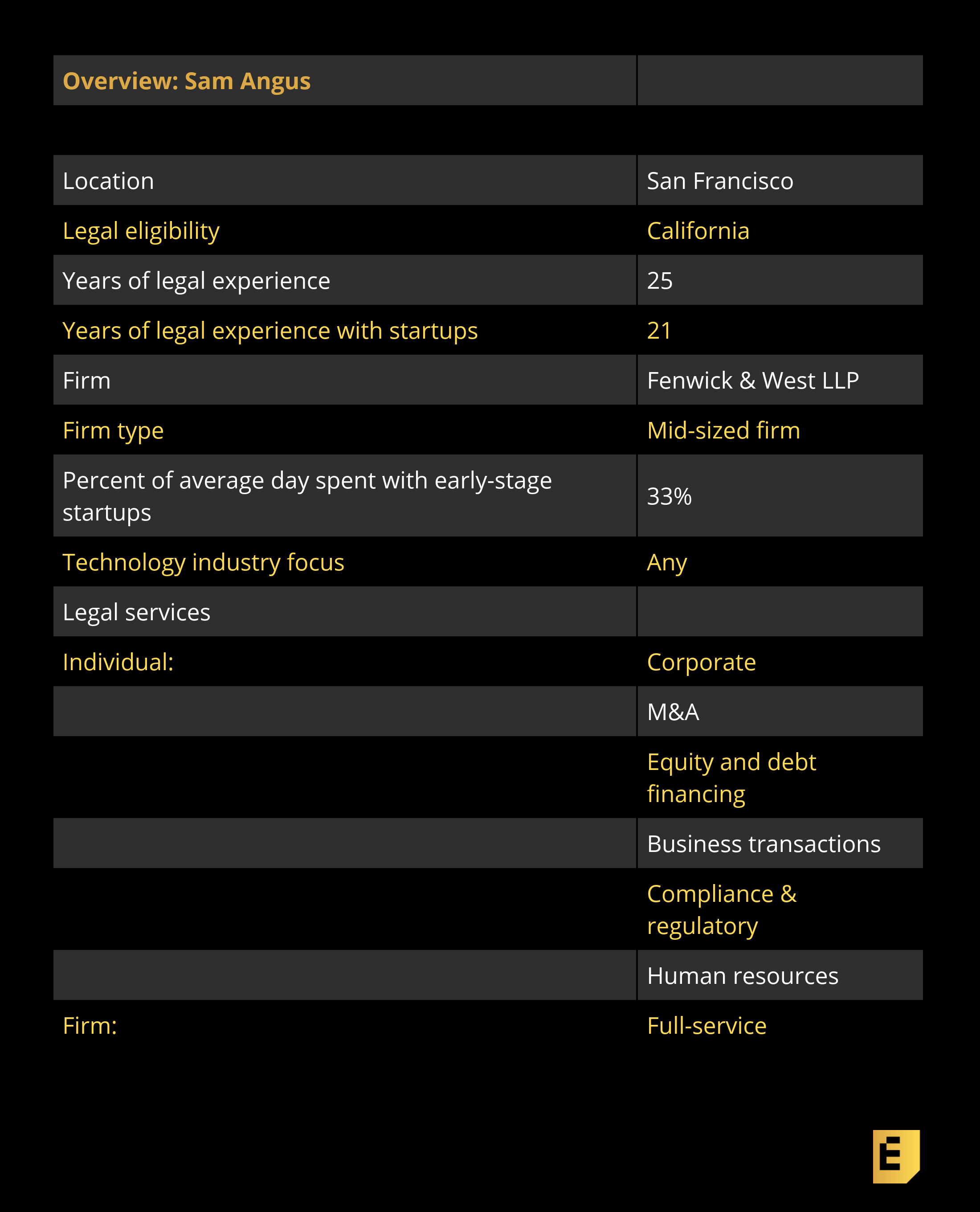

Sam Angus has been a lawyer in Silicon Valley since the 1990s. Today, he represents some of the biggest names in the startup world, from their earliest days through acquisitions and IPOs, and including four acquisitions last year: TSheets, GitHub, Glint and HelloSign.

