How much will the changing valuation profile of software companies impact the highest-flying private unicorns? Also, why hasn’t Databricks gone public yet? The answer to the former might be the answer to the latter.

TechCrunch has spent ample time since the end of 2021 tracking changes to the value of software revenues. To catch you up: A number of factors commingled to create a climate in which software companies are worth less now than they were during much of 2021 when valued on a revenue-multiple basis.

The Exchange explores startups, markets and money.

Read it every morning on TechCrunch+ or get The Exchange newsletter every Saturday.

One outcome of this particular matter has been concern that many startups that raised capital last year at a high price will struggle to defend — let alone advance — their valuations when they next raise capital. And since it is not expected that the startup asset class will suddenly become cash-flow-breakeven, more funds will be needed. This sets up an awkward situation in which external observers — which include potential employees, mind — cannot tell which startups that attracted external capital at an aggressive valuation are hollow and which are not.

But there is a particular class of company to consider, a subset of the high-priced startup cohort: the mega-unicorns. These companies — private-market former startups that have the highest valuations — are in theory those closest to going public.

But there is a particular class of company to consider, a subset of the high-priced startup cohort: the mega-unicorns. These companies — private-market former startups that have the highest valuations — are in theory those closest to going public.

My question this morning is just how the change in market valuation conditions impacts this small set of companies. So let’s go back to our prior work on Databricks, which most recently raised $1.6 billion at a $38 billion valuation, and see what the new reality can tell us.

What’s Databricks worth today?

A few data points to remind you of where the company stands:

- February 2021: Databricks raises $1 billion at a $28 billion valuation against ARR of $425 million.

- August 2021: Databricks raises $1.6 billion at a $38 billion valuation against ARR of $600 million.

- February 2022: Databricks announces that it closed 2021 with more than $800 million worth of ARR.

Those work out to revenue multiples of roughly 66x, 63x, and 47.5x.

While we don’t know precisely when Databricks reached each revenue milestone, and we are not able to know exactly how far ahead of $800 million in ARR the company was at the close of 2021, we can infer that the company was adding around $50 million in ARR per month in the final quarter of last year. As it has been nearly four months since the start of the year, we can loosely say that Databricks should be at the $1 billion ARR mark today, more or less.

That brings the company’s revenue multiple down to a far more modest 38x. Our question is whether that number makes any sense.

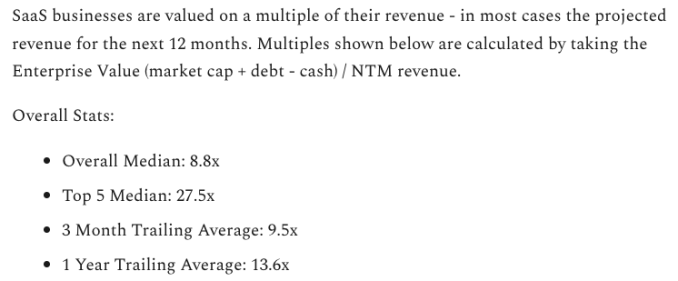

Leaning once again on Altimeter investor Jamin Ball’s regular dives into the changing value of cloud companies, we pick up from his April 15 entry:

For reference, that Top 5 Median number was 38.8x in February, when we last checked in on the Databricks situation.

If that valuation mark had held up, there would be little space between the value of the mega-unicorn and prevailing market conditions; indeed, Databricks could actually be considered a little cheap at that market multiple, given that we are calculating its revenue multiples using ARR, which is a little bit more conservative than NTM figures. (And we’re using market cap instead of enterprise value; one can only get so precise when covering private companies.)

Regardless, things have changed. And now with the Top 5 Median SaaS companies worth 27.5x their NTM revenues, is Databricks expensive? Er, kinda no? I don’t think so?

Let’s assume that Databricks exits April at a flat $1 billion ARR mark. That leaves eight months left in the year. And let’s also presume that Databricks sees steady growth at $50 million worth of ARR per month — a figure that would lead to a declining percentage growth rate, note. That would put Databricks at a roughly $1.4 billion run rate by the end of the year. At a $38 billion valuation, the company would exit 2022 with an ARR multiple of around 27x. Which, you will note, is somewhat bang-on for the current median for the most richly valued SaaS companies.

Would Databricks warrant a top-five valuation mark if it went public toward the end of the year? Yes, or close to it, if we understand its numbers correctly.

While it seems possible for Databricks to grow into its prior valuation this year despite a radically different software valuation landscape, the company is not there yet. Which is why I reckon it’s not trying to crack the IPO window open. If Databricks went public today, before it stacked a bunch more top line, it might have to concede on the valuation front. No one wants it to do that. And with simply enormous cash raises last year, the company is likely well-capitalized today and thus in no need of capital, meaning that an IPO can simply wait.

So the Databricks IPO is feeling more Q4 2022 or Q1 2023, if the market doesn’t improve. But the company should be able to do what Databricks CEO Ali Ghodsi told TechCrunch in a prior interview — that even if the market changes, companies can simply grow quickly and get through any particular trough. Yeah, some companies can.