What a difference a week makes.

This time last week, in the wake of earnings from tech’s five largest American companies and early results from other software companies, it appeared that tech shares were in danger of losing their mojo.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But then, this week’s rally launched, and more earnings results came in. Generally speaking, the Q3 numbers from SaaS and cloud companies have been medium-good, or at least good enough to protect historically stretched valuations when comparing present-day revenue multiples to historical norms.

This is great news for yet-private startups that have had to deal with a recession, an uneven and at-times uncertain funding market, an election cycle and other unknowns this year. Wrapping 2020 with a market rally and strong earnings from public comps should give private software companies a halo heading into the new year, assisting them with both fundraising and valuation defense.

Of course, there’s still a lot more data to come in, markets are fickle and many SaaS companies will report next month, having a fiscal calendar offset by a month from how you and I track the year. But after spending time on the phone this week with JFrog’s CEO, BigCommerce’s CEO and Ping Identity’s CFO, I think things are turning out just fine.

Of course, there’s still a lot more data to come in, markets are fickle and many SaaS companies will report next month, having a fiscal calendar offset by a month from how you and I track the year. But after spending time on the phone this week with JFrog’s CEO, BigCommerce’s CEO and Ping Identity’s CFO, I think things are turning out just fine.

Let’s get into what we’ve learned.

Growth and expectations

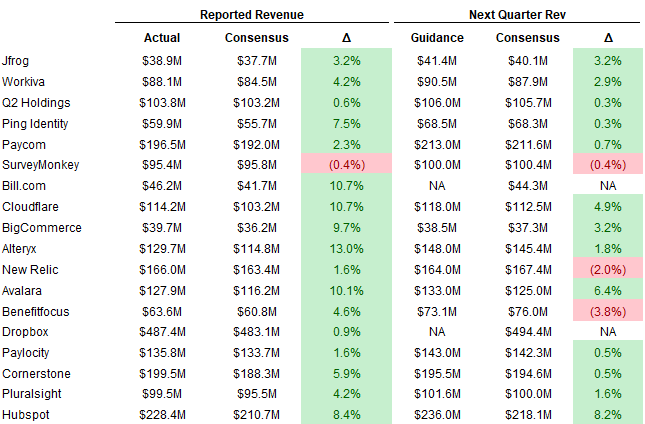

Kicking off, Redpoint’s Jamin Ball, a venture capitalist who unconsciously moonlights as the research desk for the The Exchange during earnings season, has a roundup of earnings results from this week’s set of SaaS and cloud stocks that reported. As you will recall, last week we were slightly unimpressed by its cohort of results.

Here’s this week’s tally:

As we can see, there was a single miss amongst the group in Q3. Unsurprisingly, that company, SurveyMonkey, was also one of three SaaS companies to project Q4 revenue under street expectations. My read of that chart is seeing a little less than 80% of the group that did project Q4 guidance that bests expectations is bullish, as were the Q3 results, which included a good number of companies that topped targets by at least 10%.

Inside of the data are two narratives that I want to explore. The first is about COVID-related friction, and the second is about COVID-related acceleration. Every company in the world is experiencing at least some of the former. For example, even companies that are seeing a boom in demand for their products during the pandemic must still deal with a sales market in which they cannot operate as they would like to.

For software companies, reportedly in the midst of a hastening digital transformation, the question becomes whether or not the COVID’s minuses are outweighing its pluses. We’ll explore the matter through the lens of three companies that The Exchange spoke with this week after they reported their Q3 results.

Ping Identity

Of our three companies this week, Ping Identity had the hardest go of it; its stock fell sharply after it dropped its Q3 numbers, despite beating earnings expectations for the period.

The company’s revenue fell 3%, while its annual recurring revenue (ARR) rose by 17%. Why did its stock fall if it came in ahead of expectations? You could read its Q4 guidance as slightly soft. In the above chart it’s marked as a slight beat, but its low-end came in under analyst expectations, creating the possibility of a projected miss.

