Over the years we’ve seen the emergence of a number of personal finance apps, most of which have been designed to help users create budgets, better understand their finances, and make positive decisions with their money.

Those apps were great for the small percentage of users who were already ultra-interested in examining the minutiae of where their money was going… But for those of us who don’t want to deal with the cognitive overhead and depression that comes with knowing you’re spending more than you should on things you don’t need, they weren’t very helpful.

That’s why over the past few months I’ve become such a big fan of a little startup called Digit. See, Digit wants to change the way users think about saving cash, by helping them to put money away without having to think about it at all.

To do that, the company has raised $2.5 million in seed funding and is working on an integration with a banking partner that will make its savings happen even more seamlessly.

How Digit Works

The concept behind Digit is pretty simple: You create an account, give Digit access to your online banking account credentials, and over time the company gradually transfers funds from your checking account and into a non-interest bearing but FDIC-insured Digit savings account.

The service does so seamlessly, without asking you how much you want it to transfer beforehand. Instead, Digit relies on an algorithm that determines how much it should move from one account to another, taking into account a number of factors it knows about your payment history and spending habits to do so.

Digit looks at the amount of money that you have in your account, first and foremost, to determine if it’s safe to move money out of it. Then, among other things, it takes into account a user’s regular salary or payment schedule and how far away they are from their next payday. It also looks at someone’s daily spending habits to determine how much it can transfer without them really noticing or feeling any financial pain.

Digit founder Ethan Bloch

In and of itself, that runs counter to the way most financial apps operate, in that it doesn’t overburden the user with too much information or rely on them to change their behavior to benefit their financial interests.

The other interesting quirk about Digit is that it doesn’t have a mobile app or web site with detailed statistics about your spending habits, where your money went, or how you could better budget for the future.

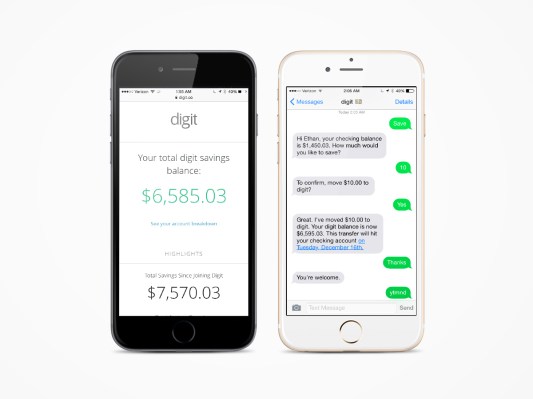

In fact, its website is pretty bare bones, only showing a few details about a user’s Digit account: How much money is currently in the account, how much has been saved over time, what the average transfer amount is, and how often a withdrawal happens. If you care, the site also has a detailed list of each transfer over time that you can scroll through.

Rather than overwhelm users with information on the website, Digit’s primary mode of communication with users is via SMS. It sends users daily updates via text with different pieces of information each day. Most days it provides users with the balance of their checking account, but occasionally also updates them on how much they’ve saved with Digit over the course of a week or a month.

Users can then request more information using a series of simple SMS commands. For example, type ‘Recent’ and Digit will text back the last three transactions to be recorded by your checking account. Type ‘Withdraw’ and you can move money back from your Digit account to checking at any time.

And Now For The Haters

There are a few caveats to the Digit service that potential users should know about. Most importantly, users should know that the money that is transferred into your Digit “savings account” isn’t really bearing any interest, the way a normal savings account would.

That will no doubt cause some skeptics to complain that any Digit user would be better off just putting aside the money themselves into their own savings account. Or better yet, those users should be putting their money into stocks or bonds or basically anything with a better financial return than a sub-1% APY savings account.

But those people are missing the point: Digit exists because the majority of people in the world aren’t good at saving money and wouldn’t do so on their own.

It puts money aside so that they don’t have to, and does so in a way that requires very little foresight. It’s hoping for a maximum amount of gain for the least amount of pain.

That is, if Digit is saving on your behalf and you don’t really notice any money has gone missing from your checking account, well then, the team at Digit believes it’s doing its job well.

And, frankly, I have to agree. I have been part of Digit’s pilot program since August, and over that time the service has saved about $1,000 on my behalf. (It’s not a ton of money, but it’s $1,000 more than I would probably have if I had tried to save on my own.)

Since launching its pilot in earnest over the summer, Digit has saved more than $600,000 for the users who have signed up, according to CEO Ethan Bloch. That comes out to about 5.5 percent of users’ monthly income on average, he told me.

About That Funding

Bloch is the former CEO of social marketing startup Flowtown. That company was acquired by Demandforce in 2011, and not long after that Demandforce was acquired by Intuit. After kicking around the Intuit product team for a bit, Bloch decided to head back into startup land, and soon after started working on Digit.

To get the service off the ground he’s raised $2.5 million in seed funding led by Baseline Ventures — which, coincidentally, also led the investment in Flowtown. Also participating in the round are Freestyle Capital, Upside Partnership, Google Ventures, Operative Capital, Garry Tan, Alexis Ohanian, Aaron Harris, Rick Berry, Nate Bosshard, Eric Ries, Joshua Greenough, Randy Reddig, Eoghan McCabe and Ted Rheingold.

That money will be used to grow the team slightly, as the company works to integrate with a major banking partner. Doing so will lower the cost of processing its ACH transfers to more favorable rates, while also ensuring that it will be able to scale up over time.

In addition to the funding, Digit is also announcing a number of advisors to the company, including Braintree founding CTO Dan Manges, early Square team member Randy Reddig, Airbnb global payments general counsel Sharda Caro-del-Castillo, and Paul Hastings partner Tom Brown. With their help, Digit hopes to make savings more seamless for a whole bunch of users.