Every year I attend sections of a Stanford Graduate School of Business class called Formation of New Ventures. The class reviews a case on the decision to take OpenTable public in 2008-2009 at the depth of the financial crisis. When discussing the case, I typically open by asking the aspiring entrepreneurs in the class two questions:

- “Who in here wants to build an enduring company?” — most of the hands in the class shoot up in response;

- “Who in here wants to run a public company?” — no more than a couple of students meekly raise their hands (out of a classroom of 50-60).

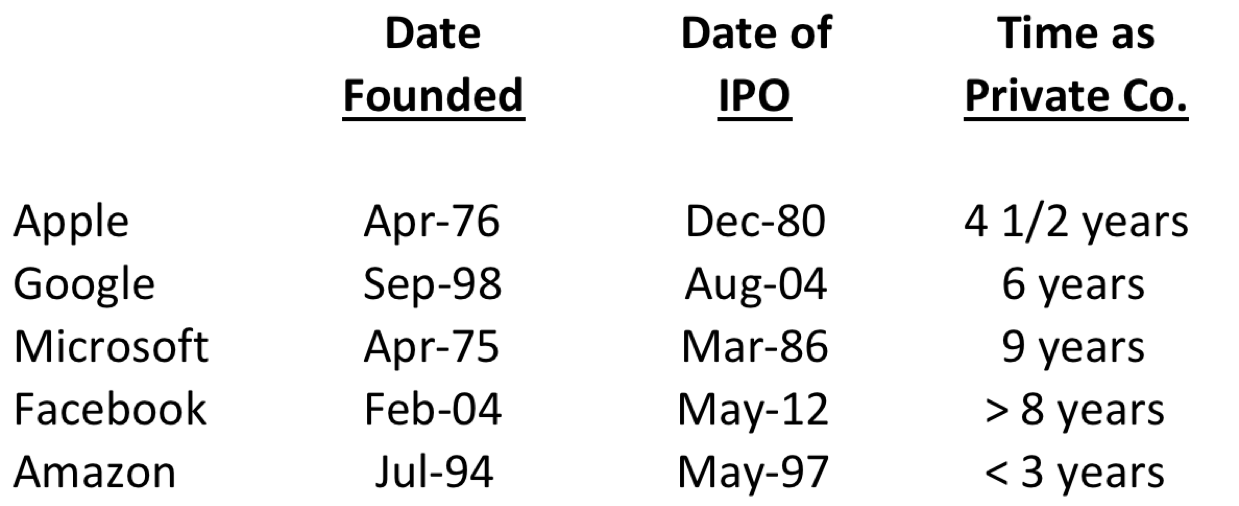

I think this disdain about the IPO is misplaced. Most of the enduring companies that “make a dent in the universe” (to borrow from Steve Jobs) are public. In fact, the five most valuable companies in the U.S. as of this writing are all public tech companies: Amazon, Apple, Alphabet (Google), Facebook, and Microsoft. All of these companies also share in common that a) they were taken public relatively early in their lives, and b) they are/were long run and controlled by their founder(s):

We’ve shared elsewhere what it takes for a company to become “IPO ready”, i.e., in a position to quickly go public if/when it wants. But as a CEO, the OpenTable IPO was a huge learning experience for me — I had never led a financing of any kind before that in my career. And, we took the company public during a time when the conventional wisdom was that the IPO “window was completely closed”.

We recently released a podcast discussing some learnings from the process of the initial public offering itself, and an entrepreneur who had recently taken his company public said he wished that he’d had the chance to hear it in advance of his own IPO process. That and other feedback motivated me to codify more of our hard-earned learnings on the topic of preparing a company to be IPO-ready. (Thanks Freddy!) So here is a list of the 16 things operators should do in advance of an IPO starting a year or two out, in rough chronological order.

New York Stock Exchange building low angle view in Wall Street.

