Seed funding is drying up. Accelerators are scrambling for revenue. Things are changing drastically in the startup ecosystem.

Why?

First, as we all know, it’s easier than ever to build a startup. An MVP can hit the app stores in a few days and the need to raise millions for servers and software is over. Second, investors want to see traction, and few will take risks on relative unknowns. So how do you raise money when your product needs more than some Django code and an AWS instance?

You run an ICO, right?

We’ve heard the hype: It’s a get-rich-quick system meets Kickstarter! You can raise millions in a few minutes! There have been hundreds of successes! It’s completely safe!

All of these points are correct. But all of these points come with huge caveats. Welcome to the strange new world of token sales. Let’s explore.

Wait, what?

Token sales are, quite simply, a process of generating and selling a new cryptocurrency. While the details change from sale to sale, this process involves building a smart contract on the blockchain, generating, and then selling the resulting coins. The process usually involves lawyers, qualified investors, and a final public sale, and is at once a virtual roadshow, a circus and a community-building exercise.

First, some definitions.

In this process you are selling cryptographically generated tokens. These are digital objects that represent something in your business. You can use tokens to represent almost anything — free shirts on a t-shirt site or beers from a brewery. But what you can’t do without a great deal of legal cover — at least in the United States — is use tokens to sell equity. And that is where most token sales efforts stop: the SEC doesn’t want you horning in on its territory. Outside of that, for the most part, everything else is fair game.

We’re going to go into this piece with a few basic truths for Americans. These are not always applicable outside of the U.S., and many founders simply run their sales outside of the country to avoid dealing with the SEC and other parties. I’m not going to discourage or encourage this. It’s your call. The legality of these sales around the world is still up in the air, and there is a fine line between tokens and penny stocks, a fact few want to admit.

Further, token sales are not a funding vehicle. While many companies treat them as such — and crow over multi-million-dollar raises that explode in minutes — what they are really doing is floating a cryptocurrency on the open market. With a lot of planning and a lot of luck, these cryptocurrencies can rise in value and, if the token sale is structured correctly, this gives companies a little bit more funding than they had before they started. Without planning, you get a mess.

Tokens are supposed to be part of the life-blood of your company. Just as Disney Dollars once gave you access to Disney merchandise, Uber Bux should in some way give you access to some software made by Uber and Krablr Koins should give you access to an aspect of your new crab-fishing system. Companies have gone through all sorts of acrobatics to get their coins to work for their business, including pegging a token to a gram of synthetic rhino horn. Again, no judgement. This is a safe space. If you want to sell a massage token or popcorn token or a token associated with robotic speech generation, nobody can stop you. Once your Krablr Koin is minted, the little crab-dedicated economy you’ve built should be self-sustaining. That’s where you “make” your money — on speculation on your own success.

Token sales are set to replace traditional angel and seed rounds, this is clear, and can even completely disrupt VC. But how — and when — they do this is also unclear. So, ultimately, should you do a token sale?

Again, it depends.

Let’s look at a successful one.

Inside a token sale

Eyal Hertzog is the co-founder of Bancor, a fintech company that had the recent — some would say dubious — honor of “raising” $153 million in three hours to create a product that will render cryptocurrency exchanges obsolete.

