Entrepreneur Ankur Nagpal raised a $70 million venture fund last year, called Vibe Capital, from over 200 investors. But now, as the market shifts and LPs are less interested in venture capital, the Ocho founder is shrinking the fund side by roughly 43%, canceling capital calls, and, ultimately, sending back money that had already been wired to the fund.

The contraction, Nagpal told TechCrunch, occurred because he’s busy building his own startup and the funding environment has shifted to more realistic expectations: “What looked like a $10 billion outcome is now a $1 billion dollar outcome.” As a result, he says he’s more confident on returning a higher multiple if he’s investing from a smaller fund size.

His LPs were surprised but “super happy” to get the capital back, Nagpal said. Since announcing the cut, the founder says that five different solo GPs have messaged him asking for introductions to LPS who just got capital back. “I think the reality is a lot of these people who are getting money back are actually not going to allocate it to venture anymore.” One of Nagpal’s biggest investors is Tiger Global, which has become notorious for retreating from venture fund bets. His other investors, namely venture funds, will likely use the capital to bet on new startups out of their own fund, he said.

In Nagpal’s case, the move will let him put 90% of his time into his new startup. But he says others in the solo GP world are going through a rough time. Many are shrinking fund goals, extending fundraising timelines, teaming up with investors to avoid team risk or even going toward placement agents, once taboo in the world of fundraising, to help them close investors in exchange for a fee. “Even the ones who are taking it seriously are actually now trying to build a firm, so you’re kind of becoming the thing that you were trying to replace,” he said.

It’s a shift from the fund of fund mentality that felt commonplace last year, in which investment firms cut checks to early-stage, experimental investors to de-risk and even lead first checks into a generation of new startups. At the time, Tiger announced its $1 billion fund to back other funds but has since reneged. Other efforts, like Spearhead, a platform to turn founders into angel investors built by AngelList’s Naval Ravikant and Accomplice’s Jeff Fagnan, appear to no longer be as public or active as before. (Update: Accomplice’s Jeff Fagnan told TechCrunch that, while Spearhead has opted to be less public about its work, it has conducted 5 cohorts across 77 funds).

The history of solo GPs

Before solo GPs were in the spotlight, they were set aside. LPs weren’t giving lone venture capitalists meaningful capital, but as entrepreneurs with massive networks sought to formalize some of their angel investing operations, the deal sweetened. Add in the fact that platforms like AngelList made it easier and cheaper to set up a fund and handle all associated admin fees, and the jokes started rolling: Anyone with opinions and a following on Tech Twitter could start a fund.

But even the early indicators weren’t perfect. Nikhil Basu Trivedi called out the solo GP trend back in 2020. At the time, he wrote, “As it is, venture capital is a very difficult business to scale. When you’re operating on your own, it’s even harder. It will be fascinating to watch how many funds and how many portfolio companies the solo capitalists can manage before they run into bottlenecks.”

At the time, he also wrote that solo capitalists have a limit on how much they can raise. That in and of itself can greenlight LP interest because of the forced creative constraints that exist. (In 2021, Trivedi launched a fund co-founded by him and partner Mike Smith. It closed at $175 million).

Eventually, the solo GP movement and emerging fund manager movement combined to make a new box for LPs: allocations specifically to back a class of new, often diverse check writers.

Rolling funds, launched by AngelList, capitalized on the trend that let techies with big networks of accredited investors raise funds.

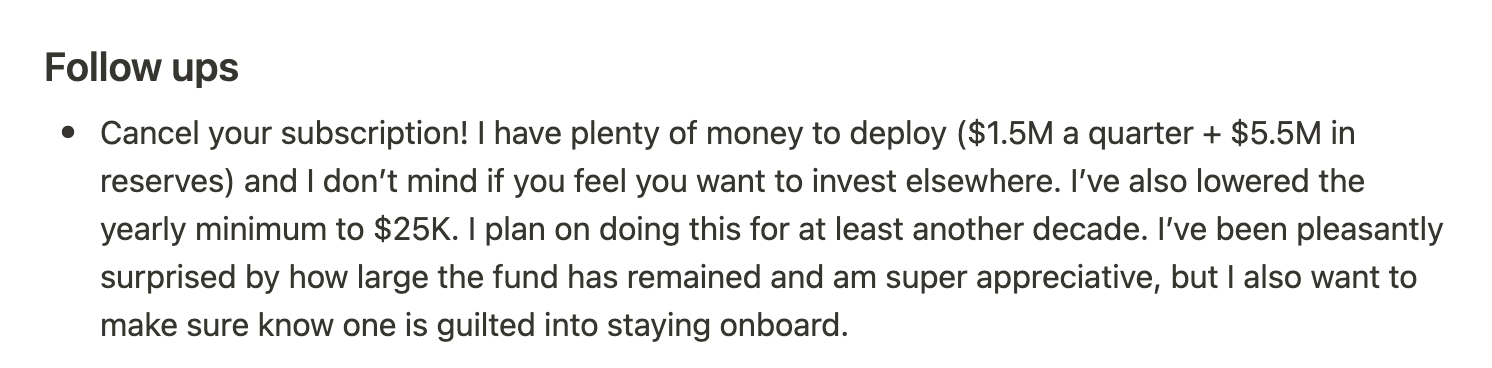

“Cancel your subscription”

