If you believe in the mantra “innovate or die,” you might conclude that the largest consumer and retail brands are terminally ill. Giants like Kraft and Clorox all seem to be too slow and enslaved to shareholders to innovate. At the same time, they may be too large to perish… at least for now.

What we have here is the perfect storm for a consumer mergers and acquisitions (M&A) avalanche.

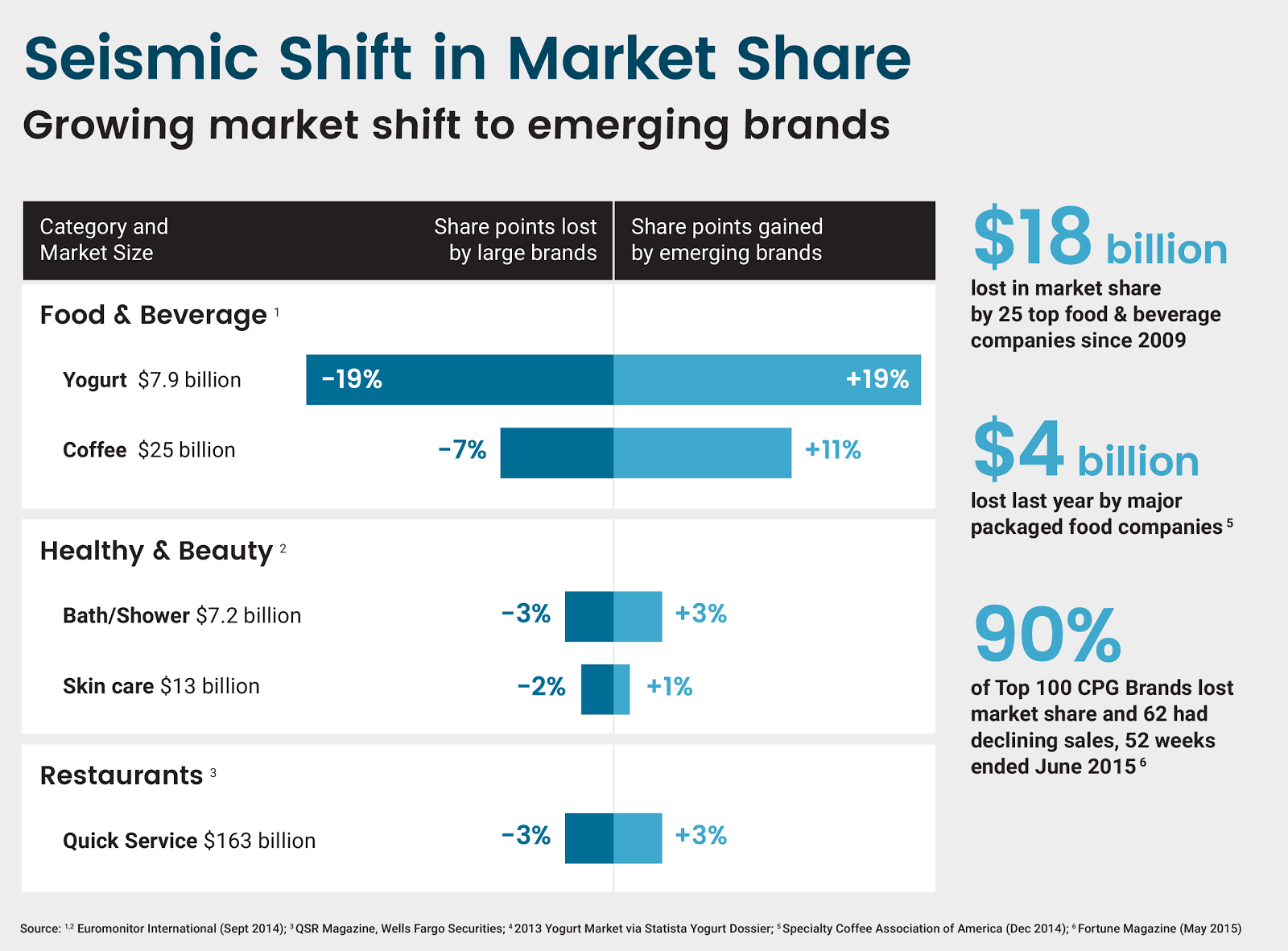

Big consumer packaged goods (CPG) companies are struggling to sell their products to a new generation of shoppers. A quick look at sales across various product sectors shows a steady downward slide for big brands. In the past five years, large brands lost market share to small brands in 42 of the top 54 most relevant food categories, according to Jefferies. Erosion is happening in nearly every consumer category.

