Khatabook, a startup that is helping merchants in India digitize their bookkeeping and accept online payments, said on Tuesday it has raised $100 million in a new financing round as it prepares to launch financial services.

The startup’s new financing round — a Series C — was led by Tribe Capital and Moore Strategic Ventures and valued the two-and-a-half-year-old Bangalore-headquartered startup at “close to $600 million,” its co-founder and chief executive Ravish Naresh told TechCrunch in an interview.

As part of the new round — which was oversubscribed and also saw participation of Balaji Srinivasan and Alkeon Capital as well as many other existing investors including Sriram Krishnan, B Capital Group, Sequoia Capital, Tencent, RTP Global, Unilever Ventures and Better Capital — Khatabook said it is also buying back shares worth $10 million to reward its current and former employees and early investors. The startup said it is also expanding its stock options pool for employees to $50 million

Even as hundreds of millions of Indians came online in the past decade, most merchants in the South Asian nation are still offline. These merchants, who run neighborhood stores, rely on traditional ways for bookkeeping — maintaining ledgers on paper — that are both time-consuming and prone to errors.

Khatabook is attempting to change that by providing these merchants with a suite of products to digitize their bookkeeping and manage their expenses and staff. The startup, which employs over 200 people, said it has amassed over 10 million monthly active users who are spread across nearly every zip code in the country.

Scores of firms from young startups such as Khatabook and Dukaan to Facebook, Amazon and India’s largest retail chain Reliance Retail are aggressively attempting to tap into neighborhood stores in the South Asian market.

There are about 60 million small and medium-sized businesses in India, a fraction of which are neighborhood stores — also popularly known as kirana in South Asia — that dot tens of thousands of Indian cities, towns and villages. These mom-and-pop stores offer all kinds of items, pay low wages and little to no rent. And on top of that, their economics is often better than most.

“At Tribe, we believe strongly in the power of the network effect and how it can create moats for businesses. Khatabook has successfully built such a network by empowering this seismic shift among MSME businesses to move from paper to digital, literally,” said Arjun Sethi, co-founder and partner at Tribe Capital, in a statement. “Despite its large early success and fast adoption to date, the company is early in its path to power the segment. We’re thrilled to be a part of its growth as it leverages its network to build additional scale.”

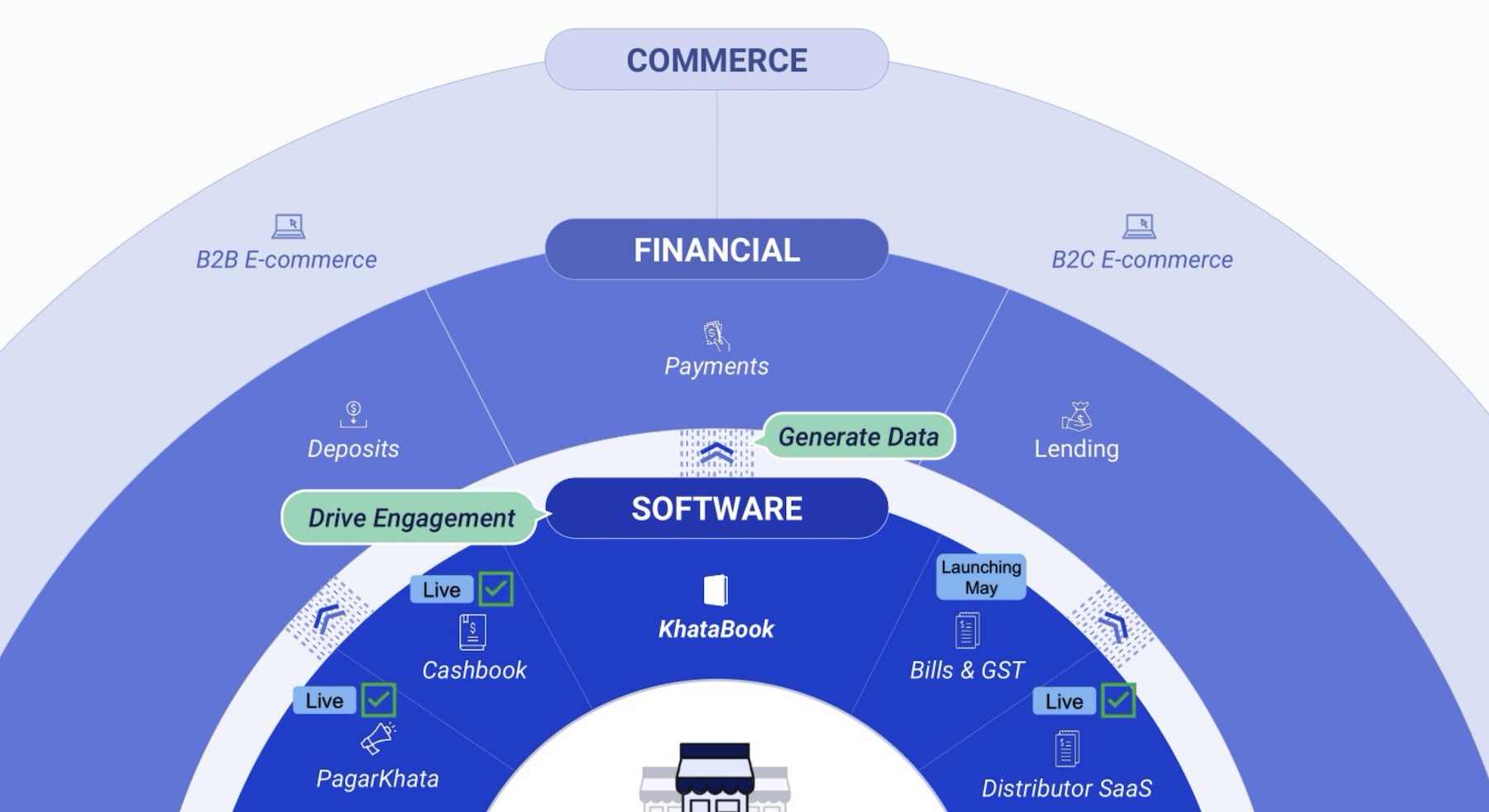

A slide from a recent deck of Khatabook. Image Credits: Khatabook

Khatabook, which also counts Emphasis Ventures (EMVC) among its backers, has expanded its product offerings in recent years to lure more businesses. Later this year, Naresh said, the startup will provide lending to merchants. “We are currently testing the product with both retailers and distributors,” he said.

Online lending has boomed in India in recent years, but very few companies are today attempting to cater to small and medium-sized businesses. “The unaddressed SME credit demand in India is ~$300 billion-$350 billion, with more than 90% of current demand being met by banks. A typical digital SME lender focusses on 1 million-5 million Indian rupees ($13,575 to $67,875) ticket size with no collateral, average tenure ~12-18 months, and with some ecosystem anchor,” analysts at Bank of America wrote in a report.

As with scores of other firms, the pandemic was not good news for Khatabook, which lost a significant portion of the business last year after Indian states enforced lockdown to restrict mobility. But the startup has since bounced back. The month of July, said Naresh, was its all-time high. “MSMEs have come back very strongly and businesses were not as impacted by the second wave this year as they were by last year’s,” he said.