Value creation in enterprise tech is often driven by a cohort of exits, while value creation in consumer tech is generally driven by large, individual exits — a phenomenon I recently dug into. What the data revealed is that, in recent years, there is a trend of larger consumer exits, such as Facebook, Twitter and WhatsApp. And if this trend continues, that’s very good news for consumer-oriented funds.

But the data further begs a deeper dive on VC-backed exit dynamics; in particular, what are typical VC-backed exit sizes?, including a look at the frequency of exits greater than $1 billion across enterprise and consumer.

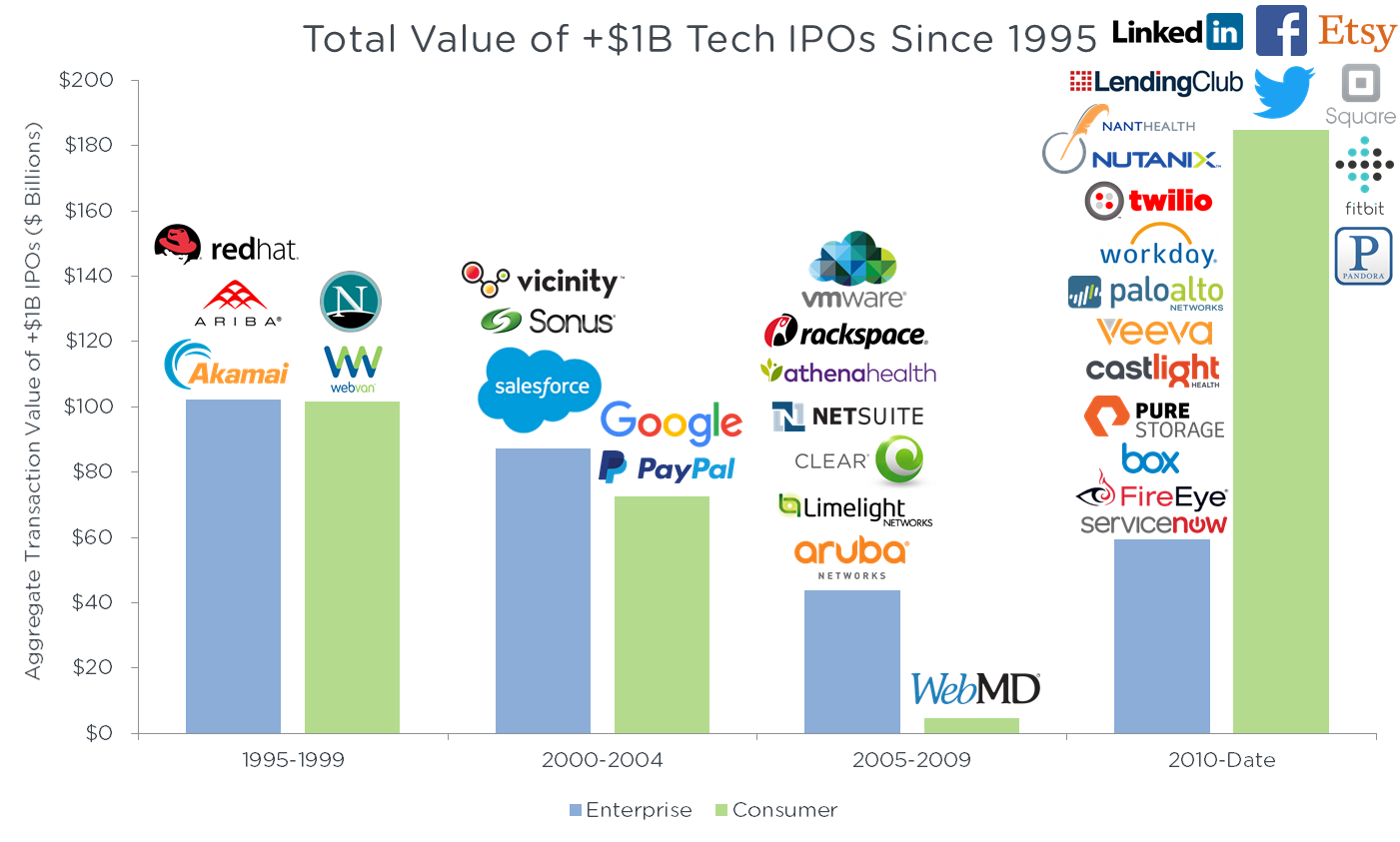

For companies with IPO exits of $1 billion or more in valuation, venture-backed enterprise exits outpaced consumer exits until recently. There were 144 IPO exits with greater than $1 billion in value, of which 97 are enterprise companies and 47 are consumer companies.

