The United States and China have long been ahead of the pack when it comes to robotics funding. However, data from 2022 is showing that these innovation hubs may have some serious competition as the investment landscape in Europe is starting to outstrip robotics’ biggest players.

The quest for technological supremacy has often been seen as a two-horse race between the U.S. and China. Over the years, we’ve only seen this investment tug-of-war intensify as both economies have vied for dominion to become an innovation superpower. Whilst in the past robotics has seen a similar dynamic, based on 2022 data, investors are starting to place their bets on an up-and-coming contender: Europe.

In 2022, nearly $8.5 billion in funding flowed into robotics companies worldwide — a staggering 42% less than the year prior – in line with the overall global downturn in VC investment. Yet despite the change in economic situation, with total USD investment volume into robotics falling by over 50% for both the U.S. and China between 2021 and 2022, Europe has seen a far more modest decline, only dropping 5% in the same period. Although it’s still early, we’re convinced it’s just the beginning of how Europe is finally beginning to find its place within the modern robotics ecosystem.

Europe emerges as a serious contender with a strong rate of growth

Whilst in the past robotics has seen a similar dynamic, based on 2022 data, investors are starting to place their bets on an up-and-coming contender: Europe.

When we compare Europe’s rate of growth in investment volume within robotics to the U.S. and Chinese markets, we observe a few key trends driving the continent’s recent power play in the robotics market.

With a CAGR of 28% in the period from 2018 to 2022, Europe is already surging ahead compared to global growth figures at 2%. This growth is primarily being led by Germany, which has seen a 77% growth spurt of investment volumes into the robotic space.

Close neighbor France has seen a 54% increase in robotic investment amounts. Meanwhile, robotics powerhouses China and the U.S. have experienced a decline in growth, with robotics investment falling 5% and 2% respectively since 2018.

China and the U.S. experience a 60% slow-down in growth/late-stage funding

To better understand these market shifts, we need to take a deep dive into the funding landscape and explore the state of play by funding rounds.

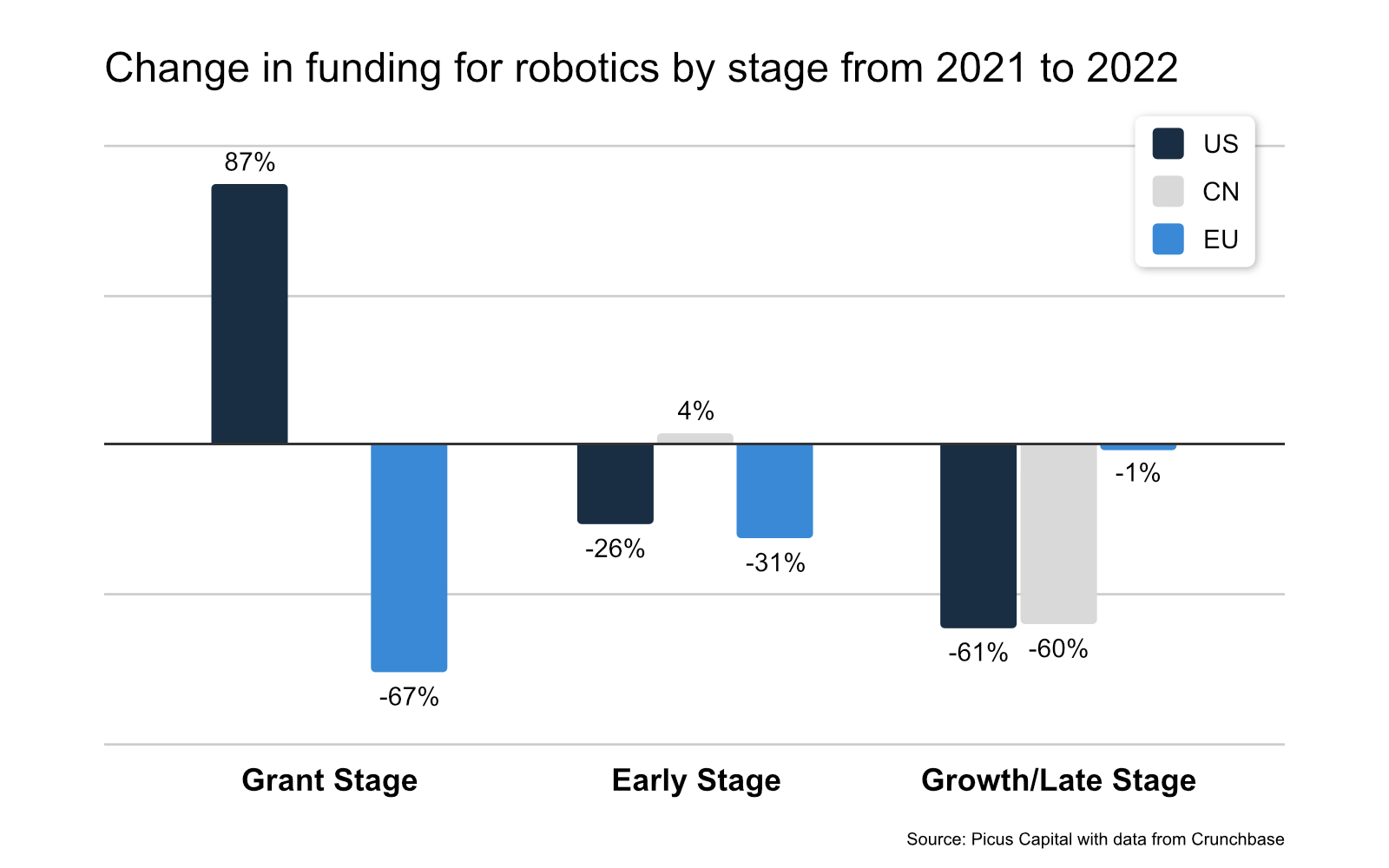

Slicing our data into grants, early-stage (pre-seed to Series A) and growth/late stage (Series B and onwards), we observed a major slow-down across U.S. and China robotics funding across growth and late-stage investment rounds.

