Editor’s note: Brandon Lipman is a startup and venture capital enthusiast and past co-founder of 3D printing company 3DLT.

Over the last few months the question has been asked by almost everyone in the startup and venture capital community: Are we in a tech bubble? I don’t think there’s even a question anymore.

Many founders are in deep denial valuing their pre-revenue SaaS Uber for CRM cloud based big data machine learning platform for millions of dollars pre-money. When a potential investor asks the founder why they are valuing their startup at such a high valuation, they just don’t know or they say, “we need to look like a unicorn so we hire the best.” This story has been told by venture capitalists across the Valley.

Bubbles are like forest fires

You can think of a bubble like a forest fire. Yes, it’s tragic that trees existing for hundreds of years die and animals are displaced. The flames come through and burn down the weak underbrush.

The aftermath looks terrible and hot spots will continue to flare up way after the flames subside. However, just as forest fires are necessary for ecological health, bubbles are necessary for industry health and growth. Forest fires make way for new trees that can grow stronger fueled by the ashes of their predecessors.

Some venture capitalists will get burned and lessons will be learned similar to those who invested heavily in the dot com bubble. In fact, many of the investors that were active during the 2000 bubble are the ones that keep warning all of us of a potential bubble.

Mattermark published a report with data comparing the quarter-one midpoint of 2014 to 2015. Mattermark’s data comes from CrunchBase, AngelList, regulatory filings, thousands of news sources and company reported data. I would highly suggest that you download the entire report from Mattermark. The graphs below were reproduced with permission from Mattermark.

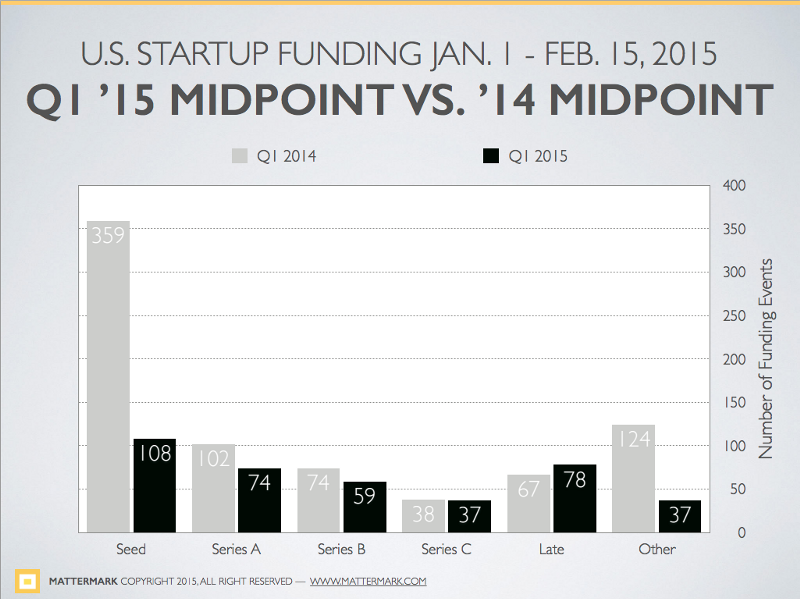

The graph above shows the number of funding events comparing the quarter-one midpoint of 2015 to the quarter-one midpoint of 2014 .

The most noticeable item is the drastic slowdown in seed deals decreasing by nearly 300 percent. This could indicate a shift in venture capital strategy focusing on funding fewer companies and putting more time into the companies they invest in.

Does this indicate a venture funding bubble? Potentially. To founders looking to raise capital, it may seem like a bubble as it is statistically more difficult to raise a seed round of funding now compared to a year ago.