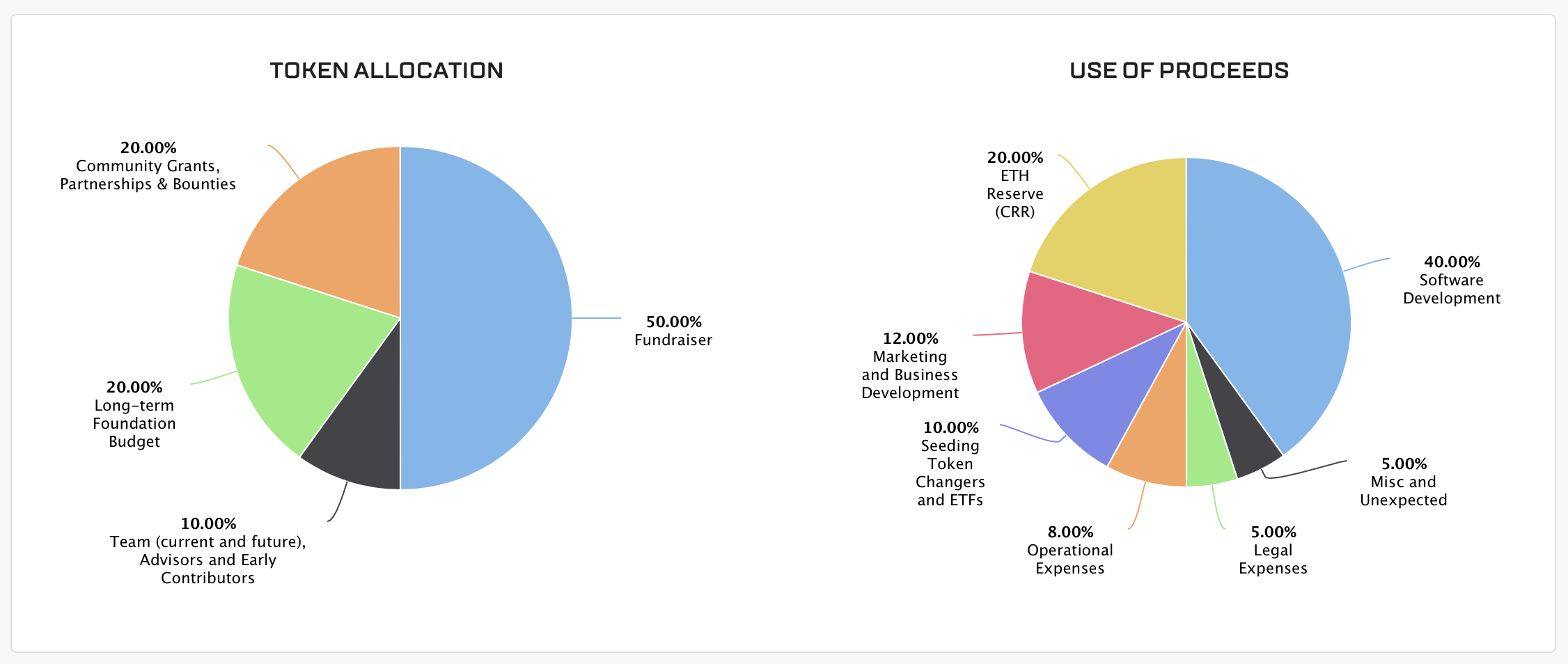

First, a bit of explanation. What Bancor did in this case was well over 76 million tokens. The tokens went out to early investors for a far lower than their current price $2 and rose immediately upon launch. The price has stabilized and current Bancor token owners can buy and sell these tokens as they please, thereby creating a real market for what is essentially a cryptocurrency.

Owners of the token do not own a part of Bancor but instead own a token that will be used in its product. As a notable New York Times article explained, imagine Bancor is a casino and raises cash by selling chips to early investors. Casino-goers will eventually use these chips at the gaming tables, but until that moment the chips hold a potential value based on the expected popularity of the casino. If enough people will pay $5 for a blue chip that once cost someone $1, you’re going to have a lot of happy investors. Bancor, however, did something even more interesting.

Hertzog said:

We decided to launch a Token Allocation Event because we had a design for a promising protocol token – BNT, the Bancor Network Token, which is based on our Bancor protocol. It’s important to emphasize that this is not a for-profit startup fundraising round, nor is this a basic application token. The fundraiser was executed by a Swiss non-profit foundation, that has a mandate to use its funds in order to develop and promote the open-source Bancor protocol. On top of this we (and others) can build and operate services, such as the “Bancor Network” service, which will provide a simple to use UX for issuing, using, transferring, purchasing and liquidating “Smart tokens”. Smart tokens use the Bancor protocol to ensure their continuous liquidity to any other liquid store-of-value (Ether, Bitcoin, USD, EUR, etc.) BNT will serve as a backbone, liquidity providing token for all user-generated smart tokens that will hold it in reserve, linking all these new tokens to each other, and to ETH and other existing currencies through BNT. BNT will increase in value as more smart tokens are created, benefiting all the smart tokens which hold it in reserve. It is a true network ecosystem, where more users benefit everyone. It would not be possible to create this momentum and incentive structure (where early adopter are disproportionately rewarded if the network succeeds) by using another token (like ETH).