But his startup experience actually goes back to the 1980s, when he and some friends built a booming calendar publishing business out of their dorm room during college. In the interview below, he tells us about the ups and downs of the tech industry over the decades, how he helps clients through the good times and bad, and how he works within Fenwick & West, one of the leading tech law firms in tech. We also discuss long-term trends, like the shift towards founder-friendly terms in this era versus past decades in the Valley.

On early-stage problems:

“I’ve represented hundreds of early-stage companies. It is not uncommon for companies to have some existing legal issue that needs to be addressed, such as capitalization, documentation and/or employee/IP issues. It is unfortunate, but these issues will frequently — especially with early stage companies — lie dormant and be discovered when the company is contemplating its first financing or a significant transaction, and can take investors or buyers by surprise.

“Sam is one of the most trusted partners that I have ever had and one of the most important people to Airbnb’s early history.” — Brian Chesky, San Francisco, CEO, Airbnb

“A common mistake is for a company to think that a given issue will not be a concern to an investor or buyers. In my experience, issues that arise on the eve of a financing or other transaction can create risk in the transaction and can be expensive to address quickly. For example, one client I worked with had been operating for years with virtually no documentation and not surprisingly had significant deficiencies in terms of corporate approvals. Very few things are fatal, but the result for this client was a bumpy and more expensive financing process — which required several rounds of explanation to the investors and their counsel.”

On being a startup lawyer:

“What I’ve learned is that the best lawyers for startups bring more than competent legal advice to the relationship – they act like business owners themselves, thinking strategically about the business. The best lawyers have significant experience and a knack for pattern recognition, the combination of which helps identify issues and opportunities in advance of when they become apparent.”

On risk-taking:

“There are some legal risks that early-stage companies will need to take. In my view, my role with earlier stage clients is to position them for success by being practical and focusing them on the issues that are material for a company at their stage of development. Overall, I want to empower clients to push the bounds of what they think is possible, while making wise business and legal decisions that won’t handicap them in the future.

“I would also point out that being able to scale with clients is extremely important. As clients grow, my role evolves to fit their needs – what works for a startup company is different from what a unicorn/growth company will need from their lawyer. With early-stage companies I tend to be more closely involved with the founders and the company’s business, while with later stage companies the relationship becomes more strategic and we tend to support internal legal teams and boards of directors.

Below, you’ll find the rest of the founder reviews, the full interview, and more details like their pricing and fee structures.

This article is part of our ongoing series covering the early-stage startup lawyers who founders love to work with, based on this survey (which we’re keeping open for more recommendations) and our own research. If you’re a founder trying to navigate the early-stage legal landmines, be sure to check out our growing set of in-depth articles, like this checklist of what you need to get done on the corporate side in your first years as a company.

The Interview

Eric Eldon: To begin with, tell me about Fenwick & West. It’s one of the original law firms that started in Silicon Valley and focused on tech companies, and you’ve been there for years through the various cycles.

Eric Eldon: To begin with, tell me about Fenwick & West. It’s one of the original law firms that started in Silicon Valley and focused on tech companies, and you’ve been there for years through the various cycles.

Sam Angus: Launching my career in Silicon Valley has provided me with a unique skillset and perspective that now enables me to thoughtfully advise clients who want to scale quickly, no matter where they are located. Working with fast-growing innovators, like those I’ve served since the tech boom of the 1990s, is in my view different from traditional approaches to practicing law. Providing clients with excellent legal advice is table stakes for any advisor to startups. What I’ve learned is that the best lawyers for startups bring more than competent legal advice to the relationship — they act like business owners themselves, thinking strategically about the business. The best lawyers have significant experience and a knack for pattern recognition, the combination of which helps identify issues and opportunities in advance of when they become apparent. Great startup lawyers also have extensive networks of investors, founders and partners and can leverage these networks to help their clients, address material operational issues, fundraise or complete a strategic transaction. They are efficient/cost-effective and move as quickly as their clients, and, most importantly, provide judgment. This entire skill-set is rare for lawyers, but when it comes in one package it is incredibly valuable to emerging companies. That’s one of the reasons why I love working at Fenwick: this approach to advising startups is simply how we practice.

