Y Combinator-incubated payday loan disruptier LendUp has raised $14 million in new funding from Google Ventures, QED (a firm that includes the founder of Capital One and Data Collective. This brings the company’s total funding to over $18 million.

LendUp is attempting to redefine the payday lending, and make loan experience for the millions of unbanked Americans more fair and transparent. Rather than force Americans to turn to predatory lenders and banks, with their high interest rates, LendUp wants to give those looking for a speedy fix to a short-term financial need a way to borrow money without hidden fees, costly rollovers and high-interest rates.

At a basic level, LendUp is direct lender and has created a way to use small-dollar loans as an opportunity for consumers to build credit and move up the financial ladder. Consumers who have poor or no credit can apply for and receive small-dollar, short-term loans (up to $250 for up to 30 days). But it doesn’t stop there. The company’s uses these small-dollar loans as a way to help customers build credit and move up the financial ladder.

Unfortunately, most credit agencies turn their backs on payday loans, so even if people are able to pay them on time, it doesn’t help their credit scores and the cycle of bad credit keeps on spinning. Most banks won’t touch these kind of loans because they’re high-risk, but like On Deck Capital (which is attempting to streamline the lending process for small businesses), LendUp uses Big Data to do instant risk analysis and evaluate creditworthiness, weeding out those who have bad credit for a reason from those who may have become victims of the system.

In fact, LendUp is now working with all the major credit bureaus to report customer data so they can build their credit.

Rather than make everyone submit bank statements, credit reports and so on right from the beginning, LendUp will use other available data and approves those with good credit instantly. It only requests more information from you if questions arise, approving or rejecting as soon as it has enough information to make an informed decision.

Earlier this year, LendUp began offering instant online loans. This means that LendUp now has the ability to deposit money in your account in as little as 15 minutes, so that consumers not only can apply for and get approved quicker than they normally would, but they now have near-instant access to that loan. LendUp loans are also available on mobile, and LendUp deposits that money into your bank account, which you can then access from your laptop or while you’re on-the-go.

Co-founder Sasha Orloff tells me that LendUp has been strategic on focusing on one state (California), and ensuring that its platform is in compliance as a lender with the state’s rules. He compares this efforts to literally recreating a different lending application for each state, considering each region’s laws and regulations. The startup recently started lending in Louisiana, and Missouri but with the new funding, LendUp plans to expand nationwide.

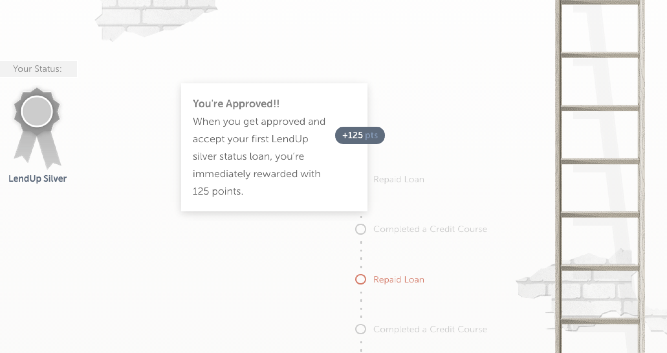

With the startup’s new financial ladder educational system, LendUp is trying to get users to improve their creditworthiness by completing online courses in credit, saving and more. As you pay back your loans on time, take the course, you earn points to elevate your up the ladder to silver, gold, and higher statuses. As you attain high statuses, you are able to access more money for loans at lower interest rates. In fact, Shane Berry and Christopher Walsh from LendUp’s UX team, worked with a design team from Zynga (where co-founder Rosenberg used to work) to help create this game-like experience, and help educate users that earning this financial credit can be fun.

Orloff also comments that LendUp currently has debt commitments for another $25 million of debt for the startup’s loan portfolio.

The online lending space at large has begun to look a little more crowded as companies like LendUp, BillFloat, Zest, Think Finance, Kabbage, On Deck and Lending Club all try to make it easier for consumers and small businesses to get access to capital without having to jump through a million hoops.

But what makes LendUp distinct is its efforts to actually help many of these unbanked Americans who can’t find a loan, become credit-worthy through education. The startup is trying to solve the root of the problem, which is poor financial education.