Rivian, the electric automaker backed by Amazon, Ford and a cornucopia of heavy-hitting institutional investors like T. Rowe Price Associates and Coatue, finally made its once-confidential IPO filing public.

The company, which started in 2009 as Mainstream Motors before adopting the Rivian name two years later, has exploded in terms of people, backers and partners in the past few years. Rivian operated in secret for years before it revealed prototypes of its all-electric R1T truck and R1S SUV at the LA Auto Show in late 2018. Since then, Rivian has raised about $11 billion ($10.5 billion of which was raised since 2019); expanded its Normal, Illinois, factory; hired thousands of employees; landed Amazon as a commercial customer; and, most recently, filed confidentially for an IPO.

Now, its S-1 is revealing more details about the company and its operations. According to its IPO filing, Rivian is officially based in Southern California, a detail that, believe or not, wasn’t so clear a few months ago. The company’s headquarters previously were listed as Plymouth, Michigan.

As of June 30, 2021, Rivian had 6,274 employees across the United States, Canada and Europe, according to its filing. The company has told TechCrunch more recently that it employs more than 8,000 people, an indication that its growth is accelerating. In addition to the Illinois factory and Plymouth office, Rivian has facilities in Palo Alto and Irvine, California as well as Arizona, Vancouver, Canada, the Netherlands and the U.K.

Media reports indicate that the company could pursue a valuation as high as $80 billion in its debut.

Certainly, there are a host of backers hopeful that that number — bandied about today as pre-IPO pricing numbers often are in companies that attract significant media attention — becomes reality. The TechCrunch crew has executed an initial dive through the company’s IPO filing, looking for intricacies, gems and possible headaches now that we’ve digested the news itself.

So, let’s talk just how expensive it is to build an EV company, why market size estimates are bullshit, what sort of voting structure Rivian intends to sport post-debut, how Amazon is a blessing and a sticking point for the company, why services matter and where Tesla crops up.

Sound good? Let’s have some fun.

It’s expensive to build an actual EV company, despite what SPACs will tell you

Folks love to say that it’s cheaper and easier than ever to found and build a startup. They are talking about pure-play software companies. It’s still incredibly difficult and expensive to build an EV company.

Evidence of that fact can initially be spotted in the sheer scale of capital that Rivian raised while private, just to get to the point when it has started to manufacture vehicles. But the company’s income statements shared in its S-1 filing are even more illustrative of the point.

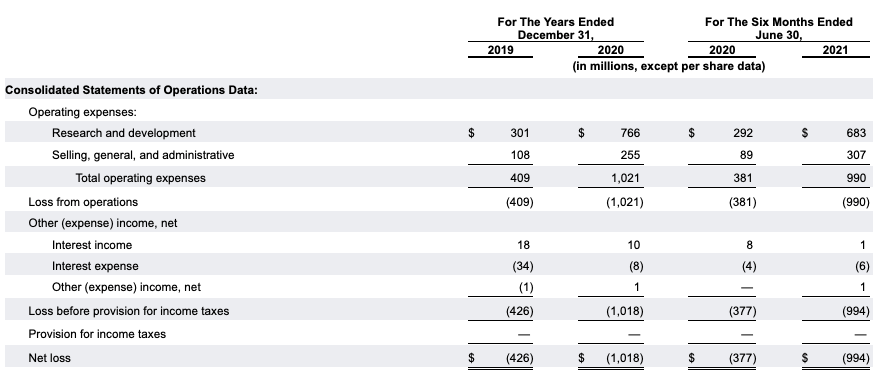

Here are the company’s operating results for 2019, 2020, and the first two quarters of both this year and the last:

Image Credits: Rivian

No, we didn’t make a mistake and miss the revenue line from the above graphic. It doesn’t exist because Rivian has essentially zero historical revenues to report; that of course makes sense because Rivian is just starting to deliver the first R1T trucks (revenue yay!) to customers. You can spy a dribble of income in the interest section, but that’s effectively it; Rivian has only made money thus far from simply having lots of cash, some of which generated a paltry return.

Past that the company has simply been spending — investing – heavily in its business, work that led to an expanding cost structure as the company got closer to fully turning on its manufacturing operations. In numerical terms, the company’s net losses grew from $426 million in 2019 to just over $1.0 billion in 2020.

The numbers have only steepened since then, with the company posting a net loss of $994 million in the first half of 2021 alone, far more than double its $377 million net loss the company posted in the same period of 2020.

Driving the huge gain in costs at Rivian are its R&D expenses. Naturally a company busy building out its first set of products will feature large research and development costs. But Rivian’s are scaling vertically. The company spent $766 million on R&D in 2020, or around $64 million per month. In the first half of 2021 the company spent $683 million on R&D, or $114 million per month. That’s quite a lot of spend to get the company’s projects ready to sell their first unit.