Eldon: The legal industry is seeing real competition from online services and automation — how are you competing?

Angus: It is true that automation is impacting the practice of law, like other sectors of the economy. Because Fenwick works closely with innovative companies across the globe and sees how technology is changing things, we are among the firms leading the way to embrace this change.

For example, Fenwick has an in-house data and technology innovation team. Our innovation team has developed various automation tools and software products to augment and enhance the services we provide our clients. These include automated forms, client portals where clients can access all the data about their companies (i.e. key corporate documents, cap table, contact information for their Fenwick team, etc.), and use of tools such as Kira, an AI platform that automates aspects of document review in M&A deals, allowing us to close deals at a rapid pace while helping control costs.

Another innovation is our budgeting capability. Fenwick’s budgeting team provides our clients with timely and accurate cost estimates for projects and transactions, such as M&A or IPOs. Leveraging our proprietary deal data about hundreds of similar transactions, we are able to more accurately predict legal costs for our clients.

Eldon: Let’s go back to how you got into working with technology companies and startups.

Angus: In the early 1980s, after a short stint playing professional tennis, I was recruited to play tennis at UC Santa Barbara on a tennis scholarship. While at UCSB, I entered the entrepreneur world, starting UCSB’s first entrepreneur club with two friends in 1984. We also launched our own business, a publishing company that produced and distributed wall calendars.

Our growth was rapid: In our first year we did one calendar title, the next year we expanded to five calendar titles, the year after that 25 calendar titles, the year after that 75 titles, as well as a number of posters and other printed products. As our business grew, we started licensing popular culture content, which was something the calendar industry hadn’t really seen before. We were the first to produce the Michael Jackson calendar and the first Madonna calendar.

Eldon: You did all of this while you were in college?

Angus: Yes, though I ended up taking a break from college in 1987, one quarter shy of completing my degree, to pursue the business full time. By 1989, the company had grown to about 150 US salespeople, ten international distributors, and was doing roughly $50 million annually in gross revenue.

In the end, I ended up selling my interest in the company to the lead investor following resolution of various claims with the investor. Through that experience, I learned firsthand what it’s like to be a founder who had bootstrapped and had scaled the company with complex supply chain … and navigated investor issues.

Eldon: So why did you decide to become a lawyer?

Angus: I decided to become a lawyer, in part, because of my experiences with the law running the company. My father also was a lawyer and served as company counsel for a time. One of the more memorable moments was when we were sued by the estate of Andy Warhol over the company’s publishing a “Pop Art” calendar. We ended up prevailing in the case, meaning that we could publish the calendar, and the case was actually published in the Federal Case Reporter. That was a very … exciting experience.

But one takeaway from that experience is how damaging litigation can be for a small company — in our case the distraction and cost of litigation really was quite a disruption.

As a result, I also wanted to be a lawyer who worked with companies and businesses, helping them achieve their goals and guard against any potential issues, as well as navigate challenges efficiently should they arise.

Eldon: How did you get involved in the tech industry and Silicon Valley?

Angus: Following my graduation from law school in 1993, I ended up practicing law in San Francisco for a large old-line law firm.

By 1997 Silicon Valley was starting to really heat up. I had done a couple tech transactions while at my first firm, and from that experience I knew I wanted to work with startups and founders in the tech sector. That year, I left my old firm and moved to Fenwick, just as the first internet bubble was gaining steam It was a great time to be a corporate lawyer, working with founders and startups, and getting incredible experience with many different types of transactions. I became a partner at Fenwick in 2001 — just in time for the bubble to burst!