Source: Sapphire Ventures

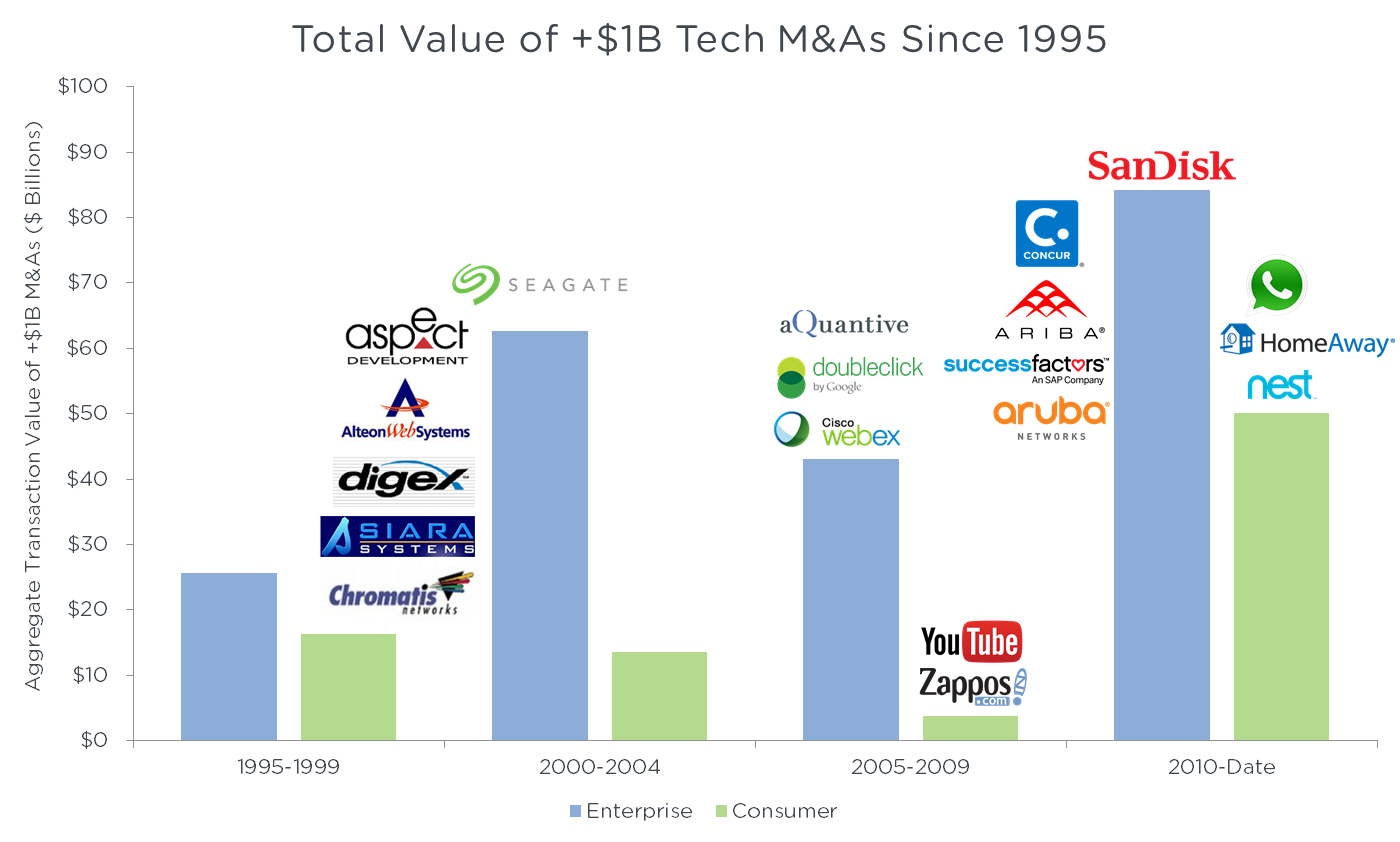

On the M&A front, there were 96 exits of $1 billion or more in value, of which 65 are enterprise companies and 31 are consumer companies. Similar to the chart above, acquisition value of enterprise companies outpaced that of consumer companies until recently, when the venture capital ecosystem became more accommodating of large M&A transactions, potentially driven by the run up in market capitalization of some of the earlier, successful IPOs of companies such as Google and Facebook.