In short, this is a building block for a future product and may not even be used in the product itself.

In this kind of sale, a few things happen that make writing about these things problematic. First, remember that Bancor didn’t “raise” $153 million. It raised a fraction of that. And, unless it wants to tank its own token, it cannot move much of its own tokens without moving the market. Every company in this case is Satoshi Nakamoto sitting quietly on a hoard of coins hoping to one day sell.

How much did Bancor “make?” In most token sales the company holds back a certain number of coins — usually millions — that it can now buy and sell to support its operations. The founders, we also assume, hold back a few million, as well. In this case the company held back 10 percent, or 3,960,000. Buyers, at least in this case, own their own millions of tokens and, because they are liquid, can move them in and out of Bancor at will.

Bancor will “use its funds in order to develop and promote the open-source Bancor protocol.” The astute among you will note that this opens the door for another token sale down the line and that there are also plenty of tokens left to sell later.

Further, Bancor had to be very careful. Token sales have been beset by a number of problems, including scams to steal Ethereum. The simplest way to do this is to post false information about sales, sending potential buyers into a fake account. Other hackers have simply changed the collection address on the token sale site. Millions have been funneled away from the sellers this way.

Danger!

A few things can happen to the hapless token seller. Hackers are sniffing around the space and have figured out some clever tricks. For example, one hacker changed the target Ethereum address during the CoinDash token sale and stole $7 million worth of Ethereum overnight. This sort of behavior is happening almost daily — hackers or con artists pop up in Slack telling users that token sale sites have changed and pump-and-dumpers post fake claims on social networks to help move the price. Companies like MetaCert are creating systems to suss out fake links and phishing scams.

“If you like to invest in cryptocurrencies and you get a message about an ICO or Token discount that’s time-sensitive and it sounds too good to be true, it is,” said founder Paul Walsh. “Contact the company directly and ask them if it’s real. Crypto companies will not have time-sensitive deals that make you act within minutes or even hours. So don’t get caught off guard — this is how very smart people get duped.”

How can you stay safe? By staying smart.

“Any ICO that promises to make people money should be avoided,” said consultant and writer Marc Kenigsberg. “Check the team for historic projects and track record, read the white paper, make sure there is a need for the product and avoid anything that focuses heavily on marketing and is light on tech. When taking part in an ICO, watch out for phishing sites and addresses posted in slack channels and always verify an address before sending any money.”

VCs or virtual cash?

If you do a token sale, can you still raise VC? Will VCs care? What’s going to happen to VC in general? No one really knows, but we’re trending toward a general acceptance of token sales as a new “investment” vehicle, and more and more funds will be integrating token sales into their investment plans.

Investors are currently in a pickle. Many want to begin buying early coins and one, Moshe Hogeg, has made ICOs his core investment thesis. Others, especially VCs with older funds, must be careful during investment for fear of double-dipping. In short, they are set up to write checks to founders, not to robotic token exchanges. The Harvard Business Review explains the position well. They write:

Venture capitalists, who generally have been standoffish to the ICO phenomenon, are now becoming more interested in it for a number of reasons. One is profits — cryptocurrency investors made some massive returns in 2016, with cryptocurrencies from Blockchain startups Monero and NEM both seeing 2,000% increases in value. For example, the cryptocurrency used for the Ethereum network, called Ether, saw its value double in just a few days in March 2017. Yes, in three days, people who invested in Ether doubled their investment. Those investors can opt to cash out to a fiat-backed currency, or wait for the cryptocurrency to continue to rise (or fall). Volatility is a two-way street. While the price of Ether has been rising, Bitcoin has dropped 20% to $1,000 dollars from a record $1,290 on March 3, 2017.

The second reason VCs are becoming more interested in ICOs is because of the liquidity of cryptocurrencies. Rather than tying up vast amounts of funds in a unicorn startup and waiting for the long play — an IPO or an acquisition — investors can see gains more quickly and can pull profits out more easily, via ICOs. They simply need to convert their cryptocurrency profits into Bitcoin or Ether on any of the cryptocurrency exchanges that carry it, and then it’s easily converted to fiat currency via online services such as Coinsbank or Coinbase.