#1 Have a great CFO in place

A great CFO is critical to any later-stage company. As I’ve argued before, it’s easy to pigeonhole the CFO as a glorified “scorekeeper” of only the company financials, but that’s a misconception — because a good CFO doesn’t just keep the “score”; he or she also puts points on the board given their vantage point on the business. And the role of the CFO assumes out-sized proportions in the context of an IPO. There are a seemingly endless number of things that need to be done to be fully IPO ready. My CFO at OpenTable (Matt Roberts, thank you!) took on responsibility for overseeing the lion’s share of these. This freed me up to spend most of my time as CEO continuing to run the company until just before we actually launched the actual IPO.

The CFO is also critical because over time he or she, along with the CEO, becomes the face of the company to investors. It’s expected that the CEO and CFO present the company during the road show, but once a company is public, CFOs spend as much or more time with investors and analysts than the CEO — particularly around earnings calls.

All of the above is why it’s not a good idea to hire a CFO just before you IPO — or worse, have your CFO exit your business soon after you IPO (a highly destabilizing event). You need to hire a CFO who can help you both in the near term and scale for the long term.

#2 Build out the capabilities of your finance team

The bar for readiness in the finance function is high for a public company. The company leadership needs to be able to forecast the business at a fine level. They also need to be able to accurately close the books in a very timely manner. The “accuracy” point is obvious — you desperately want to avoid the dreaded “restatement of earnings” that calls into question company competence. And on “timeliness”, public companies need to be able report earnings a few weeks after the close of each quarter.

Typically in startups the key finance personnel that accomplish all of this report directly to the CFO: heads of financial planning, controller, treasurer, audit, tax. You usually don’t have a public-ready finance team until strong people are in place in all of these second-level roles.

Public market investors hate to be confronted with negative surprises, and tend to react very negatively to them. Such surprises can take large chunks out of a company’s market cap in a flash. But a highly functioning finance team can help avoid those negative surprises. It’s worth the investment to build it out well in advance of an IPO.

#3 Invest in robust internal administrative and financial systems

Early-stage companies allocate scarce product resources to the projects that will move the needle on revenue and profits. As a result, much-needed improvements in administrative systems are almost always deferred… and deferred… and deferred… sometimes until right before they IPO.

This is a mistake. At some point you need to invest in these systems to ensure they’re robust, regardless of IPO. As an investor in private companies, I have observed that such system shortcomings drive many of the “negative” surprises and also tend to obstruct timeliness. But improved systems have another benefit: They can help make the company more efficient and thus more profitable.

There’s an important sequencing here: To start this process you need a great CFO. Then that CFO needs to build out their team. Only then does it make sense to invest a lot more in the systems that will allow that team to be optimally efficient.

#4 Build the right board

Early in a company’s life, the board is dominated by its lead investors. But a board membership populated only by venture capitalists with large ownership positions often has these issues in the context of IPO readiness: First, most VCs have never worked at or run a public company, and few have meaningful experience serving on the boards of public companies — so contributing to the best-practice governance of the newly public company is a learned skill. (This isn’t a bad thing in and of itself, but not ideal if both the CEO and the board is unschooled there.) Second, public company boards have requirements — due to SEC and stock exchange guidelines — with respect to independent or outside directors that large investors often can’t fulfill.

CEOs will therefore need to execute a transition where some, most, or even all of their investor board members are replaced by independents. And if you want a fully functioning board that you’ll trust when you are a public company, then begin this process early; it’s too risky to do meaningful board composition changes late in the process. After all, the key accountability of a board is holding the CEO accountable.

I’d also advise CEOs not to think of independents as unwelcome outsiders — believe me, the right independents definitely help make the company better. I learned this at eBay; I saw firsthand how our outside directors Scott Cook (founder of Intuit) and Howard Schultz (founder of Starbucks) brought important new perspectives that complemented the strong contributions of the insiders already on the board, from then-CEO Meg Whitman and founder Pierre Omidyar to Bob Kagle (GP at Benchmark Capital).

