Over the past half a decade, the tidal wave of niche brands delivering new kinds of products to consumers and doing so online has changed the retail and CPG landscapes forever.

This shift has in some way caused a shakeout in traditional retail, with once-popular retailers announcing store closures (JCPenney, Sears) or even liquidation (Payless, Toys R Us) and has sent fashion houses and CPG brands on a soul-searching journey. The changing demographics and desires of shoppers have also fueled the decline of traditional brands and their distribution mechanisms.

This bleak scenario of incumbent consumer brands is in stark contrast to the rapid emergence of a host of digitally-native Direct to Consumer (D2C) brands. A few D2C brands have been successful enough to become unicorns! Retailers like Walmart, Nordstrom, and Target have quickly adapted to the D2C era.

Walmart has made a string of acquisitions beginning with Jet.com and Bonobos. Nordstrom has broadened its assortment to include D2C brands, Target has partnered with Harry’s, Quip, and Flamingo – all of which have rolled out their products in Target’s stores across the country. Target has also invested in Casper, which is the latest D2C brand to become a Unicorn.

Venture capital firms have invested over four billion dollars in D2C brands since 2012, with 2018 alone accounting for over a billion. With investment comes pressure to scale and deliver profits. And this pressure is bringing the focus on some pertinent questions – How are these D2C brands going to evolve and how could they sustain as businesses?

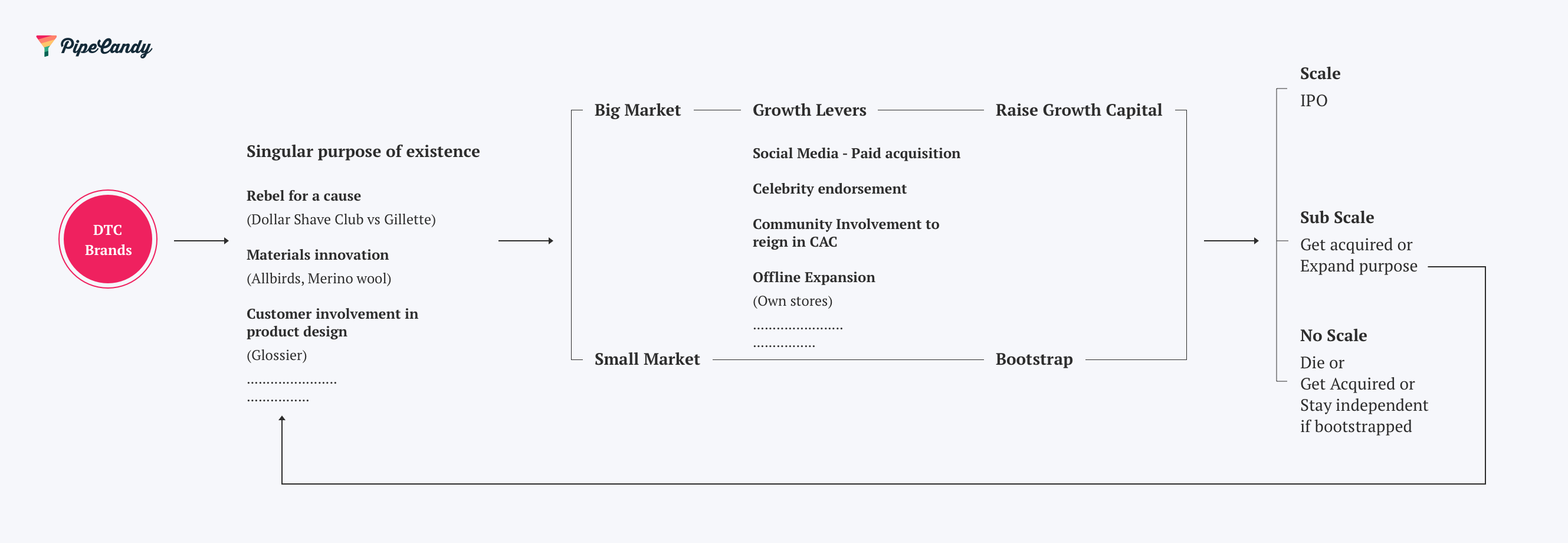

Like always, the pioneering companies find their path and we then derive the playbooks out of them. From PipeCandy’s analysis of several D2C brands, we see the following approaches taken by D2C brands.

- Playbook 1: Brand’s purpose anchored around one product category

- Playbook 2: Brand’s purpose anchored around multiple product categories

- Playbook 3: Brand’s purpose anchored around aggregation of other brands (for sale or rent)

We discuss the market size and capital availability factors that influence the paths and the outcomes.

Table of Contents

- D2C playbooks

- Access to capital and how D2C playbooks are impacted

- The VC route to scale

- The non-VC route to scale

- Outcome without hitting scale

- Roll-ups by strategic buyers

- Roll-ups by financial buyers

- Brand incubators

Brand’s Purpose anchored around one product category

Many of these D2C brands that have experienced early success owe their rise largely to an authentic relationship with consumers that is built on the promise of one product. In many ways, focusing on one product line and a small set of SKUs makes total business sense.

Design, Production, Marketing & Customer Support complexities can stay manageable with such deliberate narrowing down of focus.

In some categories, you could stay focused on one product line for a long time and build a successful company.

Image via Glossier

An example where a brand stays within one category and continues to grow would be Glossier. They play in the ‘beauty’ space. Their purpose is to give its customers’ opinions a voice when it comes to beauty. And the beauty market is over $500 billion in size, giving Glossier a big ‘target market’ to continue focusing on.

But in some categories, due to considerations such as market size and competition, diversification into adjacent product categories become inevitable.

Here is where being a brand anchored around a ‘concept or a purpose’ comes in very handy. Casper as a ‘mattress’ company is very limiting. But Casper as a ‘sleep’ company gives it the leeway to expand to many categories without diluting the brand’s purpose.

If you look at another success story, Allbirds, it’s a ‘Merino wool’ company with shoes being a category where the material innovation has been applied to. ‘Shoes’ is a sufficiently large category where they found a mega-niche of shoppers who believe in ‘comfortable shoes made from natural materials at an affordable price’.

But if you look at how ‘Allbirds’ is articulating its purpose (‘The journey to making better things in a better way’), switching from ‘We make comfortable shoes’ to ‘We make comfortable products’ isn’t a difficult leap in the minds of the shoppers.

In a slight variation to this example, some D2C companies innovate around a material or a substance. For instance, Marijuana or Hemp has many applications across health, recreational user, fashion, etc. A ‘Direct to Consumer’ brand that plays on the upstream side can build both a B2C brand and a thriving B2B business by making its products available for multiple uses (Example: CBD for end-consumer use and ingredients for pharma companies).

Brand’s Purpose anchored around multiple product categories

We spoke about Casper already. It’s a brand that has a singular purpose (Better Sleep) which manifested so far through a single product (Mattress). But already we see the product categories expanding – Glow, their range of light products that help you sleep better.

‘Direct to consumer’ brands’ biggest asset is not the product it has designed or the celebrity it has roped in. It’s not even its ability to acquire customers from Instagram. Their asset is their ability to anchor the purpose of their existence in the minds of the shoppers.

Product designs, new categories, better lifetime value, lower cost of acquisition – all come from mastering this one linkage between the purpose and the people.

Once that is established, it’s hard not to expand your product line to multiple categories anchored around that common purpose.

