The connected hardware space has undoubtedly gone through a renaissance over the last four years, with VCs nearly tripling their funding between 2012 and 2016. Changes in funding patterns have been felt in the industry in myriad ways, including the viability, typical runway and capitalization of companies. These are fundamental changes that affect how startups decide to run their businesses and develop their products, so they’re vital to understand.

This year, we gleaned some new data from Pitchbook around venture funding in IoT to get a quantitative understanding of whether investment in the space is continuing to grow or flattening out. Here’s what we learned…

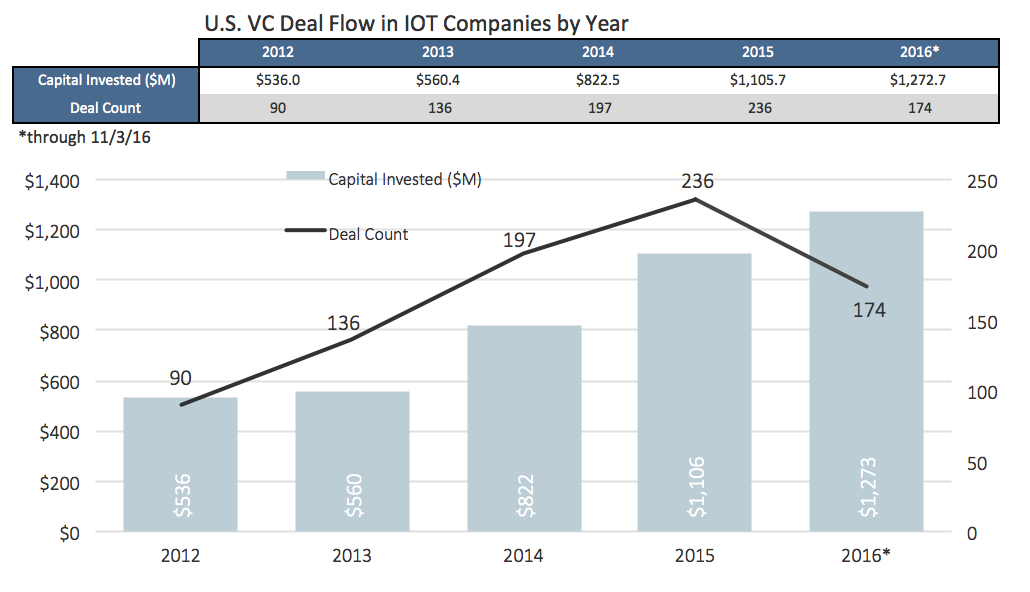

Funding totals are up, but numbers of rounds are down

By early November of 2016, IoT funding had already sped past 2015’s total, bringing in $1.27 billion. However, the total number of companies receiving funds was down, from ~200 at the same time last year to 174 today. If the current rate continues through the end of 2016, this would be a 10 percent drop from 2015, while the total funding for connected hardware companies would be up nearly 40 percent.

What does this mean? Well, for one, we’re likely seeing the space mature. We’ve heard this anecdotally, but the data agrees: More funding is going to fewer, more promising companies. Although there have been a number of public setbacks in the IoT space (especially around crowdfunded hardware — Skully, Coin, etc.), clearly confidence in the space remains.

Other data also points to a maturing investment market…

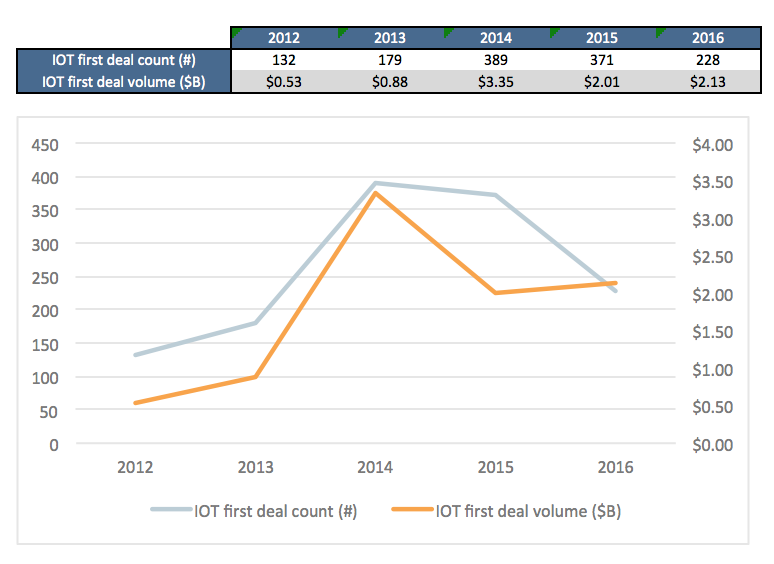

IoT investors gain more experience

The chart above shows the year that VCs and angels first invested in an IoT company. We can see here that fewer first-time VCs and angels are entering the connected hardware space, with first-time participation in financing rounds falling from the 2014 peak.

