Editor’s note: Ilgiz Akhmetshin is a business development and marketing at SKTA Innopartners. Ilgiz has a diverse experience in IT and Information Systems.

Over the past few years the semiconductor funding ecosystem experienced a downturn. According to the GSA survey, there were only five Series A semiconductor funding rounds and 10 exits in 2010 in North America, Europe and Israel. Most of the VCs who invested in semiconductors shifted their focus to software startups due to higher scalability, faster time-to-exit and low cost of failure.

However, I believe semiconductor funding hit bottom in 2013, and it is slowly coming back. I analyzed publicly available transaction data from CrunchBase and discovered promising insights about recent funding trends.

Exodus of VCs

Expensive capital expenditures

There are multiple reasons why semiconductor startups are no longer attractive to VCs. The first reason is the amount of capital that startups need to advance from the concept to proof-of-concept stage. Usually, it takes up to 18 months and up to $1 million to design and test the concept and an additional $2 million to receive the first sample chip.

The amount of capital required to start a semiconductor startup increases the potential impact of the technology risk that VCs cannot mitigate, since there is no opportunity to fail fast. Given this funding structure, venture capitalists shied away from semiconductor startups.

Consolidated industry

The second reason semiconductors are no longer attracting VCs is the mass consolidation in the semiconductor industry. With few remaining industry giants there are few potential acquirers (i.e. exit opportunities) and few potential large customers that could enable the startup to scale.

For example, one of the biggest pain points in the industry is the lack of a cheap and reliable EUV light source for sub-10nm nodes. There have been several startups with viable solutions; each seeking around $2-3 million to bring their product to the market. However, only one customer, who could provide opportunities to scale the business, exists – ASML, which has already invested in Cymer. This situation makes it very tricky for the startups to raise funding.

Another example would be the cost of design tools. There are only two: Cadence and Synopsys. Each license for a small startup team ranges from $50K to $75K per seat per year. This significantly increases the burn rate of the startups.

Long sales cycle

Long sales cycles is a third issue making semiconductor startups less attractive to investors. Let’s say a startup has successfully addressed all the problems and creates the best chip. On average, it will take approximately three years to get the chip from design-win to general availability in the market. Calxeda had a viable and attractive product but failed to ramp sufficient sales in time to remain viable. Lack of opportunity to get the market traction fast significantly hinders the startups’ ability to raise initial funding.

Semiconductor Startup Funding Is Coming Back

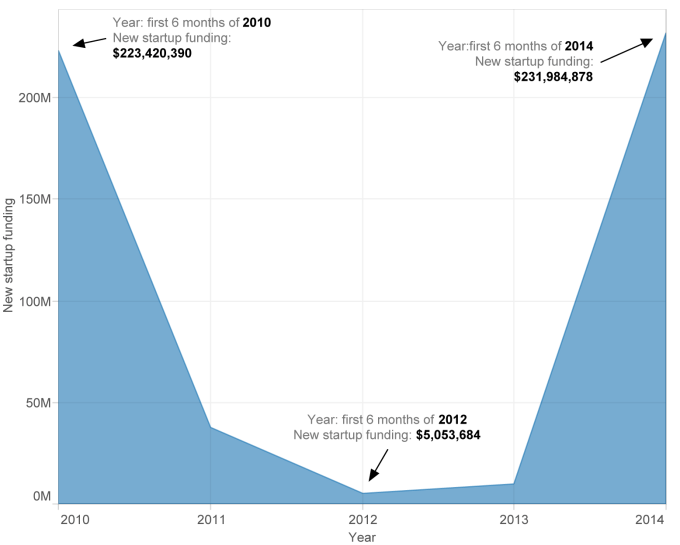

Regardless of all the problems mentioned above, it seems the semiconductor funding ecosystem is slowly recovering. Looking at the first six months of 2014 data, one can see that the number of funding rounds increased from 30 to 35 and the number of funded startups increased from 27 to 31.

Even though the increase may seem negligible and statistically insignificant, the real change is hidden in the types of these deals.

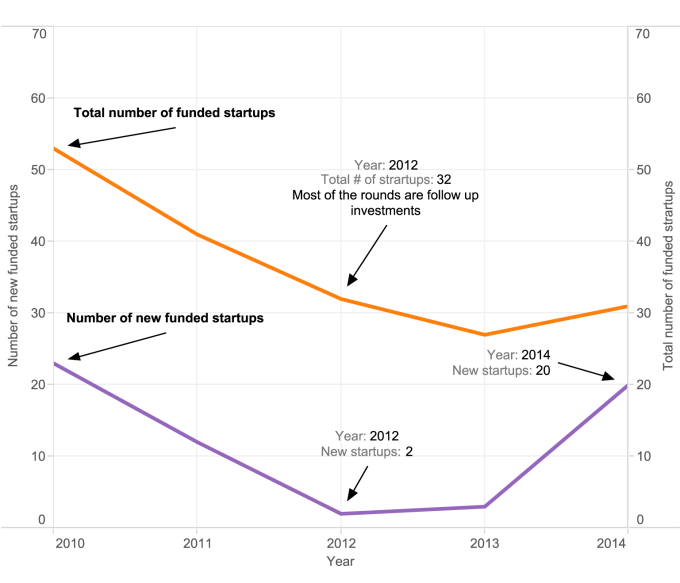

In the first half 2012 of the 32 investment rounds, only two of them were investments in new companies. The rest of the investments were follow-up rounds into companies funded before. The same trend continued during the first six months of 2013 with only three startups funded. However, this year there is a significant upward trend in new semiconductor startup funding with almost 20 new startups funded from January through June.

Also, it seems LPs have renewed interest in semiconductors and core technologies. Walden International recently raised a $100 million semiconductor fund. Also, I heard some rumors about one of the foundry companies considering launching a startup incubator/accelerator program.

Lack of funding has been a dominant pain point for capital-intensive startups for the past few years. However, it appears investors are coming back to this space. I hope the trend continues and fuels core technology innovation, enabling a new generation of IoT devices and creating industry changing applications.

Sources: