London-based Tail is a new fintech startup that offers a glimpse into the promise of Open Banking. This is seeing upcoming legislation in the EU and U.K. force banks to offer third-party developer access to your bank account data — with your permission, of course.

The app, initially available for iOS and serving London only, offers heavy discounts at local places to eat and drink, all linked to the card you pay with and delivered each week in the form of cashback. However, the draw is how seamlessly it all takes place, by being built on top of digital-only challenger bank Starling‘s API, with Monzo integration also in the works.

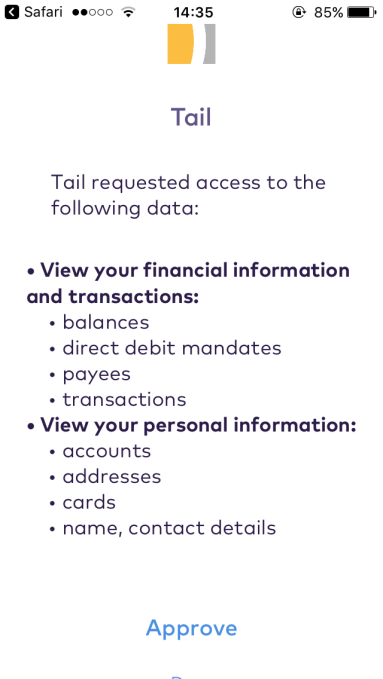

This means that it is as simple as granting the Tail app access to your Starling bank account, a one tap process akin to Facebook or Twitter log-in, presuming that you are already a customer of Starling. Once you’ve agreed to a set of permissions — which can be a little daunting the first time, even though they can be easily revoked within the Starling app at any time — any offers that pop up in the Tail app can be redeemed simply by using your Starling MasterCard at the corresponding merchant.

This means that it is as simple as granting the Tail app access to your Starling bank account, a one tap process akin to Facebook or Twitter log-in, presuming that you are already a customer of Starling. Once you’ve agreed to a set of permissions — which can be a little daunting the first time, even though they can be easily revoked within the Starling app at any time — any offers that pop up in the Tail app can be redeemed simply by using your Starling MasterCard at the corresponding merchant.

No coupons or receipt scanning or even having to explicitly tell Tail the bank account or card number you want your cashback deposited. And, presumably, once your Starling card has expired (or is lost or stolen), you won’t have to manually link your new card to Tail as it will simply pull the new card info via the challenger bank’s API.

My takeaway: Open Banking is going to be nothing if not convenient, depending on how comfortable you are with granting third-party apps access to your banking data.

“Tail is turning open banking APIs into an offer platform, thereby eliminating all friction points for retailers and consumers which are still inherent in today’s solutions,” Tail founder and CEO Philipp Keller, who was previously at Morgan Stanley, tells me.

“Using Tail, consumers can browse through a selection of curated offers, which are pre-linked to their bank card, eliminating the need for physical vouchers or coupon codes. The offer feed is updated in real-time and location specific. Redemption happens in-app, allowing for a more discreet way of redeeming offers, and accumulated savings are distributed back to the user in the form of cash back paid out in regular intervals”.

Meanwhile, along with making it super convenient for customers to discover and redeem offers, the Tail CEO reckons it is addressing a number of merchant pain points too, and thus opening up this kind of offers platform to smaller independents right down to the Long Tail.

“There’s no EPOS integration or codes required, no staff involvement whatsoever, they don’t have to download an app and we track the redemption stats for them,” he says. “The retailer provides card details and tells us what type of campaign she wants to run, the discount and the applicable times”.

In addition, new tools, such as real-time flash campaigns or “sequenced offers,” help to address specific issues such as spare capacity utilisation and new customer acquisition more effectively.

Flash campaigns that are simple to run via Tail could include a merchant offering 50 per cent off on a rainy day, or putting up an offer for the next 30 minutes during an unexpected lull in footfall. And by “sequenced offers,” Keller is referring to ways of enticing first time customers to become repeat customers, such as different discounts depending on if it is a first, second or third visit to a particular restaurant.

“We’re looking to turn this into a self-serve platform at some point. At that point it will be even easier; just insert campaign type (first-time customers, off-peak hours, etc) and enter card details,” he adds.