To those of us in the industry, this signals a move in the right direction.

One of the issues I’ve seen startups encounter over the last couple of years is VCs who have traditionally been in the software space investing in connected hardware. Bubbles and hype attract capital — which is great — but this means interfacing with a growing number of investors who have little to no experience in the connected hardware space and its intricacies.

Experienced investors are invaluable, as they can help companies navigate long development cycles. Extra runway and heavy pre-launch testing necessitate greater patience from investors. Instead, startups are seeing pressure from impatient, non-experienced VCs act as a counterproductive force.

Anecdotally, startups are also seeing more investors asking tougher questions this year. Problems remain, but pre-round due diligence seems to be getting more stringent. Founders who are looking to start a connected hardware company should expect questions centered around the desire for a working prototype that addresses the basic questions around product feasibility; an awareness around the potential development challenges; an understanding of the technologies that would be used in your product and why you are choosing those technologies; and early signs that a manufacturer is willing to work on your product.

These are crucial check boxes that first-time investors were glossing over too quickly during the hardware bubble. More investors have a healthy skepticism fueled by experiencing endless delays or products that never ship. They’re also more aware of red flags, like low-quality schedules, where no buffers are shown for integrating learnings, ID iterations or contingency plans. VCs will always prefer to see a realistic and feasible scenario over one that makes a company look good but is pie-in-the-sky.

The trend toward higher expectations and tightening due diligence makes one think that rookie hardware startup founders would have a harder chance at bringing in funding. But you’d be wrong…

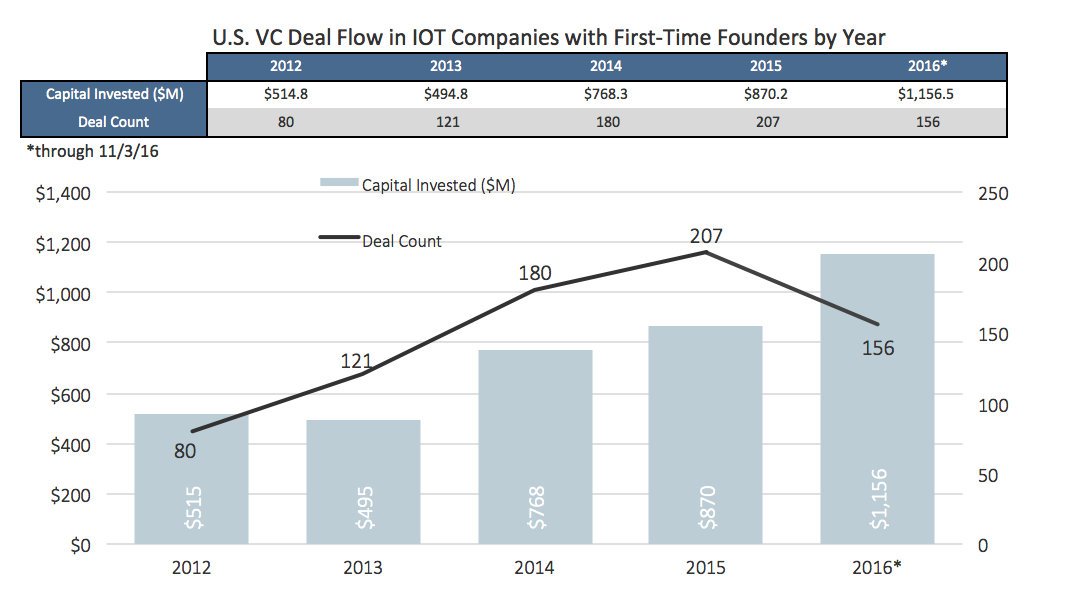

First-time founders are not at a disadvantage

Although the chart above makes it look as though first-time founders have had an unfavorable 2016 in the hardware space, they are, in fact, right around average. From 2012 to 2016, anywhere between 80 to 90 percent of IoT startups were founded by first-timers.

Surprisingly, it is 2015 that stands out as the anomalous year, with serial founders jumping into the fray and snagging 22 percent of total funding in the space. Otherwise, first-time founders tend to collect 90-95 percent of all hardware funding.

This is obviously just a snapshot of the connected hardware industry, but it illustrates the creation of a healthy market that’s settling in for the long term, with less “bubble” around the edges, where founders and investors are no longer throwing everything they have against the wall to see what sticks.

And that’s a good thing.