There are almost 900 million active cell-phone users in India now, and from newer startups to some of the biggest companies in the world, everybody is chasing the next mobile disruption that could potentially result in a business model for all of the emerging markets.

One such startup is Ezetap, a mobile payment company backed by some of the biggest names in the VC industry, including Chamath Palihapitiya, a former Facebook executive and founder of Social+Capital Partnership, and Angelprime, an Indian seed fund run by serial entrepreneurs.

Today, Ezetap is raising $8 million in Series B funding led by Helion Advisors, Social+Capital and Berggruen Holdings. This round takes the total fund raised by Ezetap to around $11.5 million (including $3.5 million it had raised in Series A funding in November 2012). The fresh capital will be used to expand Ezetap in Asia-Pacific, Middle East and Africa.

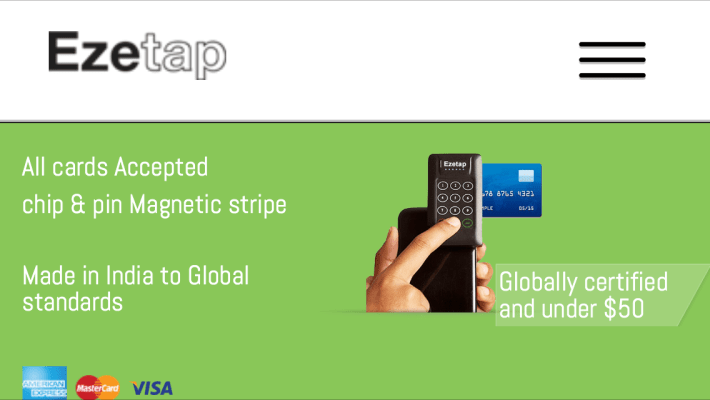

Ezetap is much like Square, at least in terms of the basic model. It uses a rectangular device that can turn any mobile phone into a point-of-sales terminal when plugged in. The device including a card reader and chip, costs around $50, and Ezetap has been able to sell around 12,000 of them to date. The startup is aiming to have over 100,000 such devices installed across Asia-Pacific, Africa and Middle East in a year.

“From day one, we wanted to go global and really felt that mobile payments in general is a great opportunity for emerging markets. There’s disparity in cash versus electronic payments leading to the challenges of financial inclusion,” Abhijit Bose, CEO of Ezetap, told TechCrunch.

Ezetap was incubated in 2011 by Angelprime, a $10 million seed fund backed by Mayfield Fund, Palihapitiya and several others in the Silicon Valley. It’s run by three veteran entrepreneurs — Sanjay Swamy, Shripati Acharya and Bala Parthasarathy. With the latest round, Ashish Gupta of Helion is joining the startup’s board. Helion is an India focused, $600 million fund.

Ezetap is the second attempt by Abhijit and Sanjay to build a mobile payment company in India. In 2006, Sanjay was the CEO of mChek which had raised around $10 million by 2009, and Abhijit worked with another venture-funded payment startup called Ngpay.

Back then, mChek and several others fizzled out because of several challenges.

“I believe there was nothing wrong with mobile payment back then, it was just the timing,” said Bose.

Indeed, the environment has changed dramatically. Back then, there were only 10 million credit cards. Today there are around 316 million credit and debit card holders in India. More importantly, the telecom infrastructure has improved tremendously, allowing users to do much more than just voice calls and texting.

“For us, Android and iOS are the game changers, too. Moreover, consumers are much more willing to use mobile payments for ease of use,” said Bose.

After building the product for one year, Ezetap officially launched with a Citibank mobile payment pilot in January 2013. Since then, the startup has signed up several banks and newer e-commerce companies, including Flipkart and online grocery retailer BigBasket. In Kenya, Ezetap partnered with Mastercard and Equity Bank to launch its services in March last year. Later in May 2013, Ezetap’s solution received global certification from EMVCo, an organization that specifies processes and gives approval for chip-based payment cards.

“Chip and pin is now the established global standard for mobile payment processing, and will soon take over the U.S. as well. Ezetap has created the only product that is certified globally, at a price point materially better than any other player – regional or otherwise,” said Palihapitiya.

Both Ezetap and Square are using similar models to enable mobile payments, but for completely different target markets, which is perhaps why Bose doesn’t like being called “the Square of India.” Ezetap’s merchants include India’s biggest e-commerce company Flipkart and even much smaller mom-and-pop shops.

“I always hate it when people call it that [Square of India]. Fundamentally, we are attacking underserved markets and are both similar in thinking about mobile payments. But we want to build a business that makes us number one mobile payment platform in emerging markets,” said Bose.

To be sure, Ezetap is not the only mobile payment startup that’s beginning to do well. With around 2 million customers using its mobile wallet, MobiKwik is aiming to reach the 100 million mark in two years. While MobiKwik and at least two dozen others are offering mobile wallets, startups such as Mswipe are more similar to Ezetap. Mswipe raised its Series B funding earlier this year from investors including Matrix Partners. All these startups are shaping an ecosystem of mobile payments in India that goes beyond just creating a non cash economy.