Source: Sapphire Ventures

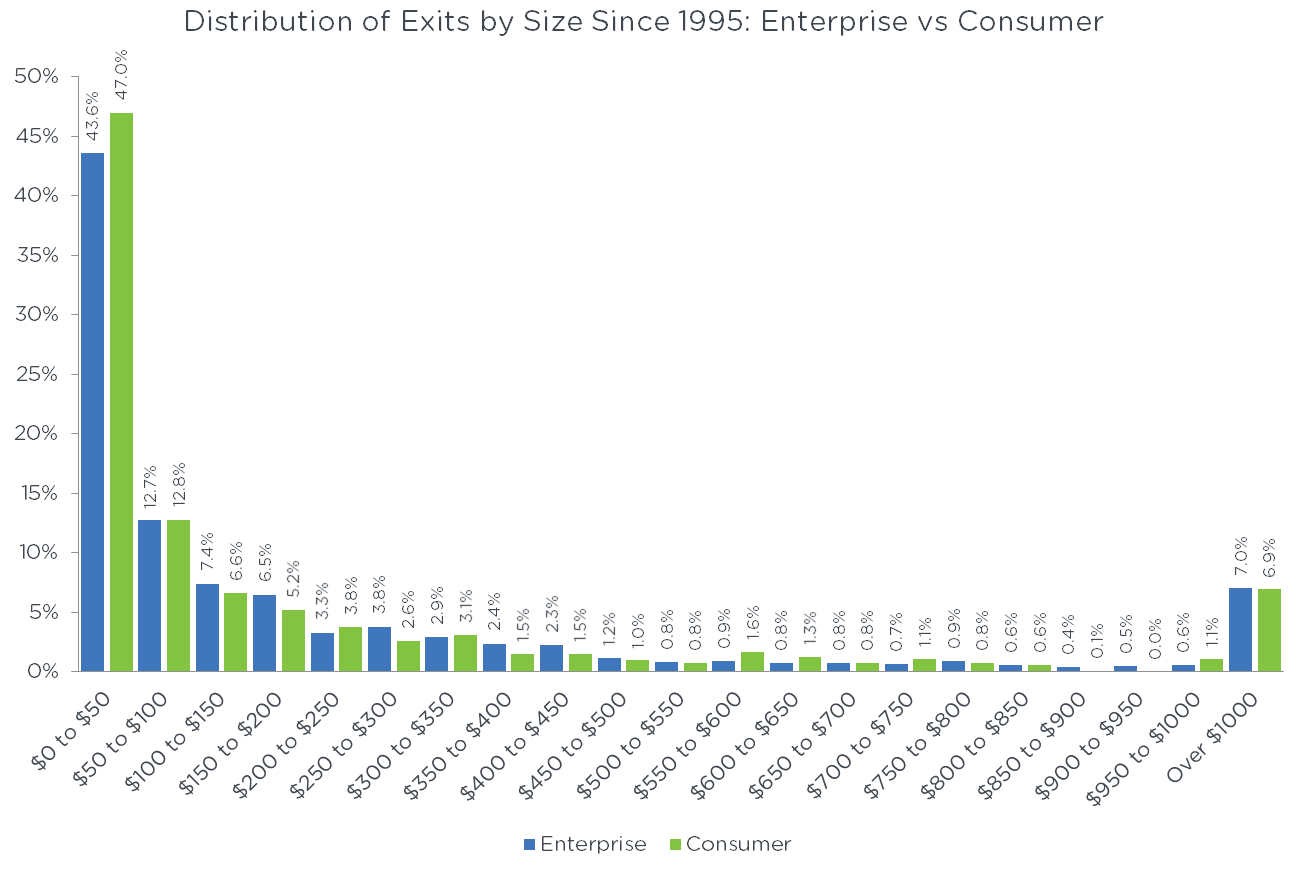

Of course, looking only at outcomes with $1 billion or more in value only covers a fraction of where most VC exits occur. Slightly less than half of all exits in both enterprise and consumer are $50 million or less in size, and more than 70 percent of all exits are less than $200 million.*