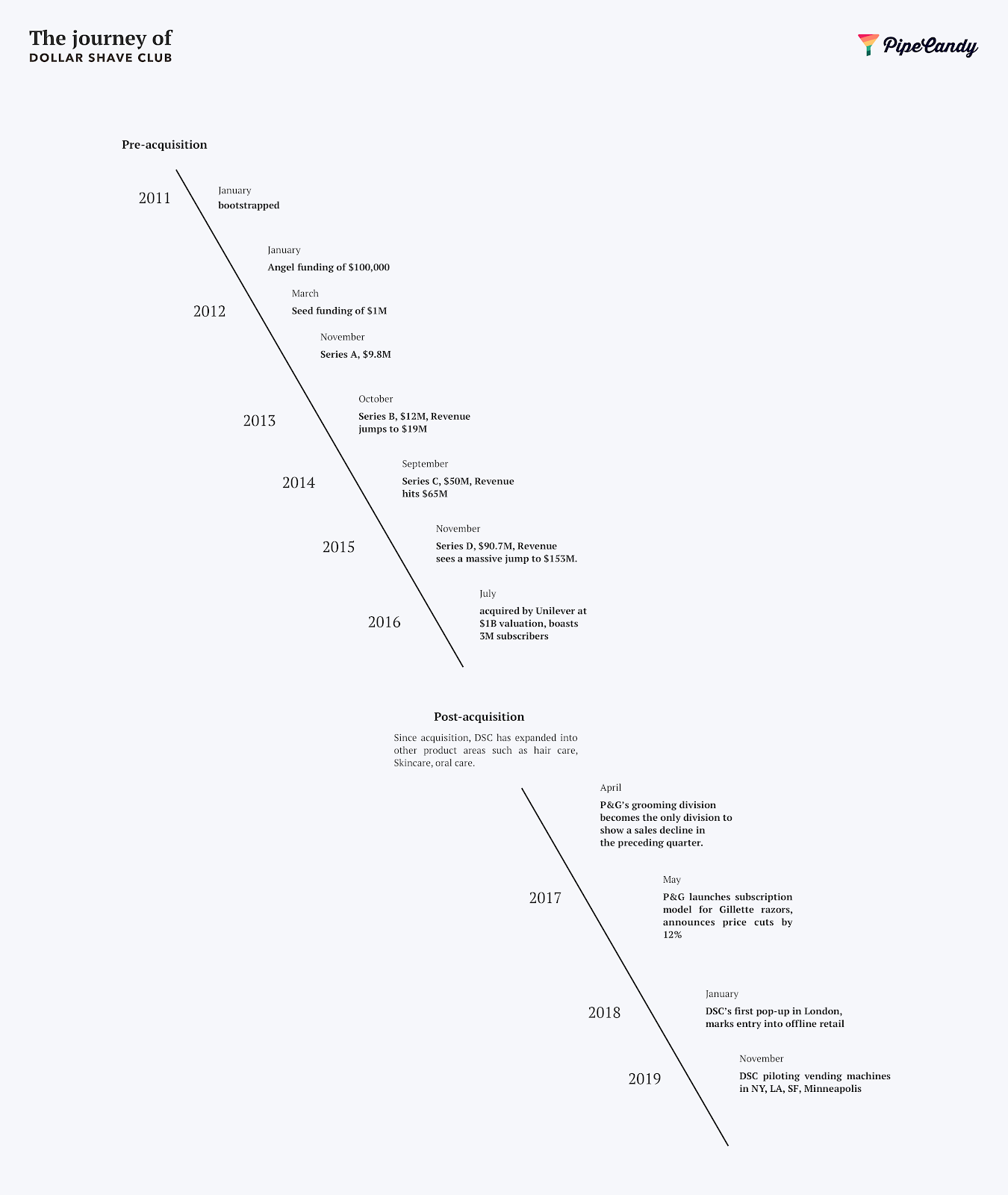

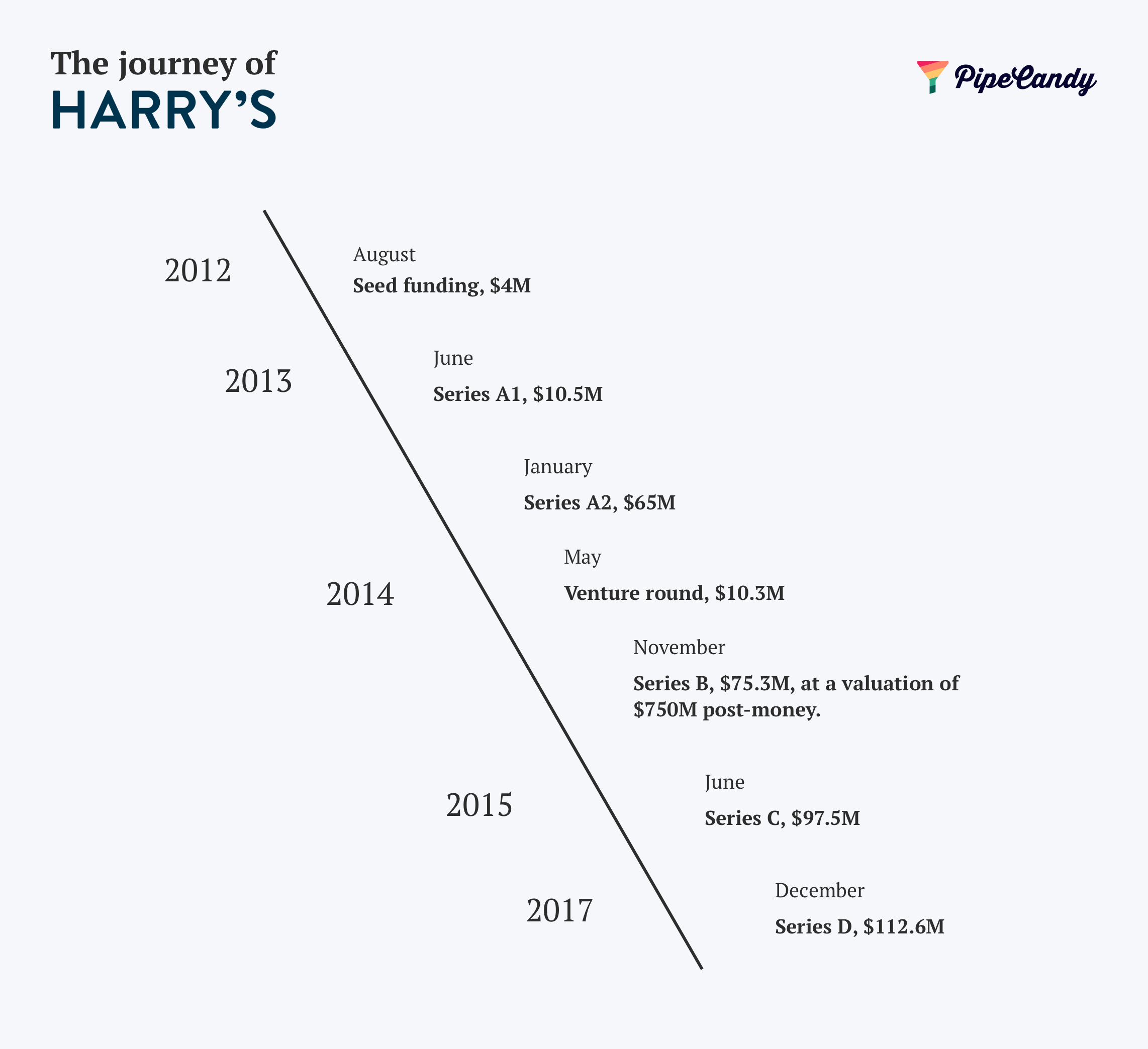

Harry’s and Dollar Shave Club fit this playbook albeit with slight variations. Both brands focused on shaving razors when they kicked off but Harry’s took the lead in expanding to adjacent product categories long before Dollar Shave Club did.

In the year leading up to Dollar Shave Club’s acquisition by Unilever, Harry’s had already ventured beyond Razors and launched its own Face wash, Lip balm and Face lotion – a clear manifestation of the company’s intention to become the ‘go-to’ brand for all things Grooming (and an early one at that), while still staying true to its core purpose of being a Shaving company – just like how Casper expanded from Mattress to all things Sleep.

Dollar Shave Club, however, ventured into the Skincare, Oral care, and Haircare categories only after its acquisition by Unilever.