NEW YORK, NY – APRIL 17: View of the NASDAQ Stock Market at Times Square in Manhattan on April 17, 2017 in New York, United States. (Photo by William Volcov/Brazil Photo Press/LatinContent/Getty Images)

#5 Start meeting with select bankers early

The selection of the right banker is critical to a successful IPO process. Bank brands are important, but to me the more important attributes are the quality of the individuals actually working on your deal and the quality of your relationship with them — you want a banker with whom you have a deep relationship built on trust. I’d also argue that a critical part of that relationship is that the bank provides full transparency into the deal dynamics — pricing, allocations, etc. — during the process.

No venture-backed tech company had gone public in the couple years preceding the OpenTable IPO. As a result, every investment banker in Silicon Valley wanted in on the deal. We ended up selecting Merrill Lynch as our lead, which wasn’t the lead banking brand in Silicon Valley at the time. But we developed a lot of respect and trust in their team, particularly in their then-capital markets lead JD Moriarty; we became convinced that they (and we) would collaborate effectively on the transaction. They rewarded this trust handsomely over the course of both the OpenTable IPO and secondary transactions by taking a thoughtful and collaborative approach. (I’d be remiss to not also compliment the very important role that Harry Wagner at co-lead Allen & Company bank played in the transactions; they helped us develop relationships with a number of public market investors that over time became OPEN’s largest investors.)

#6 Start meeting with target investors well in advance of the filing

All investors are not the same, and this is as true of public market investors as it is of private market investors. In the consumer internet, there are a handful of investors at mutual funds who have lots of capital and demonstrated track records of buying and holding select positions; I assume this is true in other sectors as well. So the odds of having a successful run as a public company go way up if you get some or all of them to participate in a meaningful way as well as hold for the longer term. It also makes the process of running a public company easier. The odds of these investors participating also go up if you’ve built a relationship with them over time and educated them about your business.

The IPO road show is a bizarre process — you visit with investors and they have 60 minutes with you in a rehearsed presentation to decide if they want to make a multi-million dollar commitment. The more they know about you and your company in advance of that meeting means they’re in a better position to pull the trigger on the investment.

The SEC allows these informal conversations; they’re called “test the waters” meetings.

In our case, we started periodic meetings with a targeted set of investors more than a year in advance of our filing. The most efficient way we found was participating in “bus tours” organized by leading investment bankers, where they would gather a select group of these investors in the Valley for a few days to meet with a set of companies. Spending an hour every few months with select, high-quality investors helped us efficiently start building relationships — and an understanding of our business that would have long-term value.

That said, I’d caution entrepreneurs to wait until you have visibility into potential IPO timing before you start talking to both bankers and investors. Otherwise you might do it too early, and those conversations suck up a huge amount of time that early on is better spent on other things like growing the business. You want to be cautious of premature/excessive disclosure early on as well, as bankers and investors could be working with companies that are your competitors.

#7 Clean up your cap table

Issues involving equity can accumulate over the years as early stage companies scale over time. Maybe it was an early verbal agreement that never got documented. Or an early contractor or advisor that never got their shares. Or a disgruntled ex-employee.

Once you file to go public, the stakes of resolving these issues go way up — certainly in perception, and often in reality. Frankly, your leverage in resolving any latent or lingering ambiguous issues is much higher before the IPO drum starts beating too loudly. So dedicate time to identify and resolve potential issues early in the IPO-readiness process. (There are now a number of free tools out there for helping manage cap tables too, like this.)

#8 Communicate (carefully) with your company about IPO plans

There’s a fine balance to strike here. On one hand, you want to and often need to communicate with the company about your IPO plans, at least at a high level. But on the other hand, it’s not a good idea to commit to specifics such as timing, pricing, post-IPO stock performance, and so on.

Here’s what I said to the OpenTable team a couple of years prior to our IPO: “Our aspiration is to be a public company so that we’re in control of our long term destiny. And we think we’re building a business that will be attractive to public market investors. So we’re embarking on a concerted plan to be ready to be a public company when we think the timing is right. We’ll likely ask for the help of some of you in doing this. Everyone else, please keep your heads down and focus on continuing to deliver results. Oh, and keep these plans confidential, as leaks could have a negative impact on our potential timing”.