Following the bubble burst, the environment went from one extreme to another. It was an extremely challenging environment to operate, let alone raise capital. Suddenly down rounds, recapitalizations and distressed sales became the norm, and there were literally thousands of companies that burned minimal cash, but continued to exist (zombie companies).

While the industry has certainly stabilized since those days, it is still a very exciting space to practice with, with continual, rapid changes to stay on top of. Innovation and creativity are key — both for lawyers and startups.

After the bubble burst in 2000-2001, the power balance between founders and investors really shifted, with investors having significant leverage in financing transaction simply because capital was scarce. Because investors had a tremendous amount of leverage, the financings that did get done tended to have very pro-investor terms, such as multiple liquidation preferences, participating preferred stock terms, and full ratchet anti-dilution protection to name a few. It was during this period of time that the change-of-control bonus (or carve-out) plan really came into wider use. These types of plans are designed to provide management/employees with a bonus payment in the event of a sale of the company (usually a percentage of the sale proceeds) in which management would otherwise not get anything in the transaction.

There were also some very good lessons from this downturn, and the subsequent recession. Ron Conway came out with his famous manifesto first published after the internet bubble burst urging companies to reset quickly. After the 2007 financial crisis it was republished, along with the Sequoia presentation slides (RIP: Good Times). Both were perceived as dire at the time (and probably would be today), but in retrospect I think much of what they counseled was spot-on.

Eldon: But hasn’t it been a much longer-term shift towards founders getting better terms? Back in the 1960s and 1970s, once you raised your A round, you’d lose control of the company. Over the decades it’s shifted, where startup founders have been getting more and more control until we’ve reached the present, which seems to be employees, and early employees getting more because you’re basically in a talent war from the time you incorporate, right?

Angus: I think that’s very astute observation. You’re right, in the current environment the shift you describe has continued so that founders and employees now have a tremendous leverage. If one looks at current financing terms generally this particularly true, with many founders seeking protections for control of the company that would be unheard of ten years ago.

Contributing to this is the fact that over the last ten years or so there has been a meaningful increase in the amount of seed and venture dollars being invested into the early stage sector. The early stage funding ecosystem has changed significantly and in addition to traditional institutional VCs, there is now a professionalized class of seed investors/funds, which did not really exist before. There are also incubators and accelerators who are active investors, and alternative funding sources such as crowd funding platforms, Kickstarter, AngelList, the list goes on – the seed and pre-seed section is actually among the most active in terms of deal volume. Additionally, as has been the case for years in the Valley, capital gets recycled by successful entrepreneurs, who have a lot of money to invest. This is to say nothing about what is happing to valuations and fundings of later stage companies.

Eldon: How would you say your current practice is split between companies — pre-seed, seed, Series A, and then through the middle stages of Series B, C, D, and into later stages?

Angus: I’d say it’s really like a third, a third, a third, split between early stage, mid-stage/scaling/early growth (anywhere from post-Series A to Series D/E), and late stage/unicorn.

My practice moves in cycles and I’m always looking for promising new companies. Fenwick has been serving technology companies for 40+ years, and was one of the two original firms to launch in Silicon Valley — a core tenant of Fenwick’s approach is to represent founders/companies from early-stage through the entire growth/scale cycle and through to liquidity, the full company lifecycle. This approach requires taking a long-term view of the market and clients and recognizing that clients will be bought and sold and new clients will be started and grow. For instance, in 2018 four of my later-stage companies were sold — TSheets, GitHub, Glint and HelloSign.

Eldon: Tell me more about how you see the role of a startup lawyer for an ambitious, risk-oriented young company.

Angus: There are some legal risks that early-stage companies will need to take. In my view, my role with earlier stage clients is to position them for success by being practical and focusing them on the issues that are material for a company at their stage of development. Overall, I want to empower clients to push the bounds of what they think is possible, while making wise business and legal decisions that won’t handicap them in the future.

Angus: There are some legal risks that early-stage companies will need to take. In my view, my role with earlier stage clients is to position them for success by being practical and focusing them on the issues that are material for a company at their stage of development. Overall, I want to empower clients to push the bounds of what they think is possible, while making wise business and legal decisions that won’t handicap them in the future.