Image via PipeCandy

Image via PipeCandy

Brand’s Purpose anchored around aggregation of other brands

When your purpose is to give your customers a sampling of the best clothes out there that are a good fit for them, it doesn’t matter whose brands you are recommending for sampling.

The story isn’t about one brand. It’s about how well the products are curated and personalized for the shopper. Stitchfix realized this early on. It’s this friendly fashion concierge that connect brands with shoppers but curates the experience for every shopper using the data about that specific shopper.

Image via PipeCandy

By being a curator of fashion, without having to own the product design or manufacturing, Stitchfix is able to scale while keeping a very healthy margin of over 45%.

Ipsy follows a similar model too. It’s no surprise that when your product is ‘recommendations’ and the revenue comes for your ‘wise counsel’, the way you make sustainable revenue is when there is a subscription element.

Stitchfix, Ipsy, and Birchbox – which is similar to the first two – are all subscription box companies, even as they are ‘direct to consumer’. ‘Rent the runway’ is a pioneer in using this playbook and weaved the trend of ‘renting’ instead of ‘owning’ the wardrobe. But to pull off such a change in behavior and to invest in the merchandise, you need capital.

And that brings us to the question of how these playbooks are impacted by the availability of capital.

Access to capital and how D2C playbooks are impacted

The D2C movement is in an interesting stage of evolution. There was a lot of capital, M&A and a sense of despondency among the investment community about the increasing CAC and capital costs. But there have also been companies that have crossed the billion-dollar valuations recently (Rent the Runway & Glossier). Add to these, the fact that there are going to be a lot of IPO millionaires, at least in the valley getting D2C brands out of the drawing board isn’t going to be a challenge.

For the D2C brands, there are several ways to get from zero to the IPO or a private market exit.

The VC route to scale

The success stories where the brands have taken VC investments have either had really large markets (Allbirds) or really strong following among the core audience (Glossier) or very strong, differentiating tech that led to an asset-light way to grow revenue and margins (Stitchfix). Often, it is a combination of more than one of these factors that have led to these companies to billion dollar valuation or IPO.

Lack of large markets are fixable (Casper). Lack of purpose and a strong purpose that connects the audience is not.

Also, many of the early-day VC investments in the category were based on the thesis that the brands can acquire customers online and there is no cap to that behavior. However, that has become prohibitively expensive over the years with many more brands fighting for clicks from the same cohort of customers.

