Boku is debuting a brand new mobile payments platform today, that aims to disrupt the current way that consumers pay for goods via their mobile phones or credit cards. As you may remember, Boku offers an online payments platform that allowed users to pay for online goods by charging the transaction to their mobile phone bill. When a user wants to purchase a virtual item, he can enter his cell phone number on a site, the site sends a text message to the phone, the user confirms the transaction with a short reply, and all the charges show up on his phone bill.

With Boku’s new product, called Boku Accounts, the startup is expanding online mobile payments technology to cover e-commerce and retail point-of-sale payments. The payments platform, which will be licensed to carriers, will be embedded on users’ mobile phones as well as via a pre-paid Mastercard credit card.

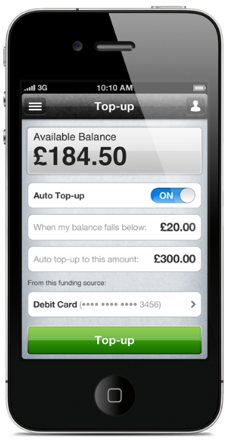

Basically there are three prongs to Boku’s payments platform: the consumer, the carrier and the merchant. Here’s how it works. The Boku Accounts platform allows carriers to issue their subscribers a branded mobile payment account accessible via both mobile device and the Web. Using an NFC sticker that can be adhered to the phone, and the prepaid credit card, subscribers can make payments online, in-app, and in-store. In-store purchases via Boku accounts will be enabled anywhere credit cards are accepted.

Merchants can work with carriers to target subscribers with personalized deals and offers as well as access to loyalty programs. Subscribers can pay via NFC or their pre-paid Mastercard (branded by the carrier), which they are able to add money to. A mobile subscriber will receive a Boku Account from their carrier, which includes a branded mobile payments account, online and mobile access (Web, iPhone, Android, and HTML5) and more.

Consumers can not only access special offers from participating merchants but can also access a Mint-like platform that tracks their spending via the payments platform. So consumers will be able to see how much they spent on restaurants, transportation and more categories in a given month,

Additionally, subscribers can send and receive money via person-to-person transactions completed by phone.

As Boku’s President Ron Hirson explains to me, this is Boku’s “most significant announcement since its launch.” “We want to go to everyday purchases and help change the way that cash is transacted,” he says. He adds that while NFC reach is currently limited, he feels there is potential for the technology to be more widely adopted.

It’s important to note that carrier partnerships are key for Boku to expand this offering. This platform is completely dependent on carriers adopting this as a way to offer mobile payments for its subscribers. It’s a white label offering.

And Boku Accounts is not contingent on merchant adoption. Even if merchants don’t opt in to create offers or deals, users can still use the payments option via the credit card or NFC chip (at NFC enabled terminals). For now, Boku isn’t ready to announce any carrier partnerships yet but Hirson says the company currently has a trial running with a major carrier in the U.K.

It will be interesting to see if Boku can land any major carriers in the U.S. It’s unclear what the financial terms will be at this point (we do know Boku does take a rev share on merchant offers), but even one carrier partnership could be potentially huge. Boku has been increasingly negotiating direct carrier partnerships for its online mobile payments offering, so the company is certainly familiar with this territory.

With its mobile payments products for online transactions, Boku mainly faces competition from eBay-owned rival Zong. With this new technology, Boku now finds itself competing with NFC-enabled platforms like Google Wallet as well as PayPal’s new retail point of sale system. Hirson doesn’t see BOKU Accounts as competitive to Google or PayPal though. He believes that because Boku isn’t requiring merchants to re-terminalize, or add any new technologies to the actual payment experience since Boku’s platform uses a prepaid card in addition to NFC.

This new platform is debuting ahead of a new funding announcement that Boku is expected to disclose (along with a new carrier investor) next week. To date, Boku has raised $38 million from Andreessen Horowitz, Benchmark Capital, DAG Ventures, Index Ventures and Khosla Ventures.