was free.

The idea then struck him that many people don’t even realize they may have discounts or deals available to them, or even when they do, they don’t remember to ask or know how to go about using them.

“One hundred and twenty million Americans are members of three or more membership associations,” explains Bank. “Sometimes it’s alumni associations and professional associations, sometimes museums and cultural institutions, and even credit cards and health insurance. We’re all entitled to hundreds of discounts we don’t even know exist,” he says.

Across the U.S., there are 200,000 memberships organizations, Bank remarks. In Larky, which is available both online and as a mobile application, they’ve documented the deals and discounts for around 2,000 of those groups. However, those 2,000 account for what 90 to 95 percent of people are looking for today, Bank claims. This includes big name groups like AAA, AARP, USAA, VISA, AMA, Blue Cross-Blue Shield, Costco, American Express, AFL-CIO, and several other alumni associations and museums.

To be clear, Larky doesn’t yet have a partnership with all these groups, but is in discussions with several of the above, and has a deal with a well-known health insurer in the works. To date, it has partnered with around ten associations, including alumni and transit organizations, which have a combined reach of around 600,000 to 700,000 total members.

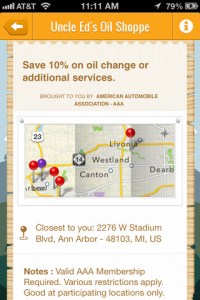

To use Larky as a consumer, you don’t have to provide the startup with your actual account numbers, only the basics of which groups you’re a member of. On mobile, the app is the most helpful, since it can alert you while at point-of-sale that you have a deal available, as well as how to use it. For instance, if the merchant offers an AAA discount, you’ll get an alert, and you can also store a photo of your AAA card in the app so you don’t have to fumble around with your wallet.

To use Larky as a consumer, you don’t have to provide the startup with your actual account numbers, only the basics of which groups you’re a member of. On mobile, the app is the most helpful, since it can alert you while at point-of-sale that you have a deal available, as well as how to use it. For instance, if the merchant offers an AAA discount, you’ll get an alert, and you can also store a photo of your AAA card in the app so you don’t have to fumble around with your wallet.

Longer term, Bank says he foresees Larky being integrated directly with payment systems, both online and on mobile – such as in Google Wallet or PayPal, for example. If that came to pass, your discount could be provided to you at the same time as your payment was processed. “When mobile and online payment systems get more mature, they’ll all have APIs,” Bank explains. “And we don’t even really care who wins – we can integrate with all of them,” he says.

For consumers, it’s easy to see the value proposition here. But there’s also value to the organizations, too, which use their membership rewards as a way to encourage renewals. They, too, are generally frustrated by the current system, where users aren’t well aware of when, where, and how they can redeem their benefits and rewards.

Larky plans to sell its analytics data back to these groups, allowing them to see their perks’ performance and member behavior data, including things like how much members are saving. Though it’s not tying that data to individual accounts, Larky’s service asks users if the discount worked and how much they saved, somewhat like RetailMeNot does with its coupon codes.

The company is also beginning to respond to organizations’ requests to help them improve their discounts by connecting them with more merchants.

Going forward, the immediate plan with the funding is to continue to iterate on the iOS application before launching on Android, close on more partnerships with organizations and groups, and launch a browser add-on which enhances search results by indicating where users have an available discount on products they’re searching.

In the meantime, interested users can sign up for Larky here on the web, or download the Larky app to their iPhone.