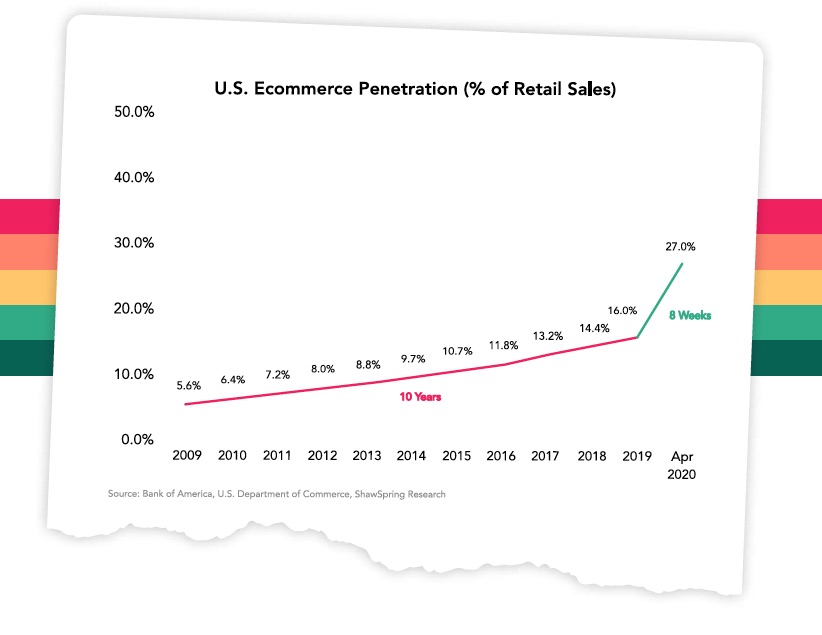

A lot has happened during the COVID-19 lockdowns in terms of human behavior.

E-commerce seems to have grown at the same rate in the last two months as it did in the last seven years. PipeCandy has been analyzing the segments within e-commerce that stand to gain the most with this “once in a generation” change.

One segment that has dominated the news and the M&A cycles within e-commerce is direct-to-consumer. The segment moved from being a disruptor of old-guard CPG companies to a channel strategy that every CPG company is now embracing. With lackluster IPOs of the likes of Casper, the closing of disruptor brands like Brandless and Walmart’s decision to not pursue D2C acquisitions, the era of hyper-funded digital natives is over.

So what’s up with digital natives now? How has COVID-19 played out for the segment?

Firstly, a comparison that some of you may not take very kindly. We are comparing actual retail sales from the U.S. Census Bureau with unique visitors from our sample of nearly 1,000 digital native brands. The directionality alone tells the story, even if we can’t compare the same metrics.

Image Credits: PipeCandy

What’s interesting about furniture is that people are buying storage units and shelves and tables for their home offices. Also, they are spending on mattresses. The rest of the furniture categories aren’t finding traction. That said, this observation is limited to D2C.

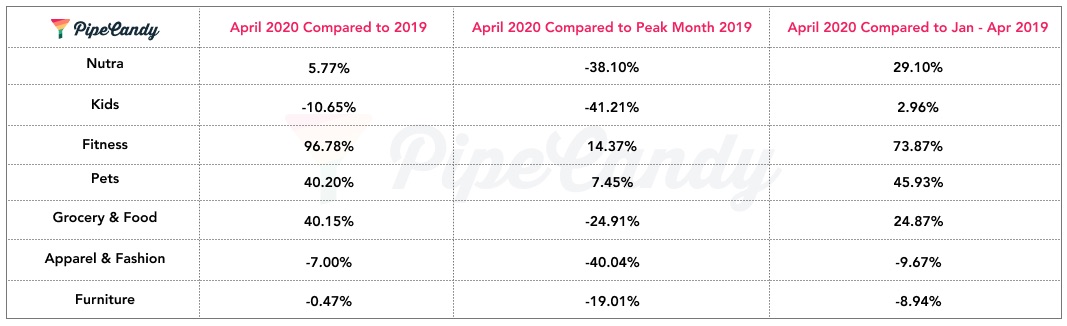

Now let’s see some D2C categories and their traffic growth trends over different slices of time.

Image Credits: PipeCandy

What you see above is a set of D2C category median growth rates of April 2020 compared to average growth rates in various time slices in 2019. We took April 2020 as the anchor month and compared against (1) the monthly average for every brand in the previous year and, (2) the month where they had the peak traffic.

The idea was to see not just whether these brands grew in April 2020 but also to see if they hit their peaks they hit in 2019. We have a few other cuts in our report (Q1 2019 versus Q1 2020, accounting for launch PR-linked peaks, etc.).

Fitness, pets and grocery registered healthy growth compared to 2019 averages, while the declines in furniture, apparel and kids have been minimal (when compared to the carnage we see in retail). But, when we see the data cut for peak 2019 versus April 2020, we see fitness and pets as categories have been resilient. We are still not back to the glory days of D2C in several other categories. Several categories and companies have been having a second lease of life. So what seems like a jaded performance when compared to the peak of 2019 is actually good news for several brands. They’d have been counted out but for COVID-19.

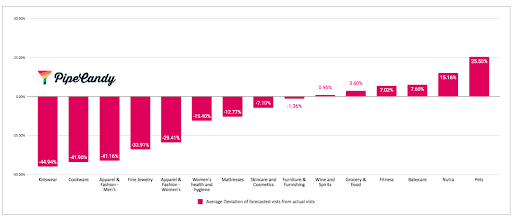

One way to truly size up the impact of COVID-19 is to look at the traffic numbers of these brands in 2019 and project the trends for 2020 assuming it would be a normal world from the vantage point of December 2019 and compare them with how things actually panned out between January and April 2020. We did consider and account for blips in numbers due to launch/PR activities in our forecasting model. The more positive the deviation is of the actual from the forecast, the better the category is doing.

I can only hypothesize that a certain virus caused the change in the trajectory.

Without, further ado, here is what we found:

Kids, cookware and kitchen tools, apparel, fine jewelry, fashion, women’s health, mattresses, furniture and skincare actually deviated negatively from the forecast. This is not to say that these categories declined. We are actually saying that these categories didn’t keep up with the growth trends they orchestrated in 2019. That said, the devil is in the details. For instance, within furniture, there is a category of D2C brands that sell shelves and office furniture. Consumers did invest in them heavily, presumably to allow participants in the Zoom call to absorb more the titles of the books stacked in those shelves than from the calls themselves.

Wine/spirits, grocery, fitness, baby care, pets and nutraceuticals did better than anticipated. Basically, anything that helped numb the reality (alcohol), sweeten the reality (food), distract from the reality (baby care and pets), survive the reality (fitness) or hallucinate an alternative reality (nutraceuticals) did well.

A summary of our findings (free) and a detailed report on the impact of COVID-19 on direct-to-consumer brands (behind paywall) can be found on PipeCandy’s website.

I will leave you with another interesting conclusion we arrived at, through further research that is currently underway: The spotlight category in e-commerce is not direct to consumer — it is the mid-market and large pure-play e-commerce companies. It is one segment where the compounded quarterly growth rate of active companies is better than the 2019 average.

We will have more to share in the coming weeks, so stay tuned!