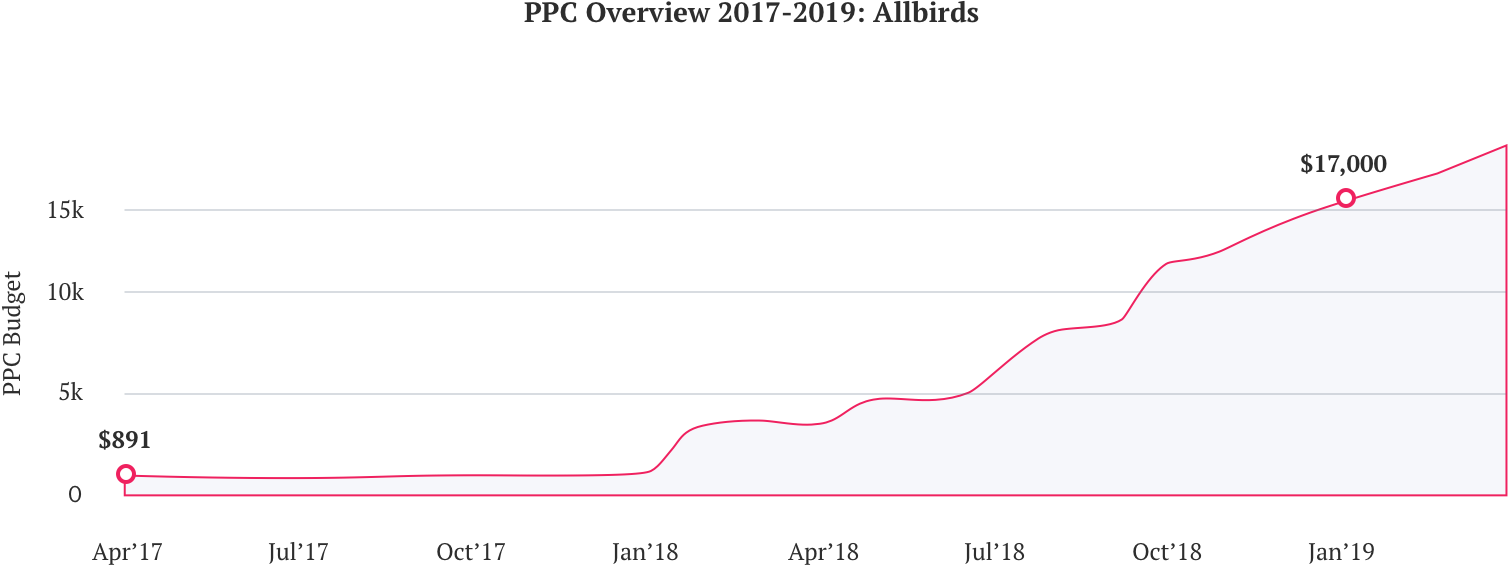

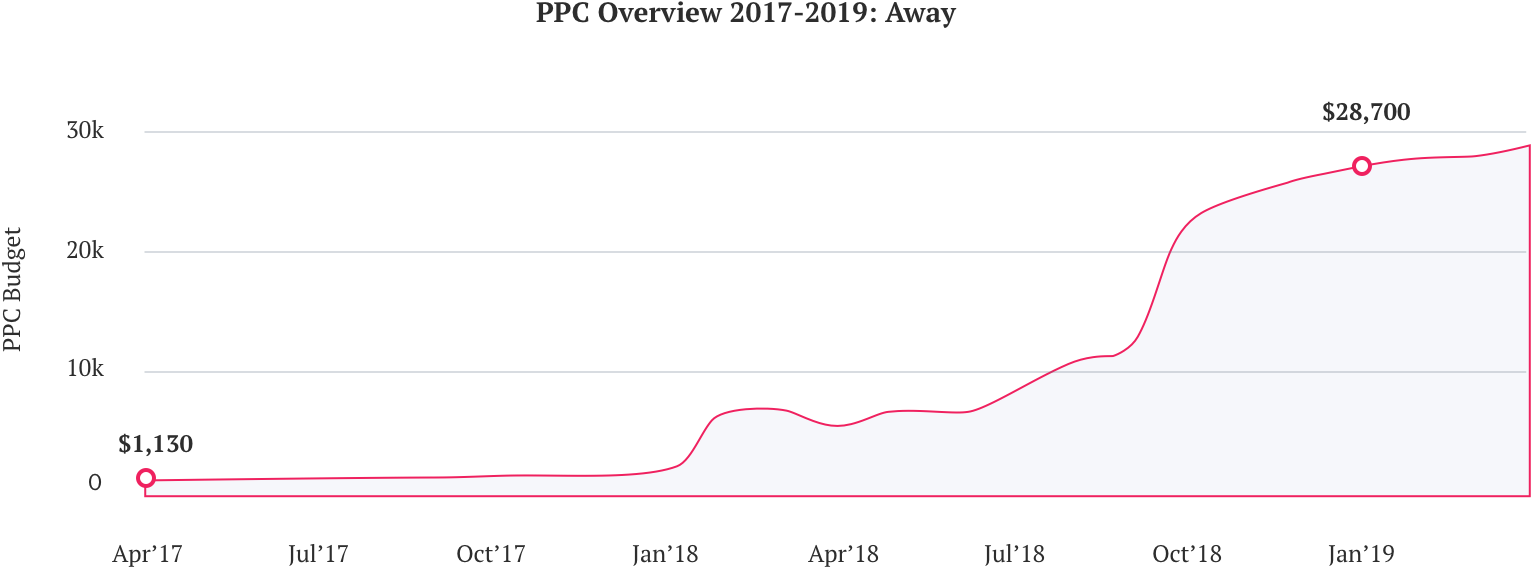

We looked up a couple of D2C brands across popular categories like fashion, beauty, travel, and sleep and found that between 2017 and 2019, these brands have increased their pay-per-click budgets by as much as 10-20 times.