Gumroad CEO Sahil Lavingia was one of the first creators to launch a rolling fund, which, at its peak, was closing around $13 million a year from quarterly investments. Now, as investors drop off venture as a whole, his fund is at $6 million. Lavingia attributes this to higher than normal interest rates and institutional risk going down.

The environment has changed so much that this week, he sent an email to LPs with a simple bullet point toward the end: “Cancel your subscription.” The reason, he tells TechCrunch+, is because the venture math has changed and he doesn’t want investors to feel guilty over a commitment they made months — or even years — ago.

Image Credits: Gumroad

Lavingia doesn’t plan on leaving the investing world but is comfortable with the ebb and flow of interest in the asset class: He’s betting that when interest rates dip back down, there will be a lot more money coming his way. As for the broader solo GP class, the entrepreneur thinks that there are two different challenges ahead.

First, rolling funds need investors who choose to stick with it on a quarter-over-quarter basis. That optionality could completely kill a fund over one quarter. “If you just raise from people from Twitter, you could go from 200 investors to zero,” he said. “[The optionality] could be like a bank run on your fund.”

On the other end, those who raised from institutional investors could have a harder time raising money in this environment versus those who pieced together a fund via super angels or high-net-worth individuals, Lavingia said.

“I can’t imagine an institutional LP is going to be as open minded to investing in a single person doing lots of investing on their own without a team or partnership model,” he said.

Where there’s hope

At Cendana Capital, Kelli Fontaine invests solely in early-stage venture capital funds around the world. She’s backed 01, Bolt VC, Better Tomorrow Ventures and Cake Ventures, and remains bullish on the idea of solo GPs.

“Our sentiment is that the biggest risk in venture is actually team risk. When you back a firm of people who have never built a firm together, there’s a risk that the partnership blows up,” she said. “For that reason, we’re biased.” While the investor does expect consolidation to happen in the solo GP world, Fontaine also argues that backing individuals will remain popular due to founder behavior.

“I believe that people have their own brands right, even if somebody is going to Andreessen or Sequoia, they’re choosing the partner they want to work with,” she said. “Back before social media days, the brand of the firm was more important. Now people have a reputation, and a brand is what they’re good at — so I do think that translates to solo GPs.”

Venture funds remain an open tap. For example, Bain Capital Ventures nearly doubled its last fund in a recent announcement of an early-stage and growth-stage investment vehicle duo. Despite the growth in assets under management, BCV isn’t dedicating a larger chunk of capital to backing emerging fund managers.

“We do suspect that [emerging fund] manager fundraising will decline,” BCV partner Kevin Zhang said, adding that he knows several managers who have opted to raise smaller debut or follow-on funds. “So we think even a constant dollar commitment will end up representing a large portion of ecosystem LP dollars.”

Sources tell me that Winter Mead is trying to raise a fund to back funds coming out of his accelerator, which is a Y Combinator-type platform, but for emerging fund managers.

The other way solo GPs are finding fresh capital is through 506(c) fundraises: Community raises in which investors pursue a vehicle that allows them to publicly advertise their venture funds to then raise from accredited investors. It’s like the crowdfunding version of venture, used by Banana Capital’s Turner Novak, Not Boring Capital’s Packy McCormick and Trust Fund’s Sophia Amoruso.

AngelList’s Abe Othman says that 506(c) fundraises are becoming more popular, and that they are a “function of the (very) challenging fundraising environment.” “506(c) is harder to raise. You have to do the accreditation verification, which is annoying and expensive,” he said. “But the benefit is that you get to talk about your fund.”

Revere co-founder Eric Woo started his company with the grand ambition of creating a platform for LPs to discover new venture funds. Since microfunds are “just getting completely whacked,” he said, the platform has inverted: GPs are coming to Revere asking to help discover new LPs, subjecting themselves to the platform’s rigorous vetting process and requirement to share financials and the nitty gritty details on fund structure.

“We thought it’d be like pulling teeth, to get GPs to come to us and share all this information and go through four to six weeks of this process,” he said. “Actually, they love going through this.”

If you have a juicy tip or lead about happenings in the venture world, you can reach Natasha Mascarenhas on Twitter @nmasc_ or on Signal at +1 925 271 0912. Anonymity requests will be respected.