I would also point out that being able to scale with clients is extremely important. As clients grow, my role evolves to fit their needs – what works for a startup company is different from what a unicorn/growth company will need from their lawyer. With early-stage companies I tend to be more closely involved with the founders and the company’s business, while with later stage companies the relationship becomes more strategic and we tend to support internal legal teams and boards of directors.

Eldon: Since you have all this going on, what does it take for you to want to sign on an early-stage client? Because you’re taking a risk there in terms of your time.

Angus: Yes, for earlier stage companies there is certainly more risk, not unlike a decision an investor needs to make with a new investment. Each company and situation is unique, but generally when evaluating a potential client I pay attention to the founders and their background/experience, the traction the company has achieved to date (in terms of product development or revenue/customer validation), and the company’s realistic chances of getting funded.

Eldon: Experience in terms of degree, or in terms of things the founders have done in the past?

Angus: Mostly what experience they have and what they’ve accomplished in the past. The specific education degree is less important, though it can be somewhat of a proxy for smartness and domain expertise.

Eldon: One of the things I’ve heard, especially from the lawyers at boutique firms I’ve talked to, is: ‘we don’t represent VCs, because we don’t want that conflict, and all the big firms have that problem.’

Angus: Different lawyers have different approaches. My view is that you want a lawyer who has represented founders, companies and investors because they will better understand the perspectives of each of these constituencies, which can be very useful to the client.

In terms of my practice, I would say probably 85% of my clients are company/founders, and about 15% are investors (angels, VCs and later-stage funds).

And, I think the risk of an actual conflict is, as a practical matter, remote. Lawyers are ethically bound to solely represent the interests of clients. It is not uncommon for a transaction with a client to involve an investor for whom a lawyer may have previously done work for. I think what is more relevant is whether a company’s lawyer has relationships with investors/VCs that can provide helpful insight about market terms for financings or a particular investor’s priorities.

The other thing I would point out is that with the leverage shift to founders, there has been a prevalence of more founder-favorable corporate terms and structures, such as dual class voting stock, extended exercise period for optionees, transfer restrictions, voting agreements and secondary sale structures. I have had a number of founders ask to structure their companies to reflect the “most” founder-friendly structure that can be put in place. Founders have to be careful about what and how they ask for such terms. I think part of being a good lawyer is to advise your client honestly about the implications of such a structure/terms and that it may not be in the founder’s or the company’s best interest. Ultimately, it is up to the client to decide.

Eldon: On that note, tell me about some of the horror stories you’ve seen happen.

Angus: I’ll describe this in more generic terms, because I can’t talk about specific situations or clients. The potential for conflict obviously is greater when a company is not getting traction, having difficulty with product market/fit or some other problem that is keeping it from raising capital. A classic situation is when in the context of such difficulties the board or a founder to want to make a change in the founding team or executive management. This can be a conflict among the founders or sometimes investors (board) and executive management/founders. Navigating these situations can be tricky and how they are handled can have big implications for the company and the founders.

Another tricky situation is advising companies with husband-wife or family founding teams. These can be very difficult partnerships given the emotional dynamics, especially if things are not going well with the company or in the relationship.

Disputes over equity or IP ownership are also common issues and tend to be the thorniest to work through. There are also issues that can come up where a company isn’t doing well and needs to raise capital, and the only source of investment is from insiders. The terms of these inside financings often will provide for significant reduced valuation for the company (a down round) and the existing investors who do not invest will suffer punitive change to their existing investment. These types of financings can be fairly complex, and affect the investors but also the employees who remain with the company.

Finally, serious issues can arise by not choosing your investors/partners carefully — these are long-term relationships and need to stand up through good and bad times. That is something I always stress with clients.

Eldon: That sounds messy, but also a later-stage problem. Tell me about when you’ve helped navigate a younger company through a tricky situation.