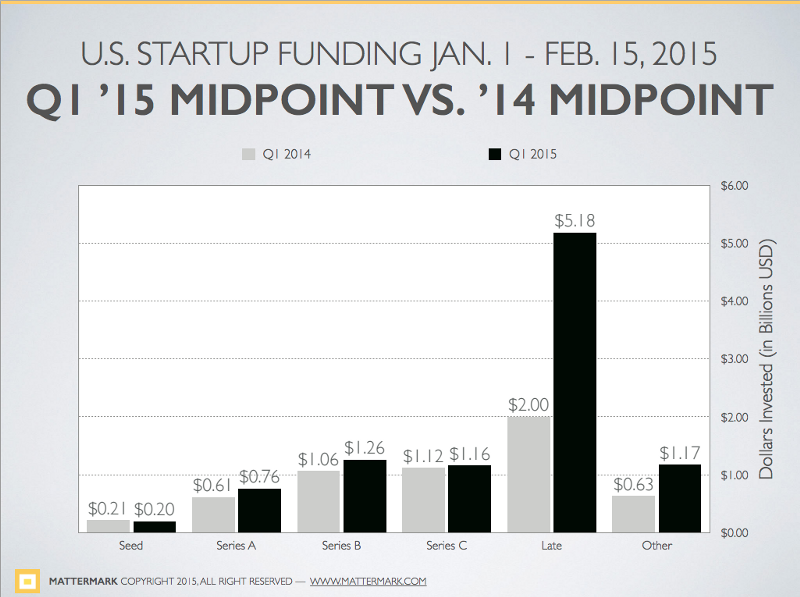

Total dollar analysis

The graph above looks at the total dollar amount of funding per stage comparing quarter-one midpoints of 2014 and 2015.

From what we noticed above, the volume of seed deals has drastically decreased. Interestingly, the amount of total dollars being invested at the seed stage has remained roughly the same. According to this data, we could infer that the amount of money going into seed-stage startups is going up.

This simple analysis comparing total dollars invested allows us to conclude the following:

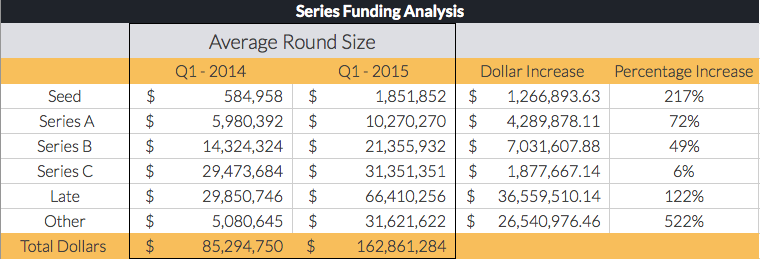

The average round size is calculated by taking the total dollars of deals in a stage at a specific quarter midpoint and dividing it by the volume of deals done in that stage of the same quarter midpoint.

For seed rounds, the average dollar amount per deal in Q1–2014 was $584,958 now it is $1,851,852, a 217 percent increase. This is the only stage of funding that is seeing that large of an increase in funding. All other stages of funding are increasing but by far less than seed rounds. Series C funding is the most stable, only increasing by 6 percent.

This also supports the theory that seed rounds are starting to look a lot like the typical series A rounds.

Another explanation of this could be if burn rates are increasing. If this is in fact true, this strongly points to a bubble as startups are becoming more capital intensive. This would also explain why the average size of seed rounds is increasing while the number of deals is dropping.

If burn rates continue to rise, startups will be forced to actively look for their next round of funding earlier than they had initially planned. This will surely lead to more startups raising a down-round (a round of funding raised at a lower valuation than in a previous round) or not being able to raise at all — many of whom will sadly die.

What’s exciting about a bubble?

The founders who are in it for the wrong reasons will go running back to their old bosses begging for their stable jobs back. Now is the perfect time for the true founders to buckle down and improve. Capital will be scarce but the best founders will use this time to rebuild and become better founders.

Valuations will start to seem inline again and San Francisco housing cost will resemble some signs of normalcy. Recruiters will slow down on their poaching of junior level engineers in coffee shops.

The venture capital and founder community will become closer. Oh, how I look forward to the bubble bursting. If you’re not seeing it yet, try looking at the many positives that a downturn could potentially bring.

I am currently reading Antifragile. The premise of the book is looking at potential gains in times of disorder, and it’s a terrific read for those involved in startups and investing. Navigating fundamental shifts in technology and outer market forces are key characteristics of great founders.

I look at the funding landscape and see a terrific environment for learning. Bubble or not there are certain things that remain true. Great founders create amazing companies and great founders will always find a way to succeed.