Why avoid specifics? Because shit happens. OpenTable had scheduled its org meeting for our planned IPO for Monday, September 15, 2008. Over the previous weekend, however, the global financial system started melting down as Lehman declared bankruptcy. And then our lead bank Merrill Lynch suddenly needed to be rescued by Bank of America (which acquired it, so it’s now Bank of America Merrill Lynch). Oh, and consumers everywhere collectively freaked out and drastically slowed discretionary spending — which meant revenues at our partner restaurants fell 15% over a single weekend. In a dramatic understatement, I told the company, “This is not off to a good start.”

Lesson learned: The right way to discuss the company’s IPO plans is to talk about your aspirations and plans in broad strokes, but give yourself enough wiggle room on the fine details so you can navigate the unexpected.

#9 Hire the right accounting firm

Make sure you have a reputable accounting firm capable of supporting you in your efforts to be a public company and well beyond. This is an area where I believe brand does matter: There are a (shrinking) handful of accounting firms that investors recognize and trust, and not using one of those is a potential cause for concern. You should also be comfortable with your specific partner at your accounting firm — it has to be someone that both you and the CFO want in the trenches with you, because believe me, you’re going to be.

And make sure that the national office signs off on your planned accounting treatments as early in the process as you can. Early in the company’s life, virtually all of its interactions with its accounting firm are with the local office only. But as the company moves towards being public, the risk profile of the company increases for its accounting firm. Before you file an S-1, they will insist on getting your accounting treatment signed off by the national office. And more often than you might realize, the national office actually overrules the accounting treatments that the company has been deploying until then. Resolve the definitive treatment as early as you can, so it can be incorporated into all aspects of the process including go-public audits, statements, forecasts, and just overall accounting.

#10: Resolve your company’s corporate governance

Resolving good corporate governance as well around the issue of founder control is increasingly a “pick your poison” proposition these days:

On one hand, we live in a world where there are a ton of activist investors seeking to exert influence an ever-expanding array of public companies. This can be highly disruptive to companies, and is huge chore for founder/CEOs to manage through — particularly when they don’t have access to supportive corporate governance tools.

On the other hand, the key tools for fighting back against activist investors (e.g., giving founders/CEOs strong governance control) risks undermining accountability at a company.

But you and your board do need to proactively to pick your poison here, and then implement it.

Giving a founder/CEO effectively “full” control over his or her company continues to be controversial. Whatever your position on the right degree and approach here, the fact remains (as noted earlier) that the most valuable companies in the U.S. are technology companies that had or have long-term founder control/involvement in their companies. Imagine if activists had forced Jeff Bezos out of Amazon early on while he was suffering negative headlines; investors most certainly would have missed out on most of the 491-something (split-adjusted) multiplication in value since! (Put another way, $5000 invested at the time of IPO would be roughly $2.4 million today.)

#11 Develop a long-term financial model

I believe the day you start earning revenue is the day you should start building out your long-term revenue model, if not sooner. It will immediately make you smarter about the actual dynamics of your business, and will guide your focus as CEO to the high leverage areas.

You’ll definitely need to re-visit early assumptions, and often, but this is part of the learning process. Over time and done right, you should have a highly predictable business where you’re focusing on pulling the right levers. Not only will bankers and investors question you about this as you go on the road, this framework is what you need to have in place to even consider being a public company — especially given the devastating impact of the earnings “surprise”.

#12 Interrogate your P&L

Comb through your profit and loss (P&L) statement looking for things that you eventually might want to change… and then change them, well in advance of the filing. Say your company has a material revenue stream that you never really embraced or that you didn’t think was very profitable; or that your pricing might not be sustainable long term; or that you weren’t investing in a material cost area that you thought was strategically important. It’s actually relatively easy as a private company to make changes that address things like this, before you start to print the quarters immediately preceding an IPO. It’s much harder to make material changes like this once you’re already public.

That said, I do think the oft-cited point that public company CEOs get pressure to manage for the short term is overblown. Yes, there’s pressure. But if you get the right shareholders and create the right expectations, they’ll be open to conversations about initiatives that you think are important in the long term.

