A recent discussion on the tech IPO market yielded the comment “all IPOs this year were down rounds.” Square’s recent IPO priced below its last private offering, spurring Khosla (a Square investor) partner Keith Rabois to comment to The Wall Street Journal that “the steroid era of startups is over.” But the data on IPO down rounds, a concept we first reported on in TechCrunch in March, tells a different story.

As with our story on IPO down rounds, we gathered the data on IPOs through the end of October 2015 and compared the IPO price of each company to the last private round of financing they’d raised to determine which were down rounds.

Here’s what we learned.

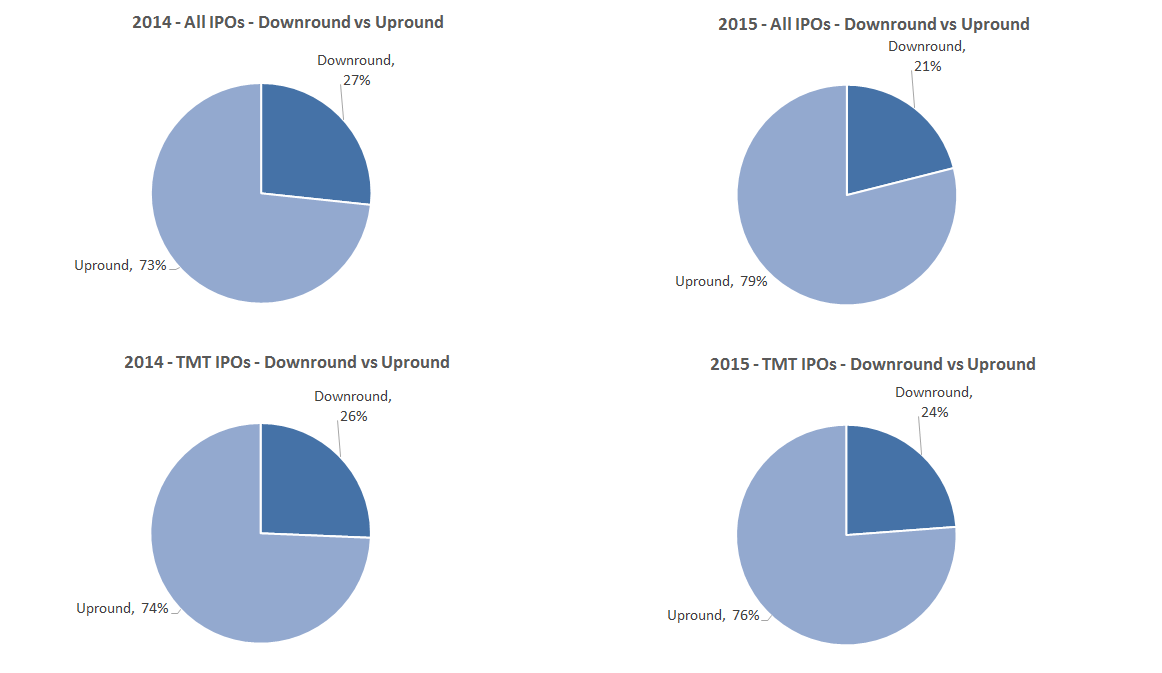

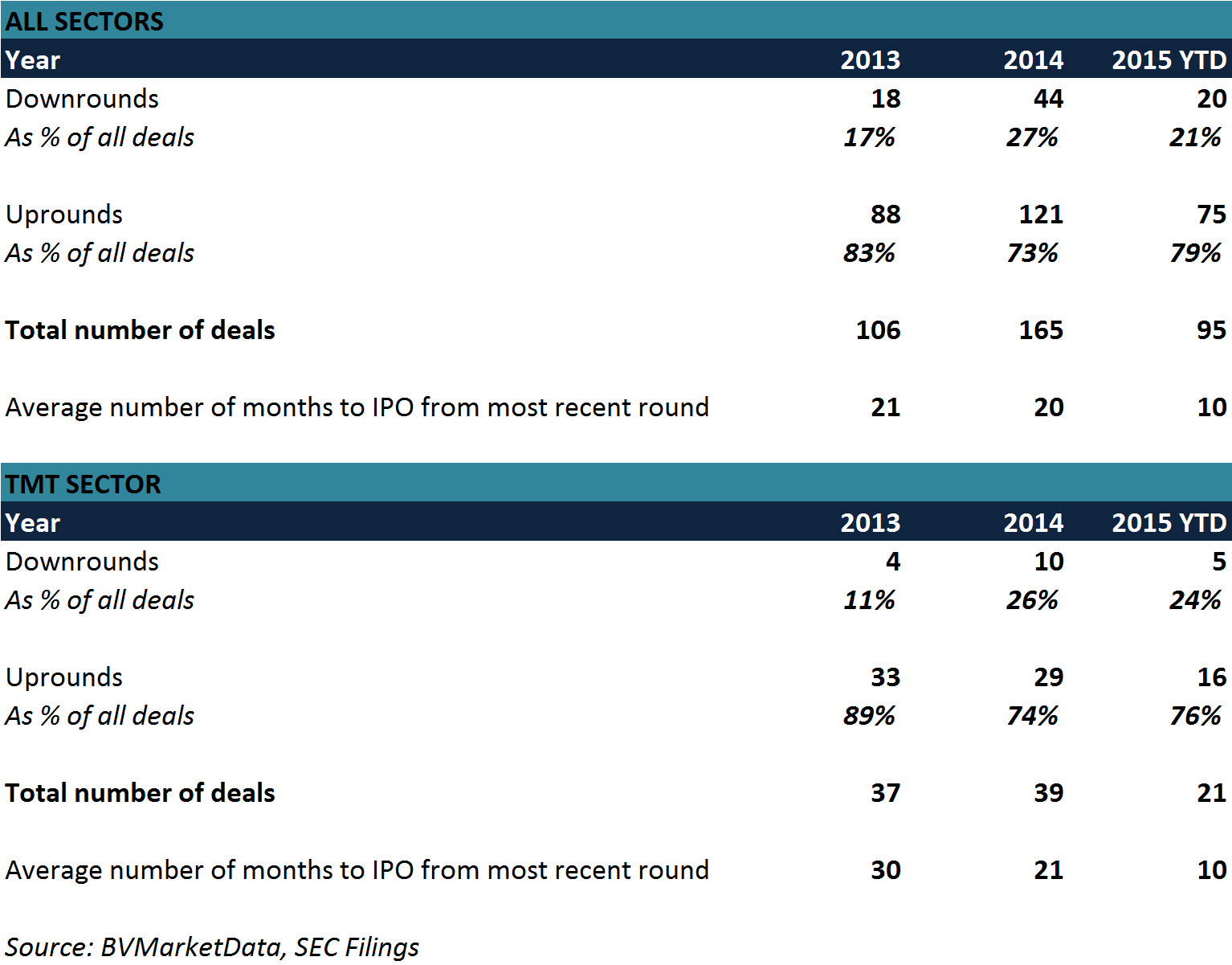

So far this year there have been 95 IPOs, 21 of which have been in the technology, or TMT, sector. Of those, 20 of the total and 5 of the TMT sector have been down rounds; slightly less than last year.

In 2014, 27 percent of all IPOs were down rounds, compared to 21 percent of all IPOs so far this year. The spread is a bit tighter in TMT, with 2014 yielding 26 percent of IPOs as down rounds versus 24 percent so far this year.

So, while some IPOs are pricing below the last private rounds companies have raised, they are not doing so at an accelerated rate, as yet, and remain the minority of cases.

One interesting trend that makes the lack of acceleration that much more intriguing is that IPOs are now coming to market far faster after their last private round than previously. In 2014, the time from last private round to IPO averaged 20 months; this year, that time was cut in half. In TMT, the time to market went from 21 months to 10.

One would assume that if deals were being rushed to market the pricing would reflect it, as public investors enforced the rigor an IPO process and diligence requires — but the modest decrease in down rounds doesn’t show that to be the case.

While the IPO markets are certainly evolving and creating more challenging realities for the companies going public, and perhaps thereby creating a self-cleansing system where only IPOs that can sustain or justify their valuations can be brought to market, the data makes it clear that the trend of IPO down rounds specifically is not worsening.