The lesson here is that the financial pain of building an EV company whose products are not bullshit and that has an actual hope of reaching scale only grows the closer it gets to production. So, the conviction requirement measured in dollars to get an EV company from idea to production vehicles on the road goes up with each quarter until the first unit is sold.

This is why you don’t see many successful new car companies out there, let alone new EV companies. Rivian is the exception, not the rule, and its red ink is the gulf it had to cross to get to today.

Market estimates are bullshit

As part of its S-1 filing, Rivian bigged up its market. This is standard practice for companies raising early-stage funding as much as it is for companies going public. They want investors to see as large a future for their business as possible, as the bigger the potential market the greater their potential future revenues. And that means bigger future cash flows, and thus more present-day market value.

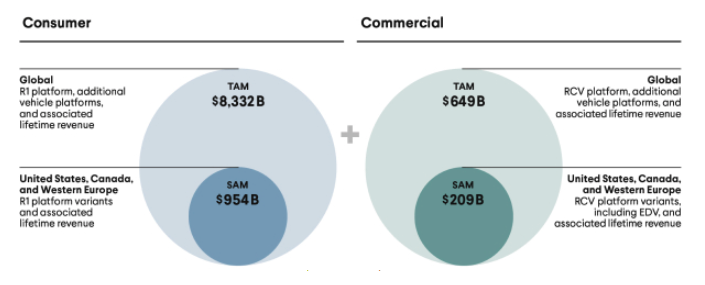

And they are largely bullshit. Here’s how Rivian talks about its total addressable market, or TAM:

Image Credits: Rivian

Yes, you are doing the math correctly, Rivian estimates that its TAM is around $9 trillion. That’s quite a lot! And it’s so large a number as to be effectively meaningless. Today the company has zero historical revenues, and, sure, the automotive market is big, but General Motors reported a mere $34.2 billion in Q2 revenues, for a run rate of $136.8 billion. That’s a mere 1.5% of the TAM that Rivian claims.

Do the math.

Dual-class shares are still hot

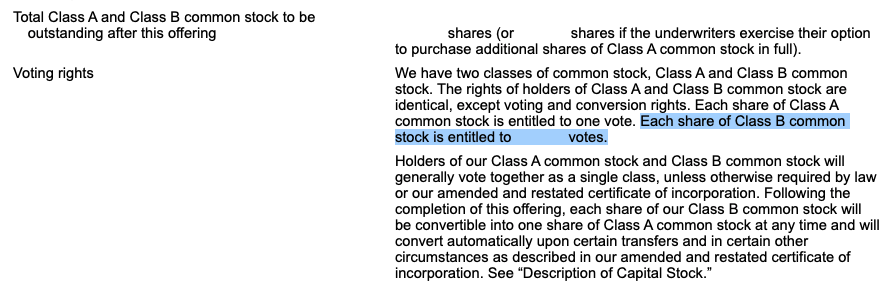

The Rivian S-1 filing is not complete, with some blanks left in until the company sets a first price range. As such we cannot precisely see how the company’s governance will shake out. However, we do know the following:

Image Credits: Rivian

Please excuse the awful screenshot. The highlighted section indicates that the number will not be one, as the company already noted that Class A shares get one vote. Class B shares will get more.

So, investors in the company’s IPO will be treated as second-class citizens in the company’s future. At least until Class B shares convert to Class A shares. So, the IPO will offer effectively worse equity, though it’s considered poor form in today’s frothy market to bleat such concerns.

Future businesses to bring in that sweet, sweet capital

Rivian has a number of future businesses in mind, if the contents of the S-1 are any indication. These are long-term objectives, meaning these will build off of existing business choices and will not happen tomorrow, or the day after that. Still, Rivian’s long-term intentions are important and help us predict its path to profitability as well as its cap ex.

Here is what stood out.

One of the first and most obvious next steps, per Rivian’s plan, is to sell a variety of vehicle variants that hit different price points. That likely means cheaper vehicles that fall below its current range of $67,000 to $75,000 EVs.

Rivian also has global expansion in mind. The company said it will focus on the U.S. and Canadian markets and enter Western European markets in the near term, followed by major Asian-Pacific markets. And to support those sales, Rivian plans to localize production — that means more factories.

Another obvious but important growth area is Rivian’s plan to offer integrated hardware such as charging, generation and storage as well as software-based energy management solutions in the residential, industrial and commercial markets.

The company said in its S-1 that it plans to build multiple vehicles within the consumer and commercial sectors. That commercial sector is interesting to me (Kirsten), especially after I noticed this little item further down, where Rivian says it believes it “will become the largest centrally managed EV fleet,” allowing the company “to unlock future service offerings, including autonomous mobility as a service for the movement of people and goods.”