Ultimately whether or not running a token sale is a good idea will come down to general acceptance by the Valley community; so far, things are looking good. Many accelerator-backed companies are abandoning the Sand Hill Road show for a token sale, and many believe that most seed investment will come from tokens rather than LPs. In the same way Kickstarter has completely disrupted the consumer electronics industry, this is expected to disrupt everything else.

How-to

First, your situation and requirements may not be conducive to a token sale. This is fine. This is not a one-size-fits all solution, but perhaps new systems will fall into place that will help token sellers work more quickly and effectively. What follows is the basic process that a few startups I’ve seen have gone through to “raise” money.

There is no right way to run a token sale. If you need a high-level understanding of things, check out this basic guide we posted earlier. It discusses the sale from a high level. This description is a bit more detailed, but I’m still only scratching the surface.

One thing is certain: there is a right way to do it and a wrong way.

“There are people doing it all wrong,” said Rahul Sood, CEO of Unikrn who recently completed a token sale. “They’re treating this like an equity sale. They’re not getting the proper legal advice to set things up and their white paper looks like a donkey doing calculus wrote it.”

Ultimately, care must be taken to avoid legal issues or, worse, a token sale dud. Why? Because those interested in token sales are now almost fully educated on the pitfalls and benefits and anything untoward is immediately suspect.

“The community is catching on quickly,” said Sood.

1. Create a product. This first step is often glossed over by folks trying to run token sales as quickly as possible, but ignore it at your peril. You must have a product, and this product must use your token. Maybe you can get away with launching an MVP or beta and then running the sale, but assume you’ll have to raise a little equity investment to get your business off the ground. Most estimate you need about $100,000 – $150,000 to really get things going. That’s right: you need money to make money. This is not a hard and fast rule, but keep it in mind.

2. Create a token. At its core you are simply creating a token in the Ethereum ecosystem that can, literally or figuratively, represent something your business needs to survive. “Tokens in the Ethereum ecosystem can represent any fungible tradable good: coins, loyalty points, gold certificates, IOUs, in game items, etc. Since all tokens implement some basic features in a standard way, this also means that your token will be instantly compatible with the Ethereum wallet and any other client or contract that uses the same standards,” write the creators of Ethereum.

These tokens are controlled by something called a smart contract. A smart contract tells the coin how to react in certain situations. The creation of a smart contract is beyond the scope of this article, but you or your techie friends can find plenty of information online. If you need a quick rundown of what a smart contract looks like, visit this page, where the creators of Ethereum create a “minimum viable token” for educational purposes. There are a number of tools to use, including OpenZeppelin.

This code helps manage your tokens and generate your sale. You could also argue that this is the simplest portion of the whole project.

3. Get a legal opinion. Any time you begin messing with other people’s money you’re going to want to be covered legally. Where a token sale really begins is in the pre-sale and legal planning. You need, in most cases, a legal opinion and a legal description of the sale that will keep you on the right side of the SEC. Two law firms come up again and again in token sales. They are Perkins Coie and Cooley. Both are well-established and have cryptocurrency practices. Cooley worked on a framework called SAFT which, in theory, reduces the cost of these legal requirements.

The goal here is to ensure that your token is not a security. There is no effort here to deceive – you just need to be on the right side of the token sale definitions.

4. Write a white paper. After that you need to create a white paper or, increasingly, a deck. White papers are essentially prospectuses — descriptions of a financial plan that include a description of the product, a description of the team and a description of the token generation and distribution strategy. You can take a look at a few interesting ones here and here.

The first paper is a traditional one written much like a scientific treatise. The other paper is written more like a brochure. Both methods are equally effective. The primary mission of a white paper is to describe the product clearly, explain the use of the token and, finally, tell the world how you’ll distribute the coins. I’ve seen white papers that have looked like presentation decks and others with the complexity of a physics textbook. What’s most important, however, is absolute clarity. Sadly, many of these white papers remain unread even during the token sales process, resulting in miscommunication and confusion.