As consumers increasingly crave unique, authentic brands that meet personal preferences, marketing and distribution costs are falling dramatically. Consumers are researching and seeking out products rather than responding to advertising.

Source: CircleUp

Major CPG companies are losing billions in market share. And they aren’t doing much about it. When was the last time a large consumer brand introduced an innovative product that anybody noticed? Research and development (R&D) should be more important — but is less emphasized — than ever.

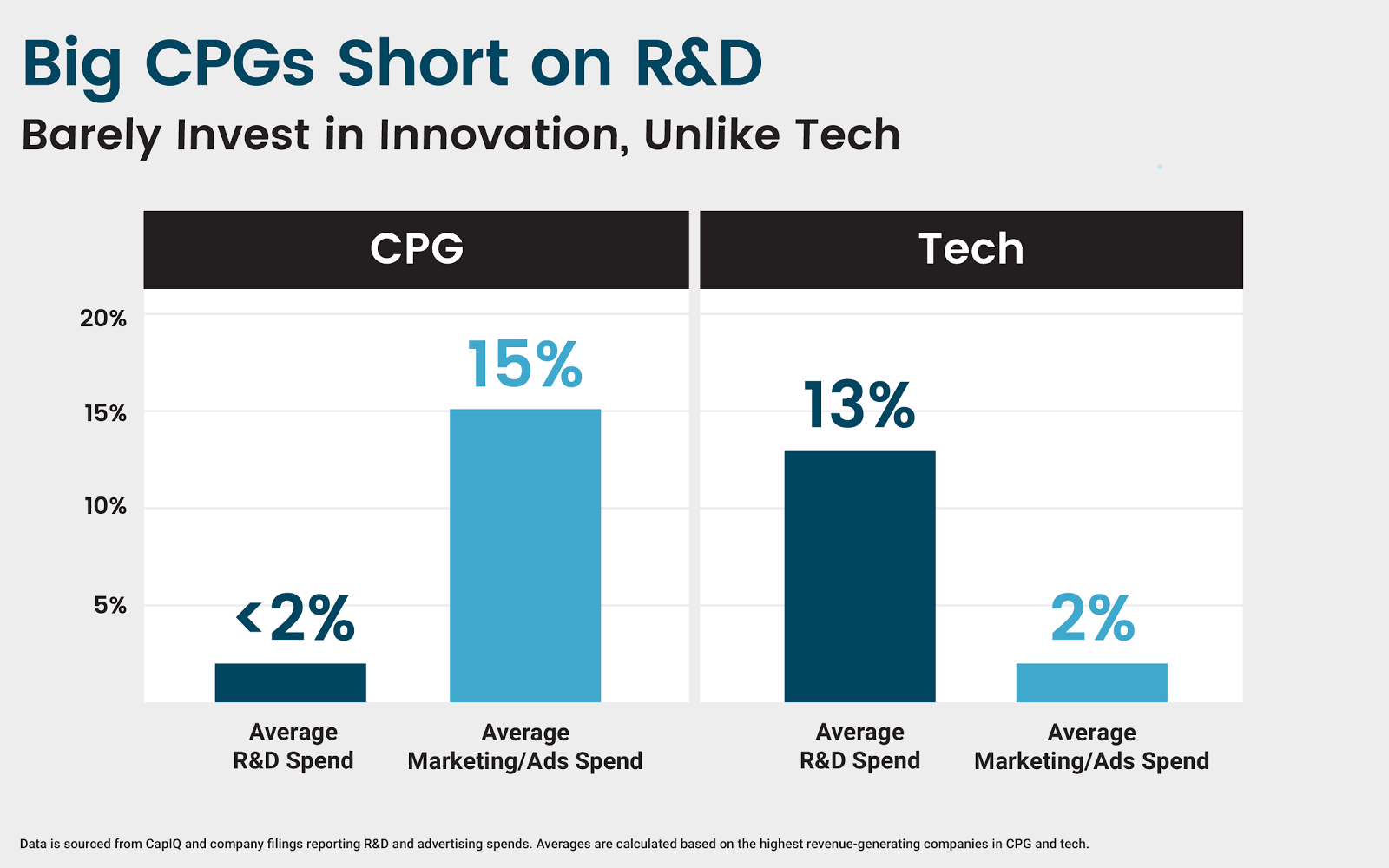

How bad is the R&D problem at CPG companies?

At CircleUp, we recently pulled some data illustrating just how bad the R&D problem has become. We found that, on average, the biggest consumer packaged goods companies spend less than 2 percent of revenue on R&D, and close to 15 percent on marketing and advertising. In technology, where innovation is front and center, the spending is nearly reversed: about 13 percent on R&D and 2 percent on marketing and advertising.

Source: CircleUp

Big brands aren’t oblivious to the challenges they’re facing. So why aren’t they investing more in new product development?

Big brands haven’t needed to innovate

For decades, large brands have been protected by the high cost of entry into the CPG market. The pre-social media, pre-Amazon era made it extremely expensive for small companies to get distribution and advertise their products. Demand for innovation was extremely low because consumers were so accustomed to seeing the same products on the shelf.

Innovation is risky

The path to innovation — developing and testing new products and weighing market responses — is flat-out risky. It could lead to quarterly and yearly losses and the future revenue takes years to kick in (if it does at all). Brand managers responsible for R&D decisions often have short-term incentives to not take risks. Should we meet our quarterly numbers or should we innovate on a new product that likely won’t show top-line impact until years after I’m transferred to run another division?

Big brands don’t have the personnel to change

There have been so few incentives to change for so many years that most big brands don’t have robust R&D teams or experience. These behemoths just aren’t well-equipped to test the water and make great new products.

These companies are decades old, sometimes a century, and they aren’t used to change. The image of your grandfather on the dance floor comes to mind. As does Clay Christensen’s “The Innovator’s Dilemma,” which calls out this trend. Big brands spend so much effort selling their existing products that they fail to plan for the future, then struggle shifting to solve for a problem they weren’t born into.

