People often ask me how I went from building multiple companies in ad tech, music tech, data analytics and mobile advertising to being a lending fund manager. It didn’t happen overnight. In fact, it was almost a decade in the making. Here’s my story, and why I fell in love with P2P lending as an investment.

Some call it P2P lending, but as more institutions such as hedge funds get in on the action, we’ve grown to call it marketplace lending. The biggest and oldest segment within P2P lending is consumer loans. As a result, I’m strictly talking about the consumer loans category as I present the ensuing comparisons and facts.

P2P consumer loans have been around for some time now, meaning there is substantial historical data to analyze. It started in 2005, when Zopa launched a P2P lending platform in the U.K. The following year, Prosper launched in the U.S., with Lending Club following about a year later. Recognizing the potential of this new asset class, I started to lend on Prosper almost the moment it opened. It was simply too exciting for me not to try.

What really sold me on the viability of this space, though, is that my 2006 and 2007 vintages of 3-year loans went through the Financial Crisis period of 2008-2010 (or whatever you want to call it). The S&P 500 was down 55 percent, U.S. consumers were hurting and I was sure that I was going to see a negative return. Yet when the books closed in 2010, my loan portfolio was positive! (For you mathematicians out there, yes, I had many loans to make it a statistically relevant conclusion.)

Banks have maintained a profitable lending spread for the past 30 consecutive years!

Shocking, right? Coming from a non-finance background, it certainly was to me at the time. Then I realized that I came across one of the best-kept secrets in investing at the time: “Prime” consumer default rates historically do not outpace the interest rates.

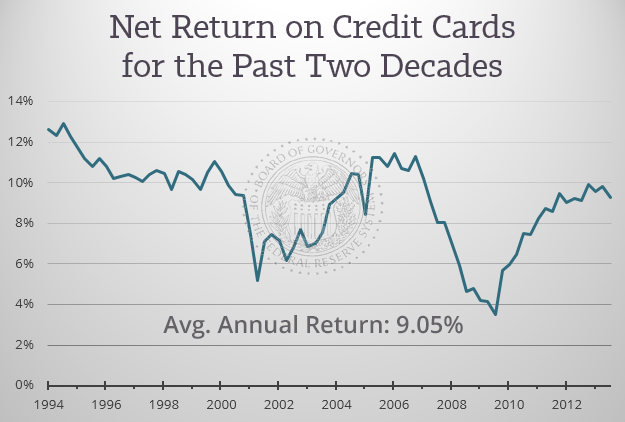

Why is that? There is a substantially similar asset class: credit cards! Just like P2P consumer loans, credit card debt is unsecured consumer debt, and it’s largely available to the same “prime borrowers” (people with good credit). Take a look below at how credit cards performed for the past 20 years.

Source: United States Federal Reserve

The biggest takeaway here? Not a single negative year. In fact, Federal Reserve data shows that banks have maintained a profitable lending spread for the past 30 consecutive years!

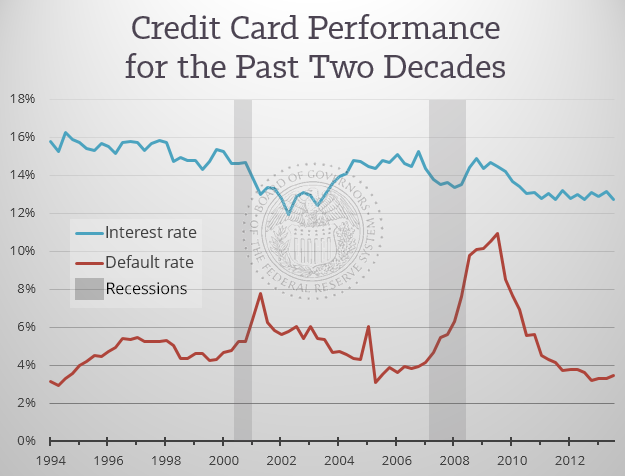

The chart below further breaks down and separates the gross interest rate from the default rate. Even at the height of the Financial Crisis, the default rate momentarily peaked at 11 percent for a single quarter, but there was 15 percent of gross interest to cover those losses, leaving credit card companies with a 4 percent spread. Not too shabby when the sky is falling.

Source: United States Federal Reserve

So after experiencing this, it was clear to me that if the P2P lending industry survived this perfect storm during its infancy, it would be the place to invest. It was thus at that point that I decided to invest BIG.

Once I made that decision, it was time to figure out how to execute on it. Because I was comfortable with Prosper, I called them first. As it turns out, investing a really large amount directly with a P2P platform is not quick or easy. First, they recommended I research professional fund managers. That led to my meeting Don Davis of Prime Meridian, which was an early adopter in the space. His team understood lending dynamics in this new world. I was very happy to hear of a fund to do this, for several reasons:

- Liquidity. While loans provide a great source of monthly cash flow, there is still not a good way to “sell” them if you need the cash immediately. With a fund, I would have access to far more liquidity because a fund has much greater cash flow.

- Time. I was too busy running my company at the time, and the idea of having someone handle my P2P lending was very attractive.

- Advanced Strategies. A fund manager does this all day, every day. Thus, the level of sophistication employed by a full-time manager would simply outperform my ability to manage this as a side project.

- Reduced Cash Drag. Putting a big chunk of capital to work in a marketplace takes time. That means the cash sits around earning 0 percent while you’re putting it to work. A well-run fund is geared to put that money to work very fast.

- Diversification Benefits. Investing into a seasoned, mature and well-managed loan fund provides instant diversification and can further reduce risk.

After lots of due diligence, I opted for the fund route.

Over the next couple of years, many people asked me about the best way to get into P2P lending. If you’re a retail investor with as little as $2,500 or as much as $250,000, I’d strongly suggest that you open a Prosper or Lending Club account. Diversify your investment across as many loans as possible and as evenly as possible, with a goal of having at least 400 loans (remember, you can lend as little as $25 per loan).

With a growing number of individuals and institutions looking to invest more than $500K in marketplace loans, a number of options have arisen. Those include paper, from the likes of Citi or Blackrock, that typically pay about 3-5 percent; unlevered funds, such as NSR or Prime Meridian Income Fund, that typically generate 6-9 percent; or a levered fund, such as Eaglewood, targeting 11 percent or more.

So there you have it, my (almost) 10-year history with P2P lending — and why I think it is a great asset class that has yet to be found by the masses.