Source: Sapphire Ventures

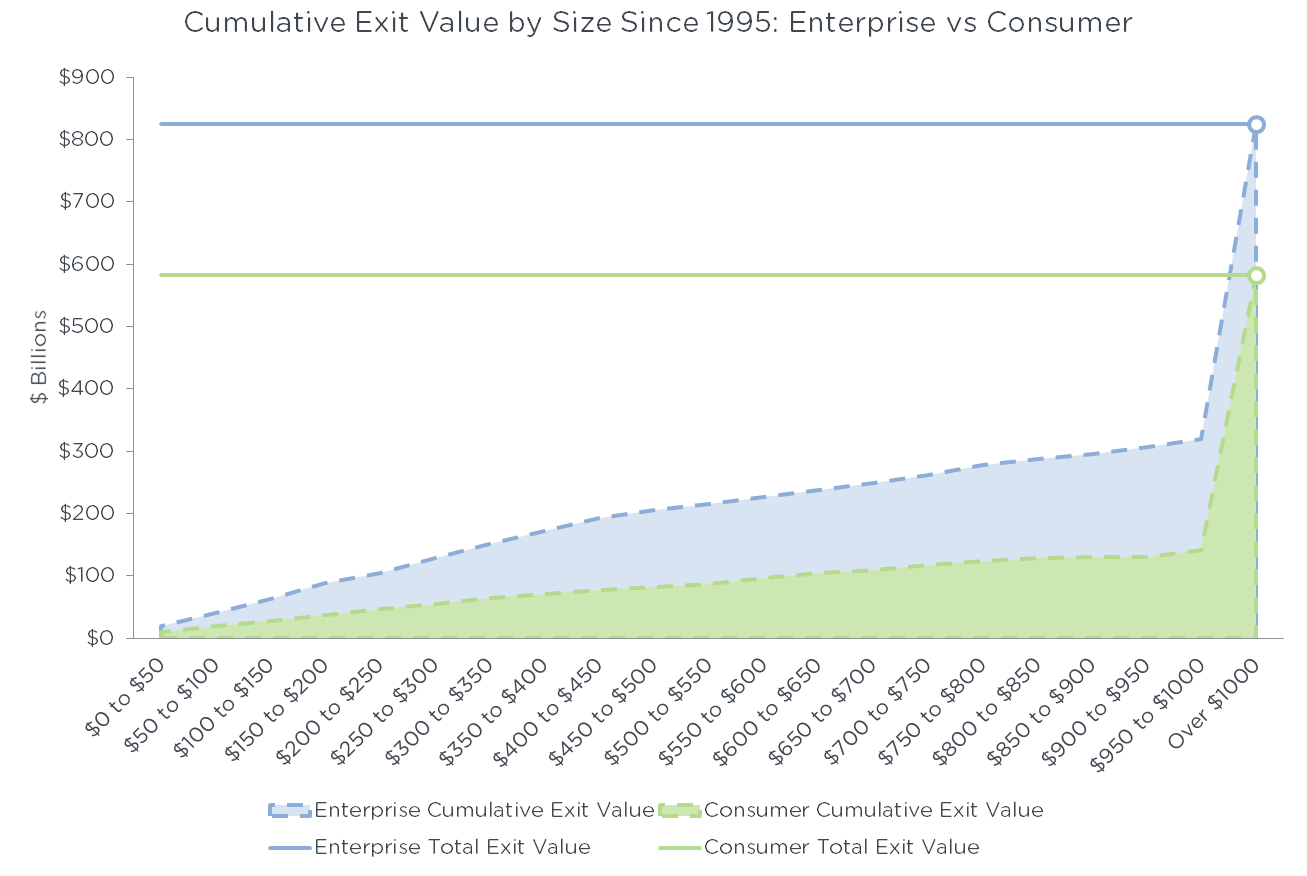

Additionally, it’s interesting to consider cumulative value accretion across exit sizes for both enterprise and consumer (see chart below). The power law of venture outcomes is apparent in both enterprise and consumer, whereby a significant portion of total exit value is generated by the $1 billion-plus outcomes. In particular, exits greater than $1 billion generate 62 percent of total returns for enterprise and 77 percent for consumer.

Source: Sapphire Ventures

So, consistent with my previous conclusion about enterprise funds returning more capital than consumer ones, it furthermore turns out that the enterprise category has generated a larger cohort of successful outcomes, while outlier companies make up the vast majority of returns in the consumer category.

Now we have to wonder about capital invested into each category and how investment cost per annum correlates with exit value. A future article will look into this question — and more.

*The distribution chart only captures the percentage of companies for which we have exit values. If we change the denominator to all exits captured in our database, i.e. measure with a higher denominator, the percentage of outcomes with $1 billion or more in value drops to around 3 percent of all outcomes for both enterprise and consumer.

Disclosure

The information set forth herein is not intended to constitute investment advice and under no circumstances should any information provided herein be used or considered as an offer to sell or a solicitation of an offer to buy an interest in any investment fund managed by Sapphire Ventures. Sapphire Ventures does not solicit or make its services available to the public and none of the funds are currently open to new investors. Past performance is not indicative of future performance.

Any portfolio companies referred to above do not necessarily represent all of the investments made or recommended by Sapphire Ventures, and were not selected based on the return on Sapphire Ventures’ investment in them. It should not be assumed that any specific investments identified and discussed herein were or will be profitable. Not all investments made by Sapphire Ventures will be profitable or will equal the performance of any of the companies identified above.