Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

A year of aggressive growth

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

Subscription-based business model

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

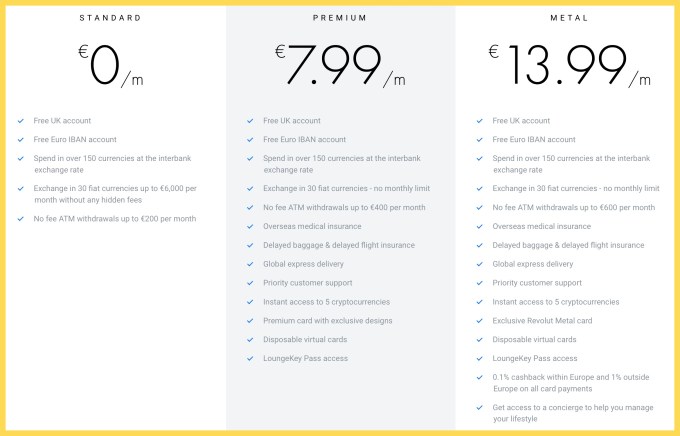

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Upcoming challenges

Challenger banks have been doing incredibly well, but they have yet to reach the scale of retail banking giants. Chances are you can find a lot of people around you who have opened a bank account from a challenger bank, but nobody is willing to ditch their existing bank account to go all in.

Here’s why:

- Banking is a local industry, even more than expected. Customers in the Netherlands need a Maestro card. Customers in many countries need local IBAN banking information for direct debits.

- The feature set of challenger banks is still limited. Don’t expect checks, traditional savings accounts or joint accounts (with some rare exceptions).

- Many legacy retail banks now offer features to freeze and unfreeze your cards as well as cards without any foreign exchange fee. They’re slowly adapting to competition and reducing the need for a second bank account.

- While many challenger banks are well-funded, traditional banks have some of the deepest pockets in the world thanks to investment banking operations. Traditional banks can undercut challenger banks on some features as a loss-leading strategy.

- The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country. Many challenger banks rely on local banking partners to take advantage of their licenses. But it’s going to take a while to build a true bank in the U.S.

- Valuations have skyrocketed. It has become increasingly difficult to imagine a challenger bank buying another one to increase its footprint.

- Many challenger banks have been criticized because their customer support teams are slow to answer. Some accounts may even be frozen until someone can deal with the issue — people want to be able to access their money 24/7.

- Tech giants, such as Apple with the Apple Card and Apple Pay, also want to offer banking products.

To be fair, startups also have a clear advantage over legacy retail banks. Some banking software is still written in COBOL, a programming language that is 60 years old. And software engineers are probably more likely to join a challenger bank over a traditional bank with tens of thousands of employees and a dated corporate culture. Challenger banks still are more likely to offer a better user experience over traditional banks.

In the coming year, let’s see if challenger banks have what it takes to build product that works well globally, customize that product to local needs without complexifying the product offering, and finally, expand to new countries at a rapid pace to reach mass market.