Source: CircleUp

M&A is replacing R&D

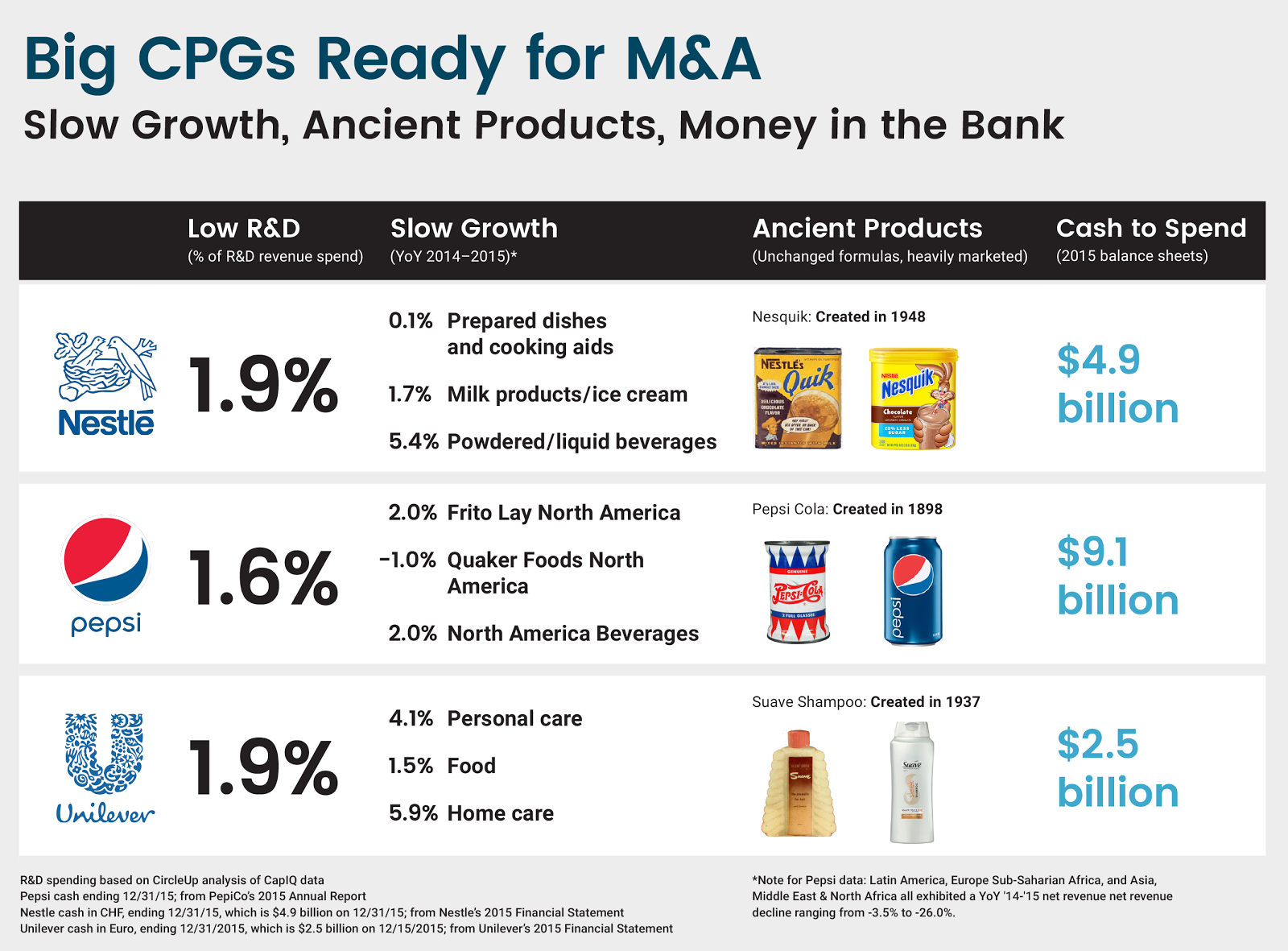

Mergers and acquisitions are, effectively, big consumer brands’ substitute for R&D. And with drastically shrinking market share, slow growth and big cash war chests on their balance sheets, we’ll be sure to see a lot more of it. And a lot more early-stage investing, as well, so they can participate in more of the growth, earlier in a brand’s life.

Unilever spent a mere 1.9 percent on its R&D last year, but it hasn’t been shy about hedging bets elsewhere, snatching up Dollar Shave Club ($1 billion) and Seventh Generation ($700 million). Unable to outflank startup brands, big consumer brands are upping their M&A games as a way to outsource R&D and leave the risk of innovation to the startups that do it best.

This trend has already taken hold in the pharmaceutical industry. The conglomerates there skip R&D almost entirely, acquire new formulas like crazy, then plug those products into their vast distribution pipes while they focus on advertising and regulatory issues. Big consumer brands are on the same path.

But the deciding factor, and what we’ve yet to see, is how well these big brands preserve the quality and authenticity of their newly acquired products. People increasingly demand personalized offerings, be it organic, environmentally sustainable, fair-trade, of an ethnic variety — the list goes on. Now, the seemingly simple act of selecting a household cleaning solution is an act of self-expression. If big brands don’t preserve the uniqueness, they’ll be back where they started.

The forces behind an M&A avalanche have been building for several years. Last year alone the M&A in consumer and retail was $238 billion, almost twice the size of M&A in tech. The M&A avalanche signals are there, and they’re only growing stronger. Get ready for the ride.