Both the U.S. and China saw a decline of growth/late-stage robotic investment volume by 60% compared to 2021. Meanwhile, looking at the European market, the total investment volume for growth and late-stage deals was only slightly less than those of 2021.

Surprisingly, China has seen an 4% uptick in early-stage investments, whilst Europe and U.S. followed a similar downward trend – a potential sign for new ventures brewing. The trends in the growth/late -stage funding environments, accounting for the lion’s share in terms of investment volume, helps understand the relative stability in Europe.

Comparison in investment volume between 2021 and 2022 across geographies. Image: Picus Capital with data from Crunchbase

Under the surface, 2022 saw more European robotic firms consistently raise capital — 20 growth/late-stage rounds — and fewer outliers driving investment volume. By comparison, European robotics investments in 2021 were more prominently driven by outliers across 13 growth/late-stage rounds with an average round size of $108M USD. Meanwhile, the U.S. and China have seen a decline across a number of deals and mean & median investment amounts.

Growth/late-stage funding is complex. Nevertheless, we think that one dynamic influencing the change in investment volume discrepancy between U.S., China, and Europe is the shift in priorities for growth and late-stage funds – from growth to profitability. The continued funding into European robotic companies at these stages indicate that these companies are able to meet growth stage criteria better than U.S. companies. This is what we believe will also continue to be relevant throughout 2023.

Three factors are driving European investment

With the above trends – Europe is poised to become an attractive robotic market — both for investments and robotic firms to sell into. There are three key reasons why the continent continues to have a pull on investors.

1. European demand for automation is rising

With a recent study showing that over 60% of SMES [source: Fruitcore] in Europe are actively looking for automation solutions to improve process inefficiencies and labor shortages, it’s clear there’s a huge market pull for automation across the continent. When we couple this with shifts in the space from new players like RobCo, Fruitcore, and Coboworx, who have taken huge strides to improve procurement transparency and customer journeys, it’s easy to see how European companies have been able to drive strong fundamentals.

2. Europe has developed a strong geographical footprint

Over the last five years, a surge in interest in robotics has steadily made its way across the continent, ultimately creating a nexus of robotics firms across central Europe & UK, including Germany, France and Switzerland. Unsurprisingly, this has resulted in a shift in funding.

Within individual banner nations, we’re also seeing a strong trend towards talent diversification — both in terms of background and across local geographical borders. In Germany, for example, funding of more than $10M USD was often concentrated across Munich and Berlin back in 2018. But in 2022, that picture is starkly different and far more dispersed across seven major city hubs exceeding $10M in funding.

Shift in funding landscape within Europe – towards central Europe with France, Switzerland and Germany. Image: Picus Capital/Crunchbase

Meanwhile in the U.S., innovation and funding concentration has largely remained unchanged between 2018 and 2022, with California still the country’s main hub for robotics investment. In 2018, there were 17 states that had more than $10M funding coming in. In 2022, 15 states had more than $10M funding inflow for robotics.

For Europe, it seems like the old wisdom of not putting all of your eggs in one basket could be their biggest competitive advantage. Given the interdisciplinary nature of robotics, Europe’s diversification across geographical and talent borders could ultimately become highly influential to its continued growth.

3. European higher education is creating a strong pipeline of future robotics talent

With future generations the key to shaping the robotics industry, Europe has become a major player for robotics higher education, cultivating a strong network of universities across the continent, says Picus Capital founder and managing director Robin Godenrath.

Germany’s higher education institutes, including TU Munich and KIT, Switzerland’s ETH and EPFL, KTH in Sweden, and Imperial College London and the University of Oxford in the UK are all known centers of excellence for robotics education. Meanwhile, a strong framework for grants and programs means technical founders have the support to spin out their innovations alongside friendly terms for IP transfer.

2023 is the year to invest in Europe’s robotics scene

With 50% less capital overall invested into the European robotics market, it’s clear that Europe still has a way to catch up in comparison to the U.S. and China — but there’s a lot to be excited about. Moving into 2023, we’ll continue to see a strong demand for automation solutions catered to SMEs, such as those offered by RobCo, Unchained Robotics, or Coboworx.

Another industry in change is that of heavy machinery automation through human in the loop operation across multiple verticals – such as Fernride for freight intralogistics and Gravis Robotics for construction. With OpenAI’s recent investment in Norwegian based 1X — previously Halodi — we’re also poised to see the ripple effects of generative AI in the robotics domain.

And while robotics may remain a challenging space for many VCs to enter, all signs are pointing towards an era of robotics not only in Europe, but globally. For any investors still on the fence about Europe’s potential, we’d argue that now is the right moment to capitalize on the unique market conditions, technology trends, and talent.

This is as much an opportunity for VCs as it is for entrepreneurs looking to stake their claim in the space. A very strong market pull, strong ecosystems that foster innovation, and an influx of talent could just signal that Europe is on the cusp of a golden era for robotics.

Picus Capital is an investor in Coboworx.