Bezos provides an obvious example here: Distant spectators bemoan that Amazon never made money, though Amazon clearly has lines of business that throw off copious cash. Yet Bezos has created the expectation among his long-term investors that he will invest that cash in initiatives such as AWS, international growth, and products like Alexa to drive growth and value. I know a few investors who got Amazon IPO allocations and still own those very shares 20 years later — it’s been one of the absolute best return drivers for their funds.

#13 Don’t starve the business heading in to an IPO

Public market investors these days want to see profitability or (more often) a clear path to profitability; they tend to focus more on the future than the past. Layer in key spending, especially for growth initiatives, before you go public. It’s a whole lot easier to show improved profits as a public company if you’ve accelerated the necessary investment for those future profits while you’re still a private company.

We did this at OpenTable, making sure we had the people we wanted to run the business for at least a year when we filed to go public. As a result were able to moderate expense growth meaningfully in our early years as a public company. Our ongoing revenue growth on top of these relatively flat expenses demonstrated to investors the leverage the business would have in the long term. They rewarded the stock handsomely as a result.

#14 Carefully think through planned metrics reporting

Resolve the way you plan to present the company to investors, including your KPIs (key performance indicators) and segments. This seems basic, but it’s actually very important and not done as well as it should be [see for example theseand these metrics]. Basically: management should strive to give investors the metrics they need to understand and predict the business.

But in the case of metrics, less is more. Investors and analysts will track any and every metric you give them, so giving them the most high-leverage ones to focus on will help them get quickly to the essence and heart of the business. Loading them up with relatively unimportant ones — or worse, giving them the wrong ones — will cause confusion and distract them from the real investment management challenges for the company.

Along these lines, once you report on a metric, you create an expectation and appetite for it; it’s really hard to stop reporting on that metric over time once you start. So be very careful about dropping “orphan” metrics — regardless of how tempting it may be at the time — once you’re a public company and frankly, even before then.

#15 Run an internal quarterly earnings process

You should start running an internal quarterly earnings process exactly as you’d do it once the company is public. This seems obvious, but it’s shocking how few people really do it. Because it’s not just a simple matter of scaling and adapting what you’re already doing; nailing the quarterly earnings process will involve lots of practice and hitches to be ironed out before you can successfully navigate it as a public company. Every good company — regardless of whether public or not – needs to be able to accurately forecast the business.

And if you elect to give “guidance” to the market (some by the way do not, more on the nuances of that in this podcast), you will also need to be able to navigate the ladder of go-forward “beat and raise” forecasts over multiple quarters within the constraints of your forecast.

Finally, since you will need to effectively explain the results (financial statements and KPIs) — don’t assume they’re self-evident — do a formal run-through of your earnings call with a subset of your best-informed private investors. Ask them to be aggressive in their questioning; I can guarantee that your public market analysts and investors will be!

#16 Position the company to over-deliver on expectations

While you’re so focused on executing the mechanics of the previous 15 steps towards becoming an IPO-ready company, it can be easy to lose focus on the business itself. But you’ll only have a long-term successful public company if you position the business well for long-term growth and profitability.

The IPOs that perform poorly in the market are often companies that under-deliver on expectations early in their tenure as public companies. The potential explanations as to why you missed one of your first quarters as a public company are all ugly:

1) The business is not as robust as you claimed it was when marketing the IPO.

2) Something unexpected changed materially for the worse, and quickly.

3) Management is incompetent.

I counsel founder/CEOs looking to take their companies public to work their asses off developing new initiatives/products/geographies — things that give them a high degree of confidence that they’ll also be able to exceedanalyst revenue forecasts for at least 1-2 years once public.

This is not to say that new ideas and initiatives can’t come up; it’s fantastic if they do. But I advise people to plan on having something in their back pockets that they can layer in as a public company to drive go-forward over-performance. I have been involved in sub-scale, low-growth public companies in the past and wouldn’t wish that on anyone; it’s a long-term sentence to oblivion. So if you don’t think you can put up attractive results for multiple years following an IPO, then you should seriously contemplate an alternative exit path (like M&A) or hold off on an IPO until you’re sure you can.