No company is completely insulated from the macroeconomic fallout of COVID-19, but we are seeing some companies fare better than others, especially those providing ways to collaborate online. Count Atlassian in that camp, as it provides a suite of tools focused on working smarter in a digital context.

At a time when many employees are working from home, Atlassian’s product approach sounds like a recipe for a smash hit. But in its latest earnings report, the company detailed slowing growth, not the acceleration we might expect. Looking ahead, it’s predicting more of the same — at least for the short term.

Part of the reason for that — beyond some small-business customers, hit by hard times, moving to its new free tier introduced last March — is the pain associated with moving customers off of older license revenue to more predictable subscription revenue. The company has shown that it is willing to sacrifice short-term growth to accelerate that transition.

We sat down with Atlassian CRO Cameron Deatsch to talk about some of the challenges his company is facing as it navigates through these crazy times. Deatsch pointed out that in spite of the turbulence, and the push to subscriptions, Atlassian is well-positioned with plenty of cash on hand and the ability to make strategic acquisitions when needed, while continuing to expand the recurring-revenue slice of its revenue pie.

The COVID-19 effect

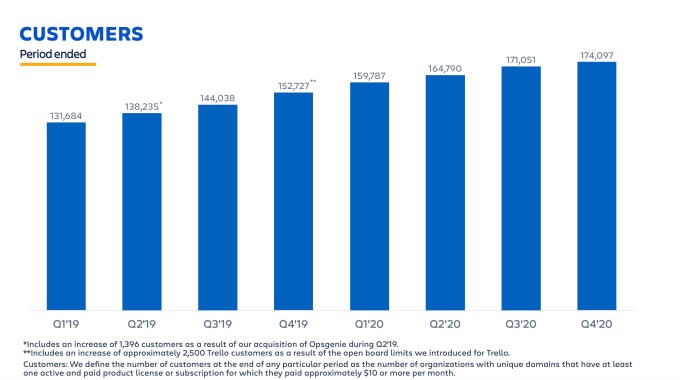

Deatsch told us that Atlassian could not fully escape the pandemic’s impact on business, especially in April and May when many companies felt it. His company saw the biggest impact from smaller businesses, which cut back, moved to a free tier, or in some cases closed their doors. There was no getting away from the market chop that SMBs took during the early stages of COVID, and he said it had an impact on Atlassian’s new customer numbers.

Image Credits: Atlassian

Still, the company believes it will recover from the slow down in new customers, especially as it begins to convert a percentage of its new, free-tier users to paid users down the road. For this quarter it only translated into around 3000 new customers, but Deatsch didn’t seem concerned. “The customer numbers were off, but the overall financials were pretty strong coming out of [fiscal] Q4 if you looked at it. But also the number of people who are trying our products now because of the free tier is way up. We saw a step change when we launched free,” he said.

The sheer number of customers it has and the diversity in size and type helped insulate Atlassian from some of the vagaries of COVID. The pandemic did not have much impact on its customer contracts because they are set up for one to three years. All the same, Deatsch definitely sees some challenges ahead: “As we look into our fiscal year starting July 1, we still know there’s macroeconomic challenges out there. [ … ] We do know and we’re planning that it’s going to have some sort of effect financially on our business, but there’s so much unknown that it’s hard for us to predict what that will look like,” he said.

Overall though, Deatsch says that Atlassian plans to move aggressively with plans to hire 1000 people in the coming year, and says the company is in a strong enough position financially to ride out whatever happens.

Moving to SaaS

If our notes so far seem cautious about Atlassian it’s because the company is working through a business model transition from license to SaaS, while digesting a distribution model shakeup — trials to freemium — all during a global pandemic and recession. That’s never going to be a great mix for short-term results that will blow your sneakers off.

But it is a way to keep redesigning your company for the long term, macro conditions be damned. In fact, Atlassian is executing the same type of transformation that Adobe and Microsoft have pursued, shifting the bulk of its revenues from license to software as a service, swapping chunky, episodic revenues for regular, recurring ones. A move to SaaS is effectively mandatory in 2020, and thus Atlassian is doing the right thing according to standard market wisdom.

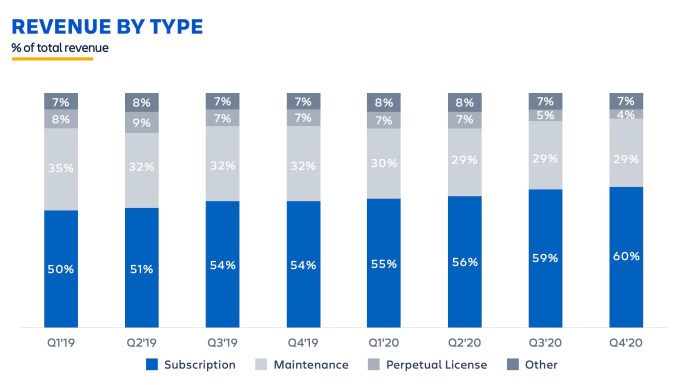

In the past year, Atlassian has seen its revenue mix shift from 54% subscription (the modern software income that it and investors covet) to 60%, the final figure coming in the quarter that wrapped up this June. So the switch to SaaS is working for Atlassian, even if it has pretty high goals to eventually meet.