Angus: I can’t really discussion specific situations or clients, but generally with later stage companies the more common issues tend to be focused on executive/employment matters, corporate governance and board issues, as well as paths for employee and investor liquidity. A key issue facing many private late-stage companies is how to provide come liquidity for employees; we are seeing more secondary transactions as result.

Eldon: Let’s end with the basics: Billing

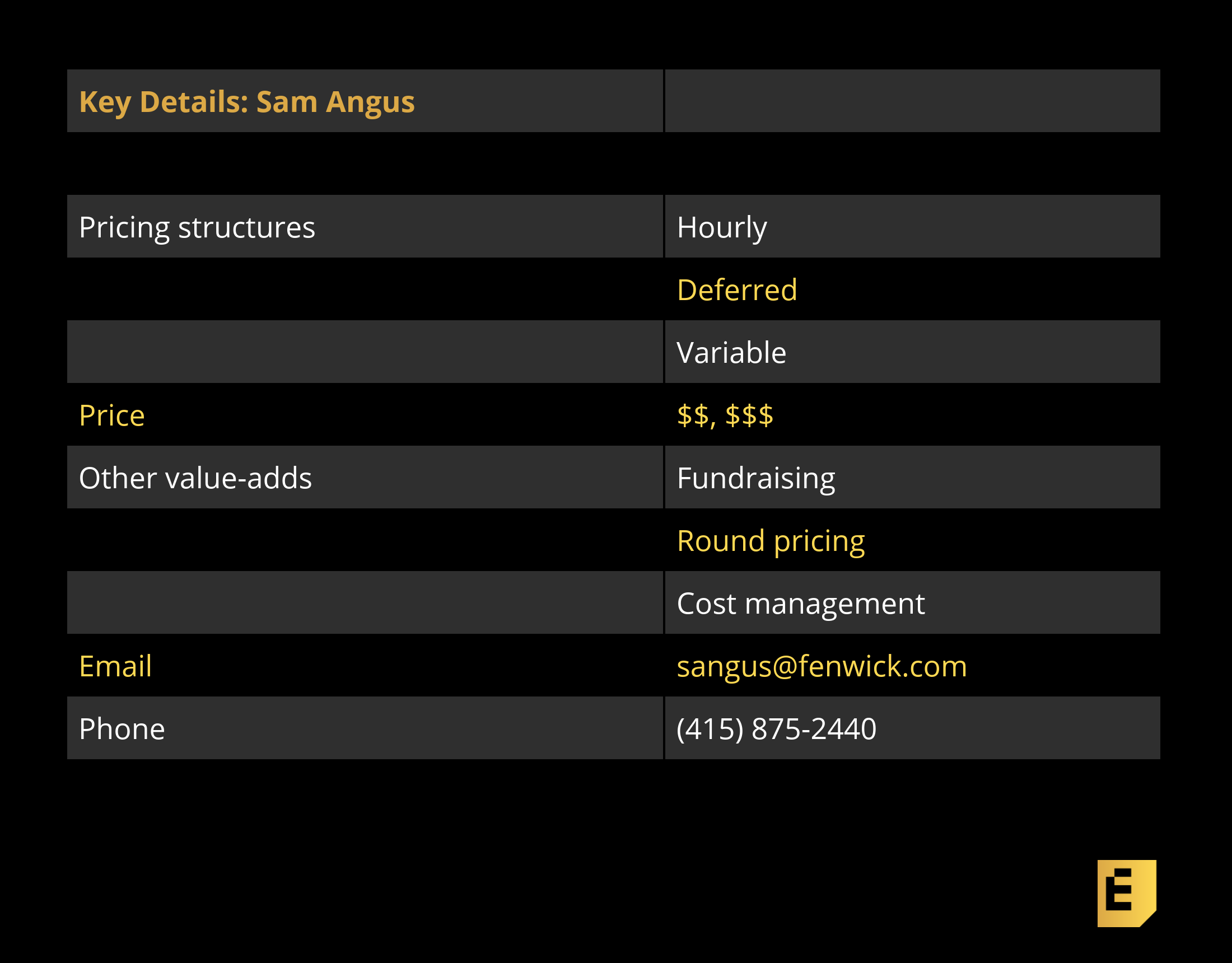

Angus: We typically bill by the hour, although we will do fixed fee billing arrangements for specific types of transactions if that’s what the client wants to explore. For startups that qualify, we offer a discounted fee structure, a deferral of fees (up to a cap), and we’ll attend regular board meetings for free. A law firm is part art, part science, and a lawyer’s relationship with his or client is really the art part of the equation. I view my role with early-stage client to set them up for success — I want to get these clients out of the gravity of the early-stage startup phase, so they scale and become market leaders, and do lots of transactions.

This means for certain clients on certain matters I will have off the clock time with them. If there are issues on billing, we work with them. That’s just part of the investment in the relationship.

We recognize that clients, especially startups, want predictability with their legal spend. I think many founders feel that early on they can use one of the many do-it-yourself legal documents, and handle the formation on their own, and when it is ready to raise its first round, then engage with a law firm.

I’ve represented hundreds of early-stage companies. It is not uncommon for companies to have some existing legal issue that needs to be addressed, such as capitalization, documentation and/or employee/IP issues. It is unfortunate, but these issues will frequently — especially with early stage companies — lie dormant and be discovered when the company is contemplating its first financing or a significant transaction, and can take investors or buyers by surprise.

A common mistake is for a company to think that a given issue will not be a concern to an investor or buyers. In my experience, issues that arise on the eve of a financing or other transaction can create risk in the transaction and can be expensive to address quickly. For example, one client I worked with had been operating for years with virtually no documentation and not surprisingly had significant deficiencies in terms of corporate approvals. Very few things are fatal, but the result for this client was a bumpy and more expensive financing process — which required several rounds of explanation to the investors and their counsel.

