New York City startup BankSimple today disclosed that it raised its first venture funding in a round led by First Round Capital, Roger Ehrenberg’s IA Ventures, and Village Ventures, along with seed investors SV Angel (Ron Conway) and Nauiokas Park, and Jerry Neumann. But it did not disclose how much it raised. I’ve confirmed that the round was $2.9 million, with an additional $190,000 raised last year in convertible debt (which converted to shares with this round), for a total of $3.1 million raised. Not exactly “a big round,” but more than enough for what BankSimple is trying to do.

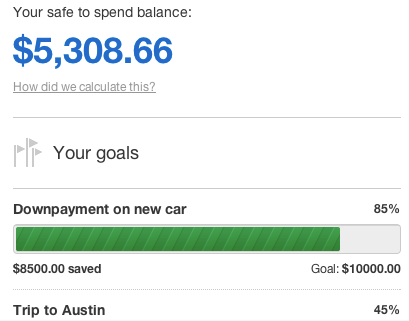

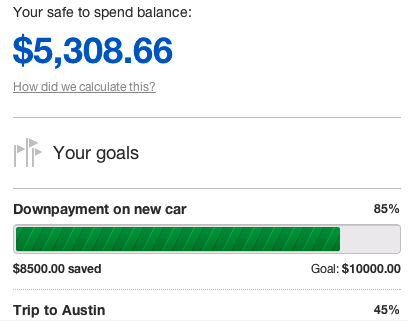

BankSimple has not yet launched. It is trying to develop a better interface for banking, working with financial institutions to actually hold the deposits. “Anything the customer sees is what we do,” says CEO Joshua Reich. BankSimple is creating a new front-end experience for bank customers both online and through mobile apps. The service will simplify their accounts into a single account and gives them a dashboard to see how much they are saving, how much they can spend, and how close they are to reaching financial goals.

The whole point is to simplify people’s financial lives by giving them a modern Web interface and realtime data linked to their accounts. So when you are about to reach an overdraft, you might get a notification on your phone. The first customers will be required to own a smartphone so they can download one of BankSimple’s mobile apps (iPhone and Android will probably be first). They will be able to deposit a check by taking a picture of one with their cell phone camera. Customers will also get a bank card tied to their account.

“The way banks work is they shove products down the throats of consumers,” says Reich. The more products you sign up for with your bank, the more fees they can charge. BankSimple will not make money from fees. Instead it will split the net interest margin with its partner banks (the net margin interest is the difference between the rate at which banks lend out money and the rate at which they pay depositors). It is looking to partner with wholesale banks to take care of the back end.

This strategy of focusing solely on the user experience contrasts with Betterment, a TechCrunch Disrupt finalist which also tries to simplify the online banking experience with a single, smarter account, but does hold deposits. Reich acknowledges that “we would certainly get more revenues if we did it ourselves,” but does not want to be distracted by regulatory compliance and managing large pools of money. Plenty of banks do that better than BankSimple could. Instead he wants to focus on what banks don’t do well: building a technology company and making the customer experience less harrowing.