Yes, autonomous vehicles people.

Rivian also sees a number of revenue streams beyond just selling EVs. Specifically, the company plans to create a marketplace to sell features and services that will be accessible thanks to over-the-air software updates. Those services might me automated driving features, financing and insurance. (More on services below.)

Amazon is a benefactor, risk

There are 81 mentions of Amazon in the Rivian S-1 filing. The number is high as Amazon is both an investor in the company and a customer. Per the filing, Amazon owns at least 5% of Rivian, though the final number is not yet available. Ford also has a stake greater than 5%, along with a number of investors.

But past investment, Rivian’s commercial fleet is largely designed with Amazon in mind. Which makes sense as the American e-commerce giant is expected to purchase some 100,000 vehicles from the company:

Our launch vehicles in the commercial space are a portfolio of EDVs designed in collaboration with Amazon. In September 2019, we entered into an agreement with Amazon under which Amazon has initially ordered 100,000 EDVs, subject to modification as described below under “Certain Relationships and Related Party Transactions.” We expect to deliver at least 10 vehicles in the month of December 2021. We plan to deliver 100,000 EDVs by 2025 and continue our relationship with Amazon thereafter.

We presume that the Amazon deal was key to Rivian managing to raise the capital that it has, as the deal gave it quite a lot of future revenue to bank off of while private and revenue-free. Still, the company’s strong connection to Amazon is both a boon — cash! orders! — and a risk. Per the S-1’s risk-factor section:

We expect that a significant portion of our initial revenue will be from one customer that is an affiliate of one of our principal stockholders. If we are unable to maintain this relationship, or if this customer purchases significantly fewer vehicles than we currently anticipate or none at all, our business, prospects, financial condition, results of operations and cash flows could be materially and adversely affected.

A bet on Rivian’s IPO, then, is in great part a wager that Amazon does in fact buy the 100,000 vehicles that it is expected to, and we’d add on a timeline and price point that work for Rivian. There’s a lot of room for things to go pear-shaped between 10 vehicles in December of 2021 and the delivery of the remaining 99,990 vehicles that Rivian expects to deliver to one of its key shareholders.

Services are key

In the software game, services are essentially blank revenue. Startups and unicorns alike often charge a breakeven price for services, as they are effectively loss-leaders for high-margin software revenues; if you can simply not lose money on services at a software company, huzzah, you are a winner.

Rivian’s model is not that. It’s actually somewhat services dependent. In its S-1 filing, the company noted that “services are a key part of our growth strategy, driven by initial attach rate, member retention and the subsequent adoption of future service offerings.” What counts as a service from Rivian? The company lists “financing and insurance, vehicle maintenance and repair, membership, software, charging solutions and FleetOS solutions” as possible services.

So, a mix of financial products (financing, insurance), repair, software and electric charging. It’s a grab bag of stuff, in other words and hard to grade on a gross-margin-potential basis. But it’s clear that Rivian doesn’t expect to generate all its gross margin from vehicle sales. Which may make good sense!

Indeed, while software companies treat services with disdain as they are gross-margin discretive, it’s the opposite at Rivian. The company explains in its filing:

We believe the services portion of our business will have the benefit of creating a higher margin, recurring revenue stream for each vehicle, therefore improving our margin profile. Our ability to grow revenue and our long-term financial performance will depend in part on our ability to drive adoption of these offerings.

The indication here is that the amalgamated services bucket of future revenues will sport better gross margins than the vehicles themselves. So, it’s the inverse of software; for Rivian, the extras will enjoy greater gross margins than the main product itself!

Two legal squabbles

Rivan’s IPO filing lists a few legal squabbles that it has to disclose and while some of this information is out there already, it’s worth noting here again. One involves dealerships, groups of rent-seeking businesses who want the legal right to stand between car makers and car buyers so that they can extract a fee.

Starting with the dealership issue, a powerful dealership network is taking issue with Rivian. This lawsuit seeks injunction, filed in March 2021, seeks an injunction and pits the Illinois Automobile Dealers Association, the Chicago Automobile Trade Association, the Peoria Metro New Car Dealers Association, the Illinois Motorcycle Dealers Association and “over two hundred individual franchised motor vehicle dealers located throughout the state of Illinois” against the company, barring the company from direct sales in the state of Illinois.

As TechCrunch has reported, Tesla filed suit against Rivian in July 2020, alleging trade secret theft by the company and various individual defendants. The suit also alleges breach of contract and California Computer Data Access and Fraud Act claims against individual defendants, but not against Rivian, according to the S-1.

Rivian stated in its S-1 that it intends to “vigorously” defend itself against both suits. And we know that’s true because Rivian has already fired back at Tesla.