Don’t get me wrong, I’m a huge fan of automating certain legal processes, and Fenwick has developed and is developing tools for certain workflows.

Eldon: In terms of outsourcing some of the more rote work, or specialty work, how do you decide about that?

Angus: It’s totally up to the client. While Fenwick is a full-service firm— patent, IP, licensing, litigation, employment, corporate, tax, employee benefits—if a client has a relationship with a different patent shop, for example, they are certainly welcome to work with them as well. We also have a program that Fenwick has developed (called Flex by Fenwick) that allows clients to engage on-site contract lawyers vetted by Fenwick at a lower cost structure.

Eldon: Any closing thoughts?

Angus: Pay attention to the details — they matter. Make sure you know your co-founder and investors well — if you are successful, they will be long-term relationships. That’s extremely important. And, I would say, start working early with a lawyer, even if you want to do the documents yourself, start working early. You can avoid a lot of headaches that way and a good lawyer can help advise clients on market terms and navigate critical relationships.

Founder Recommendations

“Sam was instrumental in providing strategic and tactical guidance in the formation of our marketplace. He helped us navigate through the jungle, beyond the dirt road and onto the highway over a nine-year journey.” — Gary Swart, Palo Alto, CA, currently a partner at Polaris Partners; at the time the CEO of oDesk

“Sam has been the backbone of our non-employee legal team since [the company] first raised money with 60 or so employees. Through financings, acquisitions, separations, and all the day-to-day workings of growing and scaling a company, Sam has been instrumental. It also really helps that he’s easy to talk to, a good listener, and a great communicator. I’ve enjoyed working with him and the occasional dinner.” — A cofounder of a large unicorn that has been acquired

“Sam is an expert in startup formation and how to develop a company to then be able to do business with enterprise customers, hire and retain the best team, and receive investment from world-class institutional investors and angels.” — Chris Lien, San Francisco, founder and CEO, Marin Software

“Sam has provided excellent contributions on negotiating the best investment deals and term sheets for our past two financing rounds. He is a skilled negotiator and an expert in navigating complex deals (especially since we had corporate investors involved).” — A founder in Portland, OR