Image via PipeCandy

Image via PipeCandy

The representations above, given by search analytics firm Spyfu, are estimates of what the domains (Allbirds.com and Away.com) spent in AdWords during the most recent month. Spyfu takes all of a domain’s paid keywords and uses the click-through curve to get an idea of how much the domain spent overall and then averages it out over a month. The spend increase over a two-year period is shown above.

If you are a D2C company competing with Allbirds or Away, you know that your CPCs are going to be expensive.

Offline expansion comes with capital costs as well, though the CAC is lower in the long run. But when a brand goes offline and competes with traditional brands or retailers that have figured out distribution, the battle for the shopper is fought in the terrain that is unfamiliar for most of the D2C brands.

Besides, the incumbent brands are learning social and community-building and have realized that ‘direct to consumer’ is a business model change and not a segment that is impervious to them. For these reasons, the VC interest in the space is likely to be muted.

But it will be interesting to see how it plays out, given that there are a handful of companies that are already in the billion-dollar valuation club or getting there.

The non-VC route to scale

There are companies like MVMT, Native and Tuft & Needle that have either completely avoided venture funding or have done them at their growth stages making it a very viable approach.

MVMT’s founders invested $5000 of their own money into their first Indiegogo campaign and raised over $290,000. Tuft and Needle’s founders invested $6000 of their own money and took a loan of $500,000 as well. Native raised a small round of $500,000 from VCs and that was it. The common discipline among these companies was reinvesting all of their profits back into the business and keeping the company independent. Tuft & Needle, in its time as an independent company, opened four brick-and-mortar stores and attributed a quarter of its sales to Amazon.

This non-VC or VC-light strategy resulted in successful exits for all three companies, with Movado acquiring MVMT for $100 million, P&G acquiring Native for $100 million and Tuft & Needle merging with incumbent Serta Simmons for an undisclosed amount. The deal was valued somewhere between $200-$800 million.

Image via Holly Kuchera / Flickr

Between the three brands, the average initial capital invested works out to $400,000 and the value of exit averages to $200 million!

Not all D2C categories are the same. In some, the cost of acquisition of customers and product development costs are so high that a capital raise is inevitable. The ability to stay bootstrapped/independent is also a function of identifying categories where there is a large spend, there are incumbents that have no brand affinity and there is a room for a capital efficient branded play.

Outcome without hitting scale

Inevitably a lot of D2C brands are going to look for an outcome without hitting growth orbits. That’s just the way the pyramid is stacked in any market. We have seen examples of these that have gone well as well as gone bad.

Roll-ups by strategic buyers

Jet.com is an active acquirer in the space, acquiring sub-scale brands. In 2016, Jet acquired Shoes.com (formerly Shoebuy.com), a once-leading online retailer of shoes, apparel, bags, and accessories. The company was making close to $300 million in sales in 2013 but just three years later in 2017, Jet.com acquired it for $70 million – raising speculations that online retailer may have been struggling to realize scale in a sustainable manner. The brand was eventually rolled up into Walmart’s portfolio of brands.

Walmart has made a number of strategic roll-ups in the Apparel and Fashion space.

In 2017, it acquired ModCloth, which was a story of struggle. The brand reportedly ran into profitability and culture issues post a leadership change – although some sources say they were profitable pre-acquisition. While the terms of its exit to Walmart weren’t released, industry sources say that the deal was valued around $80 million, which is about all the funding ModCloth raised ever.

A year later, Walmart acquired Bonobos for $310 million. The company’s then-founder Andy Dunn was quoted as saying in an interview to Recode that he was deliberating three options – either going for an IPO or ceding partial control to a private equity firm or selling to Walmart. The call was taken to merge with Walmart citing strategic advantages. This was a moderately successful exit for a decade-old brand that was valued at $300 million around the time of acquisition.

