The crypto sell-off of the last several days was preceded by staffing cuts at several companies in the business of facilitating the trading of decentralized assets and tokens. Reductions at Gemini and Crypto.com were superseded today by news that Coinbase is cutting more than 1,000 staff. Given that Coinbase and other crypto exchanges were high-flying success stories of 2021, the retreat may feel surprising.

How could companies like Coinbase, which reported massive growth and huge profits last year, now be in a position where they would need to slash staffing? This isn’t to overly focus our attention on exchanges; other companies in the larger web3 space are also under fire, including BlockFi, which also recently cut staff.

The answer to the sharp swap from rapid staffing to personnel cuts at exchanges, however, is something that we can actually understand with reasonable clarity. It boils down to this: Costs scaled at crypto exchanges as their revenues grew. Now, as their top lines contract due to falling trading volumes, those previously warranted costs have morphed into a burden.

Leaning on May data from consumer trading service Robinhood, Coinbase performance data and public layoff notices from crypto exchanges, let’s explore how things got so upside-down so quickly.

Booming revenues, costs

Coinbase had a simply excellent 2021. Its net revenues grew from $1.14 billion in 2020 to $7.36 billion last year, with its net income rising from $322 million to $3.62 billion over the same time frame. Growth and profitability like that impressed investors and potential employees alike, with both groups flocking to the company.

In its final earnings report of 2021, Coinbase indicated it had invested heavily to keep the revenue expansion coming, citing both hiring and its cash position as potential growth levers:

Image Credits: Coinbase Q4 2021 earnings report

Our read of the above is that at the time, Coinbase felt wealthy and well staffed, giving it a liquid and human capital advantage over competitors. Coinbase stated in mid-February that it intended to “add up to 2,000 employees across our Product, Engineering and Design teams” this year.

By the end of Q1 2022, however, the company’s tone changed. Here’s Coinbase at the top of its shareholder letter released in late February:

The first quarter of 2022 continued a trend of both lower crypto asset prices and volatility that began in late 2021. These market conditions directly impacted our Q1 results. But, we entered these market conditions with foresight and preparation, and remain as excited as ever about the future of crypto.

In the first quarter, Coinbase’s revenues fell on both a year-on-year and quarter-on-quarter basis. It also saw a net income inversion, falling from year-ago and Q4 2021 net incomes to a net loss. Coinbase was clear at the time, however, that it was not ready to slow down:

We believe these market conditions are not permanent and we remain focused on the long term. In fact, our investment in our business now is especially critical — these periods of low volatility can provide the opportunity to focus more intently on product development (as opposed to peak periods, when we are more focused on meeting high demand). We approach the opportunities ahead with confidence and steady hands.

To that end, we have made good progress year to date, highlighted by the beta launch of Coinbase NFT, growth in adoption of Coinbase Wallet, expansion of our staking offering through the addition of Cardano and hiring over 1,200 full-time employees to help us build the future of crypto.

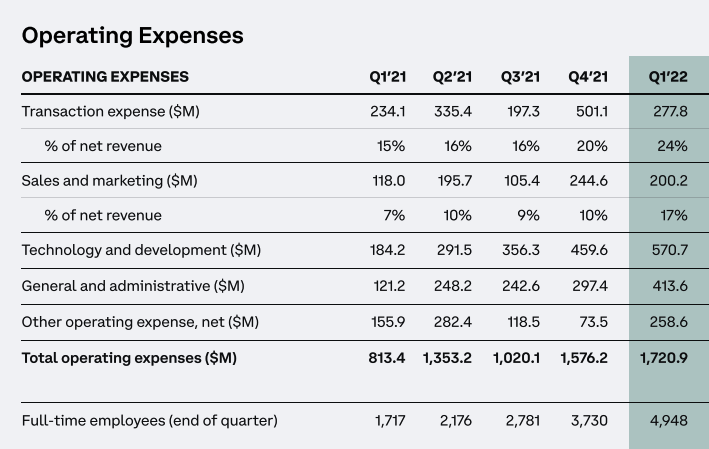

Again note the tying of staffing to attacking the future. All that hiring was not cheap. As we can see from the following expense breakdown from Coinbase’s Q1 2022 investor letter:

Image Credits: Coinbase’s Q1 2022 investor letter

As Coinbase’s staff size grew, so too did its expenses. Its “technology and development” and “general and administrative” line items swelled, putting Coinbase at a far-greater rate of operating spend than in its year-ago Q1. And it had to pay for those costs against smaller revenues than in that year-ago quarter, leading to a $430 million net loss.

By the end of March, then, it was clear that Coinbase was running deeply in the red. But it still took a little while for the situation in crypto to show up in the company’s plans. On May 16, Coinbase shared that it was “slowing hiring so we can can reprioritize our hiring needs against our highest-priority business goals.” Then, on June 2, it put an even sharper damper on cost growth, sharing that it was extending its “hiring pause for both new and backfill roles for the foreseeable future and rescind[ing] a number of accepted offers.”

That news made headlines, but the worst was yet to come. This week, Coinbase announced cuts of more than 1,000 staffers, with its CEO saying that the personnel reductions will help “ensure [that Coinbase can] stay healthy during this economic downturn,” adding that Coinbase had “over-hired.”

Given that Coinbase was already in the red during Q1 and apparently still hiring, what happened between then and this week to change its view on hiring and operating expenses? Here, Robinhood provides some context.

Robinhood’s Q2

Looking at Robinhood’s May performance data, we can see that the company had the lowest combined level of daily average revenue trades (DARTs) from equity, options and crypto, apart from April. Admittedly, Robinhood crypto DARTs actually bottomed out in February and March, but the April and May numbers were sharply down from year-ago results, and part of the company’s two smallest monthly aggregate DART periods since May 2021.

Robinhood data showed that consumer trading activity continued to fall into Q2, something that Coinbase may have endured inside its narrower market focus of just crypto. Falling trading volumes can mean smaller revenues, and at some point, Coinbase likely had to bow to the fact that it could not merely constrain new spending — it had to cut existing spending, as well.

The market had already voted: After reaching a price above $350 per share in Q4 2021, shares of Coinbase started the year around the $250 mark. They fell during Q1 before a sharp descent in early May pushed them under the $100 mark to around $50.

So what?

We could bring in a ream of trading data at this juncture, but it doesn’t feel necessary. Coinbase scaled its expenses when its revenues were rocking, with crypto use cases seeming to proliferate daily. Getting caught in a market updraft and over-hiring is hardly a new issue for companies, meaning that Coinbase is not unique in having run afoul of its own success.

The gist, as far as we can tell, is that trading-revenue-based businesses should be valued more like gaming companies than enterprise software companies, despite attractive profits during boom times. For Coinbase and its rivals, that’s likely unwelcome news from a valuations perspective.

Coinbase Q2 2022 data and guidance will be a key sentiment check for crypto for the rest of the year. More when we have those numbers — or more layoffs are announced.