Investors, betting on Ping’s move to SaaS being accretive both now and in the long-term, were not stoked by its Q4 forecast.

I chatted with CFO Raj Dani about Ping’s results, and he said that after a COVID-related shock in the first quarter, deal activity recovered. But, deals were increasingly phased, including things like slower rollouts. This flagged Ping’s growth somewhat, despite its leadership firmly believing that in an increasingly remote world, identity products have a key role to play in enterprise IT.

In its earnings notes, Dani said that “contract durations for both new bookings and renewals have begun to normalize more closely to pre-COVID levels,” which is good, but also that “prevailing economic uncertainty driven by COVID-19” had changed enterprise buying patterns, leading to “slightly smaller deal sizes and a reduction in our dollar-based net retention rate.”

Ping is bullish about its pipeline in both the world’s largest companies, per our chat with the executive. It expects to convert its pipeline into revenue. Just not as fast, perhaps, as investors expected.

Things could accelerate for Ping in Q4 faster than it has projected, but the company’s Q3 beat and stock decline explain both how high investor expectations are and that the public markets has its eyes firmly on future growth at the expense of recent performance. There’s a lesson in there for startups.

JFrog

Next JFrog, which beat revenue expectations in Q3 and missed on fully loaded profit. Its Q4 revenue projection came in ahead of expectations.

JFrog, you will recall, was a rare software company that went public this year with a history of making money. Its ability to grow — around 40% in its most recent quarter, compared to its year-ago number — and generate adjusted profit make it a neat anomaly as we keep tabs on the financial performance of software companies.

The Exchange chatted with JFrog CEO Shlomi Ben Haim about the quarter and what Ping had told me before our call about its own COVID-related performance.

Per Ben Haim, there are COVID effects in the market. However, he quickly pivoted to detailing why JFrog’s model is different than most companies’ and is working even during the pandemic. According to the CEO, JFrog approaches sales via a bottom-up approach, eschewing a heavy, standard enterprise sales model that spends lots of cash to generate ARR. This means that JFrog was less impacted by the cessation of most business travel, conferences and other things that more traditional sales orgs leaned on, we’d suppose.

Ben Haim also noted that JFrog was seeing record demand from developers, allowing his company to increasingly run industry-segmented confabs to better go after its market. The CEO also praised JFrog’s new free tier and cloud flexibility as a way that the company is driving demand apart from any COVID-induced boost to appetite for DevOps tooling.

While Ping Identity expects the market to keep moving in its direction even as some deals are rolled out more slowly, harming near-term growth, JFrog’s sales model is helping it surf the changes that COVID has brought in real time. But, in each case, we see a company that believes that the market is moving in its direction. Software then, should continue to win if they are right, just at different rates depending on sales models, and customer mix.

BigCommerce

Moving to BigCommerce, I got on the horn with CEO Brent Bellm, someone I’ve been chatting with here and there since his company filed and went public earlier this year, to chat about his company’s most recent performance. Q3 was a good period for the company, frankly.

Here’s how BigCommerce’s growth rates have gone in recent quarters:

- Q1 2020: +30% YoY

- Q2 2020: +32% YoY

- Q3 2020: +41% YoY

Seeing an already public software company accelerate its revenue growth in percentage terms is impressive, and rare.

Two things are happening at BigCommerce. First, Bellm told us that COVID’s e-commerce bump is real, and not bad for his company. That is unsurprising. Second, Bellm highlighted that BigCommerce has benefited from going public, arguing that having his company float has provided visibility into its performance and operations, helping it land more customers.

On strictly the COVID front and current earnings front, it appears that BigCommerce is seeing much more COVID-related acceleration than friction. Adding this to what we saw from Ping and JFrog, it certainly seems that more software companies than not are seeing the balance of COVID-induced market changes wind up as net-positive.

We can see this from our interview notes and from the chart of Q3 performance and Q4 expectations.

Provided no external shocks, software shares could enter 2021 in good standing. For startups hoping to raise once VCs get back from vacation, it’s a great week of news.