5. Create a community. Community is key in these early days of the token sale. This is the community that will support you. You’ll need a chat room in Slack or Discord where you can communicate with potential buyers and a PR plan. It is a sad but true fact that most token sales are driven by initial hype. Luckily this hype is bolstered by real community, and if you do not create this community early on you will find that your token will quickly fall. Further, you must ensure that early investors don’t sell their coins too quickly.

This is bad optically and bad for the market. Ultimately, you want to create a friendly community that supports you, not your token. There have been far too many token sales that can be considered simple pump and dump schemes for anyone to ignore the community growth aspect. By engendering trust in a core group of fans you can ensure you token remains valuable and useful.

6. Get your token on exchanges. Once you’ve created your coin and are ready to launch, you need to reach out to exchanges to carry your coin. This means people can buy and sell your coins on the open market at certain exchanges. Getting a few strong exchanges to accept your coin is absolutely imperative.

Most tokens will also be listed on CoinMarketCap, a website that is becoming the stock ticker of token sales. This site shows a long list of tokens and their market caps, and most tokens like to see themselves in the top 40. Tokens that crash end up at the end or delisted entirely, and it’s interesting to see the dead coins near the bottom of this massive list.

Token sales often have a pre-sale for accredited investors in order to prevent running afoul of the SEC. These initial sales mean that the public might miss out on a good initial price. but this is par for the course. Finally, most token sales go public, allowing anyone to buy and sell the token. At this point the token must fend for itself in the market, sinking or rising based on news, opinion or rumor.

Further, most companies hold back a number of tokens for founders, employees and investors. It’s this cash that makes these processes worthwhile for initial investors and founders, but remember, it’s not a preferred stock. Investors must have an understanding of your requirements, and many token sellers ask early investors to hold their coins for a period of time. This prevents an immediate dump.

Ultimately, we’re creating a new stock market without stocks, and an amazingly frictionless market. It’s inevitable that some of these token sales will fail, and many of the aspects about this process could change as international law begins to catch up. However the process of explaining, getting legal cover and building community won’t change.

When I began writing this guide I spoke to a token investor in China, Ahmed Al-Balaghi, who noted that there was “no regulation yet, which means everyone can invest and create ICOs.”

“Many new Chinese investors coming in with little or no knowledge of Blockchain and cryptocurrencies are gambling in ICO projects,” said Al-Balaghi. The ICO market in China is quite similar to the rest of the world (barring U.S.), as China has not released such regulations, yet in early June the PBOC hinted that “a regulatory sandbox approach could be adopted towards ICO” and Sheng Songcheng, an advisor to the People’s Bank of China, said recently, “Moderate regulation should be applied, but it should not stifle innovation.” So due to this, it is quite similar to the rest of the world (for the time being) in the sense that everyone can invest and participate due to the nature of ICOs and Blockchain.”

That just changed. The SEC could follow China’s lead by locking down token sales, miners and cryptocurrency firms or they could simply let things stand. The same thing could happen in the U.S. — or maybe it won’t. Until then, assume you should not create equity-based tokens and instead focus on utility tokens.

The process, in short, is get legal cover, write a white paper, make a token and sell it. This is not much different from running a Kickstarter or selling any product. But, because of the nature of these tokens, you must maintain interest and growth. There will be a moment in most of these sales when the naysayers outnumber the fans. This inflection point will sink a company if they’ve bet their entire company on the token sale. Intelligent and careful planning can help avoid this, but nothing can truly prevent it.

Buyer — and seller — beware.

The future

One thing has become clear to me while writing this piece: token sales are the new seed. Startups will have more and more trouble raising equity-based capital and will begin trying to shoehorn themselves into a token sale framework. This is actually fine.

What this amounts to, ultimately, is the embrace of cryptocurrencies as the glue of the financial world. There is plenty of space for multiple token sales, even in the same industry, and we also can expect to see shakeouts and changes to the market over the next few years. However, I suspect that angel investment will move toward token investment over time.

This is just the beginning of a new and unique fundraising model that will leave many losers and many winners. It’s an egalitarian method for raising cash for new ventures. Now it’s up to the makers, the designers, the programmers and the dreamers to make it happen in a sane way.