“Sam helped us in a number of ways, including advice on entity structure, feedback on our Series A deck, offering intros to investors, & recommending exit strategies. He’s also an overall great guy.” — Sean O’Brien, Las Vegas, Nevada, CRO at CHSI Technologies

“Critical advice and counsel on financings, M&A and business strategy” — A CFO of a unicorn company based in San Francisco

“Sam is one of the most trusted partners that I have ever had and one of the most important people to Airbnb’s early history.” — Brian Chesky, San Francisco, CEO, Airbnb

“Led Turo’s financing rounds (220M raised), M&A (5 acquisitions) and corp dev.” — Andre Haddad, San Francisco, CEO of Turo

“Sam’s experiences with successful unicorn venture-backed companies from early days to multi-billion dollar valuations gives him key business insights that are relevant to other companies as well. He’s my go to lawyer when any of my portfolio companies wants to trade up.” — Howard Hartenbaum, San Francisco, General Partner, August Capital

“Sam was one of the first believers in our business and helped us navigate everything along the way, from dealing with payments compliance on every continent, establishing new forms of insurance, and growing our legal team. He played a key role in the early days of the company, and continues to work with us to this day. I’ve recommended him dozens of times to entrepreneurs who want a legal expert on their side, fighting for, not against, their ideas.” — A cofounder of a large unicorn company in San Francisco

“Sam is an incredible attorney. He is by far the best outside counsel our company has worked with and he never fails to advocate strongly on our behalf in every transaction. Sam has represented GOAT since its inception and through several pivots. His expertise and knowledge with respect to emerging companies has been invaluable. He exhibits all of the qualities and characteristics of an excellent legal representative and his level of service is unparalleled. Sam approaches all legal matters from a business-friendly lens and is constantly thinking of creative solutions for complex matters. He is easy to work with, responsive, and unfazed by tight timelines and difficult opposing counsel. Sam deserves high praise.” — Eddy Lu, CEO and cofounder of GOAT Group.

“A great business partner, not [just an] attorney. Brings relevant experts when helpful. Also can see around corners on legal and business issues… helps in setting stage for hypergrowth.” — Andrew Swain, cofounder of Sundae, former CFO of Airbnb

“Preempt is the third company that Sam has helped me with. He was with my first company from start to finish, from formation to exit. He helped us navigate the entire process very well, including through 3 funding rounds. At Preempt, it has been the same. From corporate law, to compensation to IP, he knows how to help us think through the challenges both from a strategic and legal standpoint.” — Ajit Sancheti, San Francisco, cofounder and CEO, Preempt Security

“Sam led all of our early legal undertakings, including all the fundraising rounds (very sizable), regulatory assessments, liability issues, etc.” — Nathan Blecharczyk, San Francisco, co-founder and CSO, Airbnb

“Three financings (including a recap), international expansion, tax advice, HR advice, shareholder interface … Sam is an All Star in so many disciplines it’s amazing.” — Mark Rabe, San Francisco, CEO of Sojern

“Sam was my lawyer at my second startup, which I sold to [a major enterprise software company]. I hired him after I fired [another leading tech law firm]. I have recommended him to people ever since. He is a very good balance of ‘business advisor’ and lawyer. All too often lawyers simple tell you what clauses mean but not how to think about them commercially. Sam does both. He guided me through my sale. Actually, he tried to talk me out of it :) and give how well Box and Dropbox did (I was before them!) perhaps I should have listened.” — An entrepreneur turned VC in Los Angeles

“Sam has been outside counsel to my last few companies and several companies where I was on the board. He is exceptional in every respect. Extremely knowledgeable and competent, great instincts, very collaborative, overall top notch. Over the past 20 years, I have worked with great lawyers from leading firms like Latham, Wilson, Fenwick, Wachtell, and Skadden, and Sam is one of the very best.” — Jim Barnett, CEO and co-founder, Glint, SF Bay Area

“Sam has provided excellent service advising the company and was instrumental in helping us successfully close our Series A and B rounds.” — A GC of a growth-stage startup in Columbia, MO