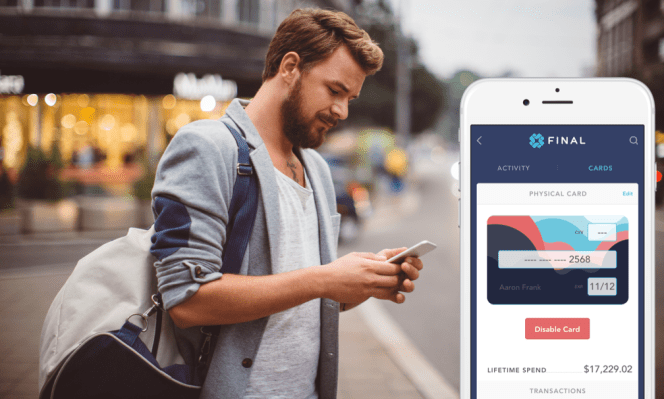

A startup called Final wants to change the way people use credit cards — or rather, the company wants to change the credit card industry to fit consumers’ lifestyles. With a 1 percent cash-back bonus and no annual fee, Final offers a competitive credit card product, but it really excels in the flexibility it provides in the way consumers can manage virtual cards across multiple vendors.

If you’re like most of the people who read this site, you probably have a Spotify account and a Netflix account, and maybe you subscribe to one or more online video services. You probably have a card on file at Amazon.com and shop a variety of different e-commerce sites. Who knows, maybe you pay monthly for some sort of subscription box that used to be all the rage a few years ago.

Increasingly more of your purchases are moving online, and you probably pay for all of those goods services with the same credit card.

And what happens if that credit card is ever lost or stolen? Well, you’ll need to get a new one, but that’s only the beginning of the hassle that comes with a compromised account. You’ll also need to update your card information with all the subscription service, e-commerce sites and online vendors that you happen to use.

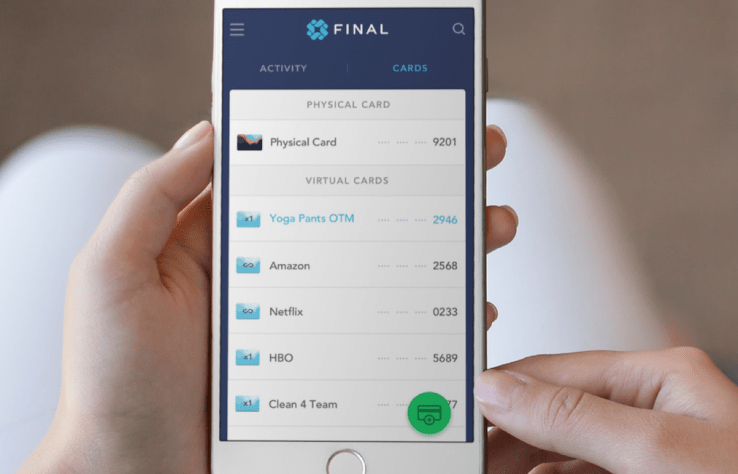

But what if I told you there was a way to have a different card number on file for each individual service? And what if I told you that each of those different card numbers would be aggregated into one single payment that you make monthly?

That’s the beauty of what Final is doing: It allows its credit card customers to create an unlimited number of virtual cards that they can specify to use with various different online services. And if one of those cards is ever compromised, or even if they want to just cancel or stop paying for a service, all they need to do is delete the virtual card.

That’s the beauty of what Final is doing: It allows its credit card customers to create an unlimited number of virtual cards that they can specify to use with various different online services. And if one of those cards is ever compromised, or even if they want to just cancel or stop paying for a service, all they need to do is delete the virtual card.

Final customers still get a single physical card in the mail, but they may never use it. And that will be the last piece of mail they’ll receive from the company. All other correspondence, including statements, happens online — and in the case of a problem, Final is eschewing complicated phone support trees and moving to email-first support.

In other words, Final is trying to build a credit card product for how consumers would like to interact with their accounts today. They want to be paperless, they want flexibility in managing their accounts, and they want more control over the ability to sign up for and cancel subscription services.

Also, consumers want instant approval upon application, something that Final can deliver on. It can approve and activate customers immediately, meaning they can begin creating virtual cards and using the service before a physical card is ever even mailed to them.

To do all that, the Final team spent more than two years building up its tech stack from scratch, which enables it to issue a near-infinite number of virtual cards. With that technology in place, the company is coming to market with a consumer-facing product, looking to take a small piece of the $6 trillion consumer credit card market. But Final could also serve enterprise customers that want a turnkey solution for issuing and managing credit cards.

Final has raised $4 million from investors that include 1776, Canyon Creek Capital, DRW Venture Capital, Kima Ventures, KPCB Edge, Ludlow Ventures, Michael Liou, Right Side Capital Management, T5 Capital, Wei Guo, Y Combinator and Zillionize Angel.