Image Credits: Atlassian

“I think there’s a world eventually where [subscription revenues] could be 100%” of the company’s top line, Deatsch said. It will take time, however, with the executive adding that Atlassian has “lots of customers” sitting on older deals that will still need to shift over, but that the company believes these “long-term partnerships are going to have more cloud in them.”

Atlassian is super clear about where it’s moving to, which as far as public companies go, is somewhat refreshing.

Shifting priorities

By swapping old revenues for new, Atlassian is forging a path to the right side of the business-model divide. Its move to freemium suits the shift well, as it should provide an ample funnel from which the company can generate new subscription customers at little cost. (The company already has impressively low sales and marketing spend for a company of its size; Atlassian wants to keep that going when it is a pure SaaS play.) The present reality may be providing some tailwinds, as well. “The SaaS transition is only being accelerated through [COVID] and that’s providing a big opportunity for us,” Deatsch said.

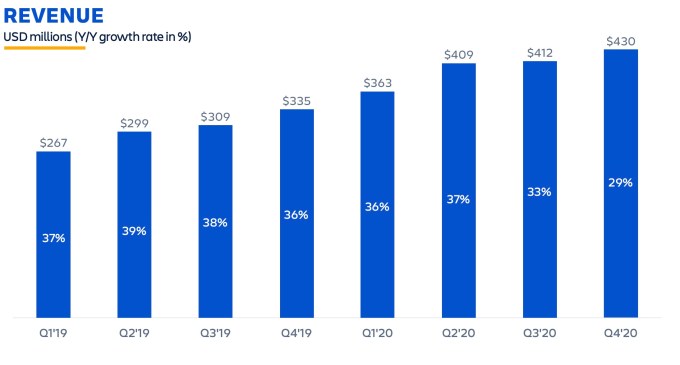

But in the short term, exchanging larger license revenue chunks for smaller recurring revenues can result in slower growth. Atlassian grew 36% in the first quarter of its fiscal 2020, but just 29% in its most recent quarter. It expects growth to slow even further to 18%-22.5% in the current quarter, the first of its fiscal 2021, according to its recent forecasts for investors.

Image Credits: Atlassian

This is the cost that companies pay when they move to SaaS. Atlassian, however, is being a bit more radical. It isn’t merely shifting stance over time, it’s trying to accelerate down the SaaS path. The company said that it will use “every tool available to spur migrations to the cloud over the next few years, including: large scale R&D investment, new product innovation, effective migration tools, partner migration services and generous cloud discounts for eligible migrating customers,” per its most recent shareholder letter.

That means that Atlassian will keep R&D spend high as it works to move customers to the cloud, even offering discounts to do so. The company said in the same letter that it will also “be sensitive to customers facing challenges due to COVID-19. [ … ] We will also continue supporting customers by providing extended terms and concessions to the subset most in need.” All of this combined could help account for the slower growth projections.

There are encouraging signs to point to as well from the company’s perspective. Deatsch said that “a big part of Atlassian’s drive right now is our cloud transition for our larger customers [ … ] and we’re seeing the only increasing demand for that due to [the company’s] products evolving and getting very strong” in the cloud setting.

What’s the end result in four or eight quarters’ time? Better-than-previously-possible revenue growth consistency, with a revenue mix more tilted toward high-margin, recurring SaaS dollars. That’s investor catnip, and during a more normal time would be the easy move, but to do so during the recession and pandemic shows the company’s self-confidence. And not misplaced confidence, we’d reckon.

Aggressive acquisition approach

Even as they implement the long-game strategy to build up SaaS revenue, Atlassian has the means to make purchases — and it’s not afraid to do so. In fact, the company has made more than a dozen acquisitions over the years, including mainstays BitBucket and Trello. The company swung and missed on HipChat when Slack ran away with the market, but overall it has done well.

This year the company has already made a couple of purchases. In a case of “if you can’t beat ’em, join ’em,” it grabbed Halp for help desk integration directly in Slack. The company also acquired Mindville, a tool that helps IT manage physical assets using Atlassian’s Jira tool.

Deatsch says that these purchases fit in with the company’s product-driven acquisition strategy. “We’ve always been a product-driven organization so all of our M&A comes around with a product strategy,” he explained.

He doesn’t think that the current market is necessarily more conducive to buying early stage companies, simply because they play in collaboration, and that area has remained fairly hot through the pandemic. The key point is that Atlassian has plenty of cash, and if it sees an opportunity to build upon the overall company vision with an acquisition, it’s going to grab it.

While Atlassian’s shorter-term growth projections are going down, the company benefits from sound financial health with plenty of cash, while playing in several huge addressable markets. They know there could be some economic factors ahead that are outside of the company control, but Deatsch isn’t concerned.

“In a world where the macroeconomic situation could be a little bit rough we’ll continue to invest in our business by hiring ahead of things, and of course M&A is a key piece of what we do. We’re a multiproduct company and we have a long track record of successful M&A,” he said.