Eloquii, the plus-size clothing brand had a relatively more successful exit. The company raised $42 million in venture capital over 5 years and was acquired by Walmart in 2018 for two to three times that value.

In the luxury industry, we’ve seen conglomerates like LVMH acquire ‘D2C original’ brands like Rimowa, Christian Dior and Bulgari over the years. Estee Lauder has also rolled up D2C originals like MAC, Michael Kors, and Bobby Brown.

Image via Getty Images / Daniel Acker / Bloomberg

Roll-ups by financial buyers

As is the case with any playbook, this path has examples that went well and didn’t go so well.

Julep was founded in 2007 by Jane Park as a physical retail concept. The company was operating four nail parlors in the Seattle area at the time and in 2008, grew into a multi-channel online cosmetics brand, launching 300 new products each year. Investors such as Andreessen Horowitz poured more than $60 million into the company.

In 2016, Private Equity firm Warburg Pincus came along and paid $120 million to acquire Julep and two other brands and rolled them up under a new banner called Glansaol.

Glansaol’s plan was to create a portfolio of high-growth brands alongside competitors like Glossier and Kylie cosmetics. Due to differences in the core purpose of the participating brands themselves, this effort failed. Revenue dwindled until Glansaol filed for chapter 11 bankruptcy in December 2018. Julep was taken over by a company called AS Beauty.

While the roll-up was a deliberate move, a bankruptcy filing and acquisition by AS Beauty was certainly not the path Julep or Glansaol envisioned.

A brighter example was L Catterton’s roll-up of swimwear brands Seafolly and Maaji. In a move to create the largest independent house of beach lifestyle brands, L Catterton in 2017 rolled up two of its umbrella brands – Australia-based ‘Seafolly’ and Colombia-based ‘Maaji’. The brands collectively have a revenue of over $100M, placing them at the forefront in an industry that is extremely fragmented with over 3000 brands worldwide.

Brand Incubators

Like we’ve seen earlier, big corporations typically play the waiting game before reaching out and acquiring brands that fit their strategic interests. However, with the arrival of Incubators, these corporations are getting into the incubator game too!

Kendo (owned by LVMH) and Seed Beauty were the first ones on the scene. They were the baking ovens of popular celebrity and influencer backed brands such as Kat Von D, Marc Jacobs, Fenty Beauty, and Kylie Cosmetics.

These success stories stoked big corporations like Unilever, Revlon, and L’Oreal to set up their own incubators. They started pushing innovative brands from within the company rather than searching for external brands to partner with.

Seed Phytonutrients, for example, was born out of L’Oreal’s incubator. Sephora’s Accelerate, P&G’s Connect+, The Unilever Foundry are few other examples. Not to forget, Amazon has an accelerator too and it spun out its first beauty brand called Fast Beauty Company in March this year.

There are three main reasons why corporations are going the incubator way.

Firstly, it is just easier to invest in relationships with a range of early-stage startups through an incubator, with the assurance that the relationship and financial stakes will be maintained as the startups grow. Secondly, they are involved in every step of product development and fine-tuning, which helps fix mistakes early on. Thirdly, the time elapsed in execution from concept to creation is way more narrow in incubators than in traditional companies.

Seed Beauty reportedly takes five days from concept to creation which is in some cases years fewer than what traditional companies would need. With the adoption of the incubator model, traditional companies are realizing that the fast fashion model can be replicated for other products too!

Image via PipeCandy

To conclude, we see a recalibration of what ‘D2C’ even means. Traditional, incumbent brands are realizing the need to own customer experience and are embracing D2C channels either by launching their own online storefronts or experience centers, while modern digital native brands are getting acquired by incumbents.

It’s still hard to say if D2C as a standalone segment has come off age. Billion-dollar valuations for companies like Rent the Runway and Glossier aside, we believe that D2C is more a business model that will be widely adopted by brands of all vintages than a segment that will hold out on its own.