News that former FTX CEO Sam Bankman-Fried was arrested yesterday in the Bahamas set the technology world alight.

After the dramatic implosion of FTX’s crypto empire, which resulted in the loss of hundreds of millions of invested capital and billions of paper wealth, many in the larger crypto community were incensed that he was not instantly arrested.

Now, with Bankman-Fried in custody and a complaint in hand, it is clear that the former startup executive had not purchased political protection, something alleged by humble anonymous Twitter accounts and the man who recently bought the social service alike.

The Exchange explores startups, markets and money.

Read it every morning on TechCrunch+ or get The Exchange newsletter every Saturday.

Legal folks will carefully dissect the complaint and provide more capable commentary on its aggregate claims. This morning, we’re going to take a different angle. What matters is that the FTX empire was, effectively, bullshit. It was, per the complaint, built on fraud.

This matters for startups because information about how other companies are doing is scarce and competition is intense. That means the leading startups’ business results carry outside influence — they become the cultural leaders in their market. When it turns out a screaming success was no more than smoke and mirrors, it means that a key signal in the tech startup market was actually quite specious.

I wonder how many founders looked at what the FTX crew claimed to have built and tried to ape something similar. I wonder how many regular folks saw billions being minted in crypto and put too much of their own capital not only into FTX but other crypto projects that imploded this year. I wonder how many investors, chasing the returns their rivals and peers were posting thanks to entities like FTX, are now sitting on a bunch of paper losses. I wonder how much money from regular folks — pension holders, university staff, etc. — was burned at an altar of greed and nonsense for no reason other than hubris and, let’s be fair, a lack of due diligence.

The entire situation is gross. But for the startup market, it was also a series of erroneous lessons during a time when investors and founders were nearly entirely operating in a risk-on fashion. And why not! FTX exploded out of nowhere, building wealth faster than nearly any company ever. It played a huge role in the last crypto supercycle, not only by taking capital that could have gone to legitimately useful projects, but also by using some of its allegedly misappropriated funds to fuel startup activity that, in retrospect, is likely more suspect than credible.

The entire situation is gross. But for the startup market, it was also a series of erroneous lessons during a time when investors and founders were nearly entirely operating in a risk-on fashion. And why not! FTX exploded out of nowhere, building wealth faster than nearly any company ever. It played a huge role in the last crypto supercycle, not only by taking capital that could have gone to legitimately useful projects, but also by using some of its allegedly misappropriated funds to fuel startup activity that, in retrospect, is likely more suspect than credible.

A piggy bank for hogwash

The U.S. Securities and Exchange Commission complaint alleges that Bankman-Fried shuttled funds between FTX and Alameda, a putatively independent company that, in fact, was not. The pair of companies — along with a host of subsidiaries — commingled customer and company funds, using the capital for a host of activities that it failed to disclose (or, allegedly, hid).

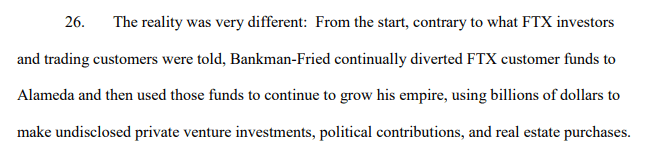

A few samples from the complaint to make the point. Here’s a note discussing how money moved from FTX customers to Bankman-Fried’s own projects:

That sounds like he used customer funds as his own! The complaint makes that particular allegation even clearer later on:

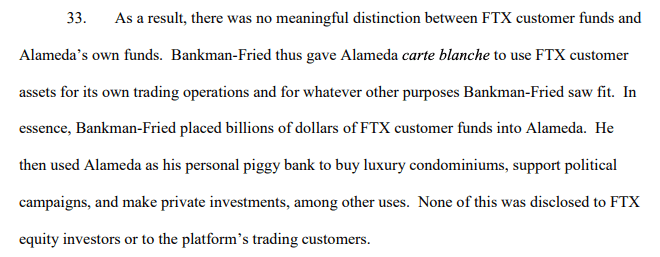

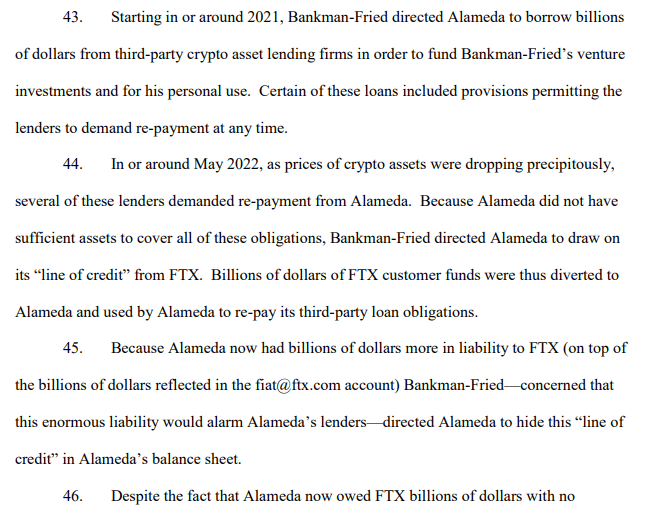

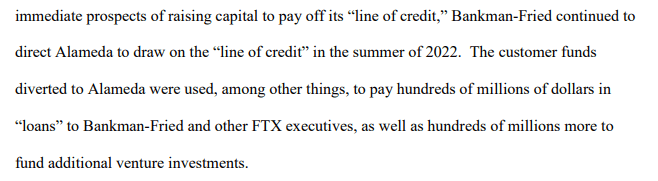

But that was not enough. Later, the complaint makes further allegations regarding the accumulation of funds and their purposes:

Bullshit! It was all, allegedly, bullshit! The money, the donations, the investments, the hype, the company, the business model — all allegedly complete and utter codswallop. A mess on stilts. A cautionary tale that will last until the very next bull market.

FTX money was in startups, in advertisements, in the halls of government, in the worlds of domestic and global sports. And a great portion of that activity appears to have been built not on the back of genius. Or business insight. Or a new approach to the physics of finance. But on a sleight of hand in which money was taken, spent and lost. Allegedly.

Someone much smarter than I am once said that a way to track a market cycle’s peak is to note when fraud really picks up. The argument, so far as I understand it, is that when a bull market reaches its zenith, investor and consumer demand for normal corporate controls and diligence fall by the wayside. Greed takes over. This creates an open season for fraudsters as their target market of marks is primed to talk themselves into a bad deal.

The issue with noting the peak of a market cycle is that we often don’t learn about alleged frauds until after the apex has passed and the damage is done. Such is the case, it appears, with FTX.

That doesn’t mean that other startups, founders and venture backers didn’t learn the wrong lessons from what appears to be a relatively boring — if massive — fraud that is newsworthy more because it was blockchain-based than novel. They probably did. And that’s a goddamn travesty, because, despite my generally cranky perspective on most things, I really do think that startups are a good and useful approach to corporate construction.

The core work of startups, creative destruction, gets me excited; the best antidote to monopoly is not the government but a marketplace so competitive that no single company can ever become too big to kill. FTX, instead of being an example of creative destruction, was simply creative in how it went about executing — allegedly — an old-school gambit in a new economy. For shame.