Accel Partners has pulled off a bit of a hat trick. In an increasingly uncertain economy, it has raised $2 billion across two new U.S. funds. The Sand Hill Road outfit has closed a $500 million U.S.-focused early-stage fund to back mostly seed and Series A stage deals (its 13th); it also raised a new, $1.5 billion growth fund to back more mature companies that are already profitable enterprises thanks to their owners. Think Qualtrics, a 14-year-old online survey research platform company that was bootstrapped for its first decade.

The funds — which were raised in two months, says the firm — come just two years after Accel raised its previous two funds, which were $475 million and $1 billion, respectively. The turnaround time is reminiscent of others in the market, including GGV Capital, which is currently raising more than $1 billion less than two years after raising its current fund.

To learn more about Accel’s pacing, and what else these newest funds might herald, we talked yesterday with three of the firm’s five senior members: Sameer Gandhi, Ping Li, and Rich Wong. (The firm’s other senior members include Andrew Braccia and Ryan Sweeney.)

TC: How big is the firm at this point?

RW: We have eight partners and eight principals, so 16 people leading deals, not including venture partners.

TC: You’ve told me that the team does both early-stage and later-stage investing. For example, Andrew Braccia led your early deal in messaging app Slack and in the online education company Lynda, which was a much older business at the time (and soon after sold to LinkedIn). So why not just raise one fund?

SG: It’s not continuum investing. There are two distinct strategies and we feel like having separate vehicles with separate decision criteria that’s easy to define and measure keeps us pure.

TC: How big are the checks you’re writing from both your early-stage and your growth funds?

SG: We like doing small seed investments of $500,000 to $8 million in seed and Series A deals. We’ll invest on average $35 million in a growth-stage deal, though the check might be $15 million or it could be $70 million.

TC: You seemed to raise this money pretty soon after raising your last funds. Were you rushing owing to growing uncertainty in the market?

RW: No. Accel was founded in 1983 and a good percentage of the LPs in this most recent cycle were part of that first fund. These investors have been with us for 30 years, so we’re not trying to time the market.

PL: If anything, we want to be out in the market right now because we think there are a lot of good ideas and entrepreneurs out there and that 2016 will be a good time from a tech perspective, meaning the last thing you want to do is to be out of the market fundraising.

RW: Back in 2008, 2009, [Accel portfolio] companies like Cloudera, Slack, Dropbox and Atlassian were founded and they’ve come a long way. We’re hoping this [current] reset of valuations will set up a similarly interesting 2016 and 2017.

TC: It’s a good time to invest. But is it a good time to reinvest in your maturing startups? The IPO market seems all but shut right now.

RW: We think companies like [project management software startup] Atlassian that have a certain amount of revenue and profitability can go public even in a choppy environment. We also think we’ll see a lot of M&A activity, with large tech companies needing to position themselves for the world of cloud and mobile.

TC: Atlassian is based in Sydney. But you mostly focus on the U.S. Is that correct?

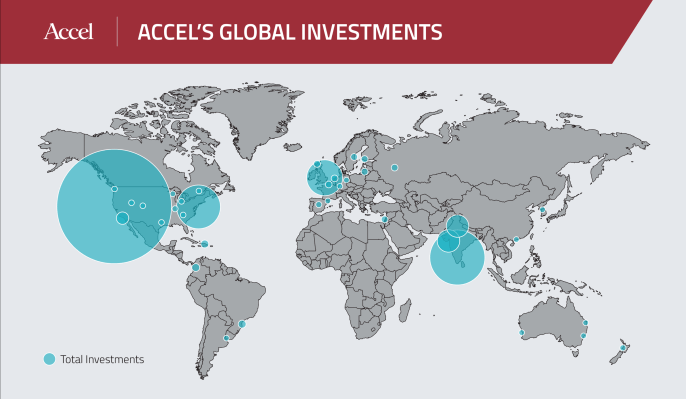

SG: When there’s a breakout company, we’ll go to Sydney or Europe or India, but it’s a smaller percentage of our strategy. Of course, we also have [affiliate funds in] Europe and India where there are dedicated vehicles with local partners executing on geography-specific strategies. We [invested alongside Accel Partners in India] in [the e-commerce company] Flipkart, for example. We also co-invested with [Accel Partners in London] in [the Paris-based shopping site] Showroomprive.

TC: You raised your last two funds two years ago, which seems to be happening more broadly because the rate of funding rounds for startups had picked up in recent years. Is this the new normal?

RW: Raising quickly is not the new normal. We probably won’t cut over to our new funds [to invest from them] until the fall of this year. We still think that 2.5 years to three years is the right goal [in terms of fundraising pacing] and we intend to keep doing that.